Homeowners across the country are sitting on a record amount of equity. Whether you are in the suburbs of Indianapolis, a historic neighborhood in Louisville, or the booming markets of Florida and California, your home has likely increased in value significantly over the last few years.

You want to renovate. Maybe it is the kitchen that hasn't been touched since the 90s, or perhaps you want to add a primary suite to increase your property value. In the past, the go-to move was a cash-out refinance. Today, the strategy has shifted.

Jump in as we explore why the Home Equity Line of Credit (HELOC) has become the weapon of choice for smart homeowners and real estate investors in Alabama, Arkansas, Michigan, Indiana, Illinois, Florida, California, Georgia, Kentucky, Missouri, and Virginia.

The Equity Goldmine You Are Probably Sitting On

Most homeowners secured incredibly low mortgage rates between 2020 and 2022. If you are locked into a 3% or 4% fixed rate, giving that up to access cash feels like a step backward. This is the primary reason the cash-out refinance has lost its luster for many.

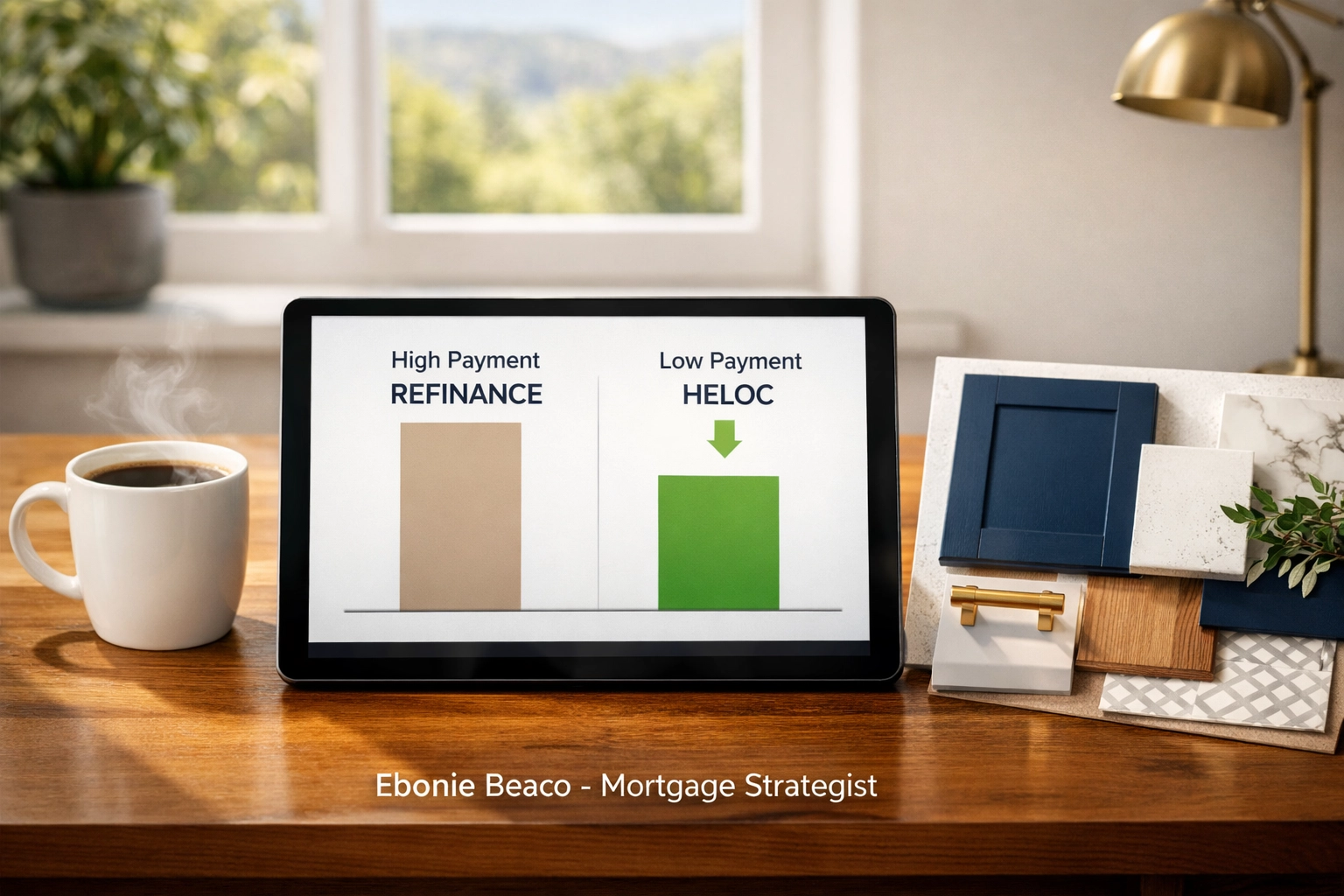

When you use a cash-out refinance, you replace your entire first mortgage with a new one at current market rates. If you owe $200,000 at 3% and need $50,000 for renovations, a refinance forces you to pay current rates on the full $250,000.

A HELOC allows you to keep that low interest rate on your main mortgage while only paying the current market rate on the money you actually spend for your project.

Defining the HELOC

HELOC: Home Equity Line of Credit.

A revolving credit line secured by the equity in your home that functions similarly to a high-limit credit card.

Benefit: You only pay interest on the amount you actually draw, not the total limit available.

Explore your options for a HELOC loan to see how this flexibility fits your renovation timeline.

Defining the Cash-Out Refinance

Cash-Out Refinance: A new mortgage that replaces your current one for a higher amount than you owe.

The difference between the two loans is paid to you in a lump sum at closing.

Benefit: Provides a predictable, fixed monthly payment for the entire balance of your home debt.

Compare this against other fixed-rate mortgage options if you prefer long-term stability over flexibility.

Why Refinancing Is Losing the Renovation War

The math is simple. If you refinance a low-rate mortgage into a higher-rate mortgage, your monthly cost increases across the entire debt.

Imagine you have a $300,000 mortgage at 3.25%. Your principal and interest payment is roughly $1,306. If you need $100,000 for a massive renovation and refinance into a new $400,000 loan at 6.5%, your new payment jumps to approximately $2,528.

By contrast, keeping your $1,306 payment and adding a HELOC for the $100,000 draw might result in an interest-only payment of around $700 during the draw period. Your total monthly outflow stays lower while you complete your project.

The Stealth Advantage: Lower Closing Costs

Closing costs can be a significant hurdle when accessing equity. A cash-out refinance is a full mortgage transaction. You are looking at appraisals, title insurance, origination fees, and various taxes that typically range from 2% to 6% of the loan amount.

In states like Florida or Virginia, where closing costs can be high, this eats into your renovation budget immediately.

HELOCs generally have much lower closing costs. Many lenders offer HELOCs with minimal fees, and some even waive the appraisal if an automated valuation model can be used. If you are looking for an Indiana HELOC lender or a Kentucky HELOC lender, you will find that the entry cost for a line of credit is often a fraction of a full refinance.

Flexible Funding for Phased Renovations

Renovations rarely happen all at once. You might tear out the kitchen in May, but the custom cabinets don't arrive until August, and the contractor doesn't finish the flooring until October.

With a cash-out refinance, you receive a lump sum on day one. You start paying interest on that full $100,000 immediately, even if it is just sitting in your savings account.

A HELOC allows you to draw funds as the invoices come in.

- Draw $15,000 for the deposit.

- Draw $20,000 for materials.

- Draw $10,000 for labor.

You only pay interest on what you have spent. This "pay-as-you-go" model is why Airbnb hosts and fix-and-flip investors in markets like Chicago and Atlanta prefer this method to manage cash flow.

How Much Can You Actually Pull Out?

Lenders typically allow you to access up to 80% or 85% of your home’s value, combining your first mortgage and your new HELOC. This is known as the Combined Loan-to-Value (CLTV) ratio.

Calculation Example:

- Property Value: $500,000

- Maximum CLTV (85%): $425,000

- Current Mortgage Balance: $280,000

- Available HELOC Equity: $145,000

Access our mortgage calculators to run your own numbers based on your local market value in cities across Alabama, Missouri, or Arkansas.

Regional Highlights: Indiana and Kentucky Market Insights

The Midwest has seen steady appreciation. If you bought a home in Indianapolis or Louisville five years ago, your equity has grown substantially.

As an Indiana HELOC lender, we see many homeowners using equity to modernize older homes in areas like Carmel or Fishers. Similarly, as a Kentucky HELOC lender, we help clients in Lexington and Louisville tap into equity for everything from basement finishes to ADU (Accessory Dwelling Unit) builds.

The strategy remains the same: protect the low-rate primary mortgage and use the HELOC as a flexible tool for improvement.

Is There a Catch? Understanding Variable Rates

Transparency is vital. You should know that most HELOCs come with variable interest rates. This means your payment can fluctuate based on the prime rate.

While the draw period (usually the first 10 years) often allows for interest-only payments, the rate can go up. If you are someone who needs absolute budget certainty, you might explore a fixed-rate mortgage instead.

However, many homeowners find that the ability to pay the HELOC down and reuse it outweighs the risk of rate fluctuations, especially for short-term renovation projects.

The Investor Strategy: HELOCs for Scaling

Real estate investors in California, Georgia, and Virginia often use HELOCs on their primary residences to fund the down payment on investment properties. This is a classic move for the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) method.

- Access equity via a HELOC on your primary home.

- Use that cash to buy a distressed property.

- Renovate the property.

- Refinance the investment property into a DSCR loan.

- Pay back the HELOC and do it again.

This strategy allows you to move quickly in competitive markets like Northern Virginia or Southern California without waiting for slow traditional financing.

Navigating the Loan Process

The loan process for a HELOC is generally faster than a traditional refinance. Because the loan amounts are often smaller and the risk is secondary to the first mortgage, the documentation requirements can be more streamlined.

Whether you are a self-employed borrower in Michigan or a salaried employee in Missouri, understanding your mortgage basics will help you prepare the necessary tax returns and bank statements to secure a high credit limit.

How to Choose Your Path

Compare your options by asking these three questions:

- How much do I need? Small to mid-sized projects ($20k–$100k) usually favor the HELOC. Massive overhauls might justify a refinance.

- How long will the project take? Phased projects favor the revolving nature of the HELOC.

- What is my current rate? If your current rate is under 5%, a HELOC is almost always the mathematically superior choice to avoid losing that rate.

If you are unsure which path fits your financial profile, it is best to select a loan officer who can run a side-by-side comparison for you.

Taking the Next Step

Using your home equity is a powerful way to build wealth and improve your living space. Whether you are looking for an Indiana HELOC lender, a Kentucky HELOC lender, or guidance on investment properties in Florida and Illinois, the right strategy can save you thousands in interest and fees.

Stop guessing about your equity and start using it.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664