Buying high-end real estate in California often requires financing that goes beyond standard limits. Because home prices in cities like Los Angeles, San Francisco, and San Diego frequently exceed a million dollars, most buyers find themselves looking for a jumbo mortgage.

Jumbo Loan: A mortgage that exceeds the conforming loan limits set by the Federal Housing Finance Agency (FHFA).

Application: You use this loan type to finance luxury properties that cost more than the maximum amount allowed for standard Fannie Mae or Freddie Mac loans.

Choosing the right lender is about more than just the interest rate. You need to look at down payment requirements, reserve assets, and the specific underwriting flexibilities offered by different institutions.

Regional Loan Limits in California

The conforming loan limit varies depending on the county where the property is located. In high-cost areas across California, these limits are significantly higher than the national baseline.

Conforming Loan Limit: The maximum dollar amount for a mortgage that government-sponsored enterprises will purchase.

Application: Knowing your local limit helps you identify exactly when your financing crosses into the jumbo category.

In 2024 and 2025, many California counties see these limits hit their ceiling.

- Los Angeles and Orange County: Jumbo territory typically begins for loans over $1,149,825.

- San Francisco and the Bay Area: High-cost limits often align with the LA market, requiring jumbo financing for anything above the $1.15M range.

- San Diego County: Financing becomes jumbo once you exceed approximately $1,104,000.

- Sacramento and Ventura: These areas have slightly lower limits but still frequently require jumbo products for luxury upgrades.

If you are looking at properties in Florida or Chicago, the thresholds are different. Florida Jumbo Loans often trigger at the national baseline of $766,550 in many counties, though high-cost areas like Monroe County are higher. Similarly, Chicago Jumbo Loans typically apply to any amount over that same national baseline.

Qualification Criteria for California Jumbo Loans

Because jumbo loans cannot be sold to Fannie Mae or Freddie Mac, lenders take on more risk. This means they will look closely at your financial profile to ensure you can manage a high-balance debt.

Debt-to-Income (DTI) Ratio: A percentage that shows how much of your monthly gross income goes toward paying debts.

Benefit: Keeping this ratio below 43% helps you qualify for the most competitive jumbo interest rates.

Credit Score Requirements

Most jumbo lenders in California require a minimum credit score of 680. However, to access the best pricing and lower down payment options, a score of 720 or higher is usually preferred.

Down Payment Minimums

While conventional loans allow for as little as 3% down, jumbo loans traditionally required 20%. Today, some specialized programs allow for 10% or even 5% down for highly qualified buyers.

Cash Reserves

Lenders want to see that you have enough liquid assets to cover your mortgage payments if your income temporarily stops. This is often referred to as "reserve requirements."

Reserves: Liquid assets (cash, stocks, or retirement funds) available to the borrower after the down payment and closing costs are paid.

Application: Lenders may require 6 to 12 months of mortgage payments held in a verified account to approve a high-balance loan.

Explore our mortgage calculators to see how different down payment amounts affect your monthly jumbo payment.

Comparing Top California Jumbo Loan Programs

Not every jumbo loan is structured the same way. You should choose a program based on your long-term financial goals and current cash flow.

Traditional Fixed-Rate Jumbo

These are the most common and provide stability. You get a set interest rate for 15 or 30 years.

Best For: Homeowners who plan to stay in their luxury property for more than a decade.

Adjustable-Rate Mortgages (ARM)

Jumbo ARMs often offer lower initial interest rates compared to fixed-rate options. These are usually fixed for the first 5, 7, or 10 years.

Best For: High-net-worth individuals who plan to sell or refinance before the rate adjusts.

Interest-Only Jumbo Loans

This program allows you to pay only the interest for a set period, typically the first 10 years.

Benefit: It lowers your monthly obligation, allowing you to reinvest that cash into other business ventures or investments.

Access more details on interest-only mortgage options to see if this strategy fits your portfolio.

Non-QM and Alternative Jumbo Strategies

Standard jumbo loans require "full documentation," meaning W-2s, tax returns, and pay stubs. If you are self-employed or a real estate investor, you might need a different path.

Non-QM Loan: A "Non-Qualified Mortgage" that does not follow the standard federal guidelines for income verification.

Application: Self-employed borrowers can use bank statements to prove income rather than tax returns.

Bank Statement Loans

For entrepreneurs in California and Florida, bank statement loans allow you to qualify based on the average deposits into your business or personal accounts over 12 to 24 months.

DSCR Loans for Luxury Rentals

If you are purchasing a high-end property as a short-term rental or Airbnb, you might use a DSCR loan.

DSCR (Debt Service Coverage Ratio): A metric used to determine if a property’s rental income covers its mortgage debt.

Benefit: You can qualify for the loan based on the property's projected income rather than your personal employment history.

Jump in and learn about loan programs that cater to investors.

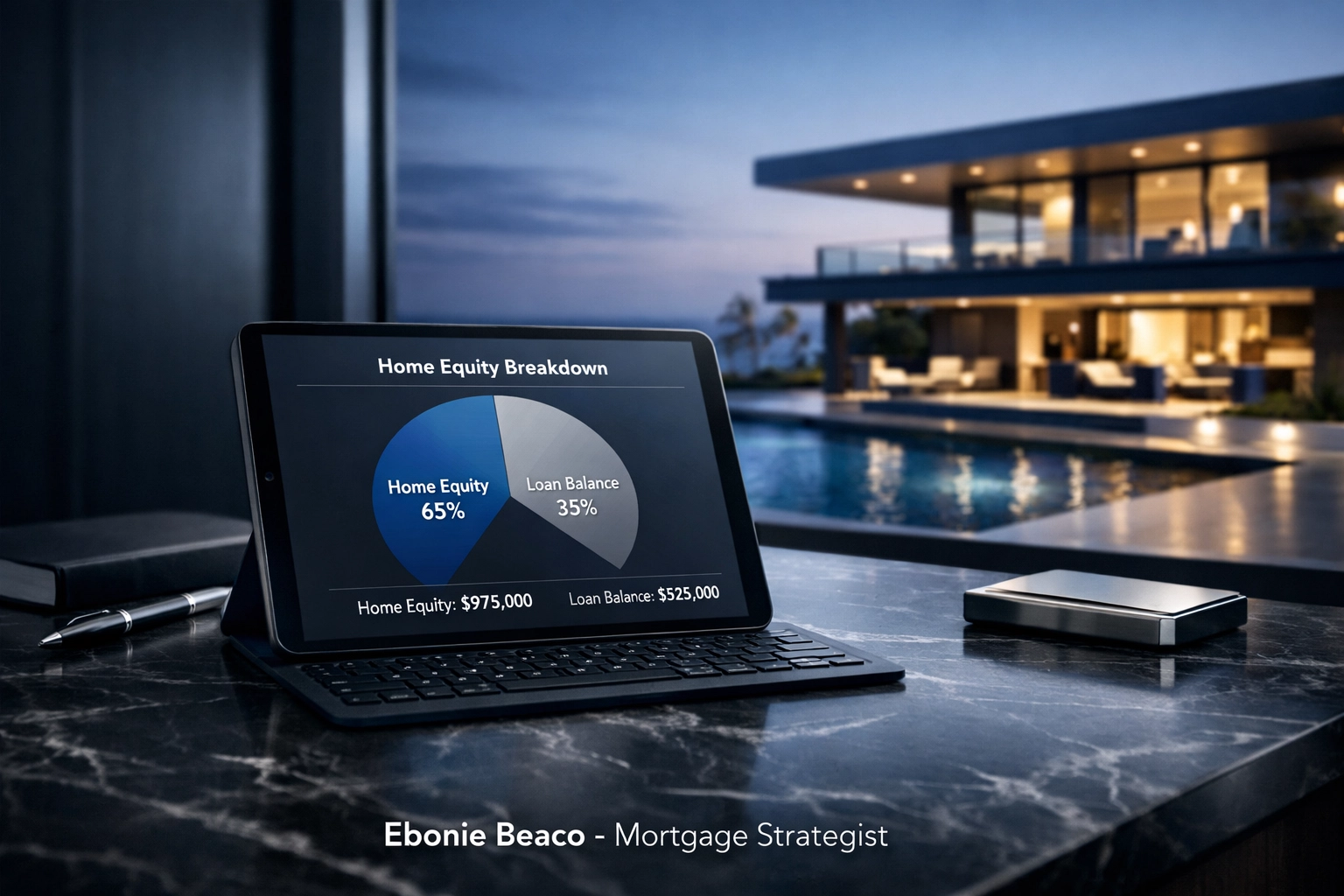

Financial Example: A $2 Million Purchase in Los Angeles

Let's look at how a jumbo loan works in a real-world scenario. Suppose you are buying a home in Los Angeles for $2,000,000.

- Purchase Price: $2,000,000

- Down Payment (15%): $300,000

- Loan Amount: $1,700,000

- Interest Rate: 6.5% (Estimated)

- Closing Costs (2%): $40,000

In this scenario, the lender might require 12 months of reserves. If your monthly principal, interest, taxes, and insurance (PITI) is $12,500, you would need to show an additional $150,000 in liquid assets after your $300,000 down payment.

This visual breakdown shows how much liquidity is required to secure high-end financing in a competitive market like California or Florida.

Closing Costs and Transparency

Jumbo loan closing costs in California typically range from 1% to 2% of the total loan amount. These include appraisal fees, title insurance, and origination charges.

Title Insurance: A policy that protects the lender and buyer against losses from defects in the property title.

Application: On a multi-million dollar transaction, this ensures there are no hidden liens or ownership disputes from the past.

Transparency is a core value at Home Loans Network. We encourage you to review the loan process so you know exactly what to expect from application to funding.

Choosing Your Lender Strategically

When comparing lenders for California Jumbo Loans, don't just look at the big banks. Credit unions and specialized mortgage brokerages often have "portfolio" products.

Portfolio Loan: A loan that a lender keeps on their own books rather than selling it on the secondary market.

Benefit: This gives the lender the flexibility to approve unique situations, such as buyers with high assets but low taxable income.

Compare these factors when vetting your options:

- Prepayment Penalties: Ensure the loan does not charge you for paying it off early.

- Appraisal Quality: High-end properties need appraisers who understand luxury markets.

- Turnaround Time: In markets like Miami, Atlanta, or San Francisco, a slow closing can lose you the deal.

Specialized Financing for Multi-State Investors

Many of our clients own property in California but also look for Florida Jumbo Loans or opportunities in the Chicago luxury market. Each state has different property tax structures and insurance requirements that impact your DTI.

For example, Florida has no state income tax, which can help your debt-to-income ratio, but homeowners insurance in coastal areas can be higher than in many California suburbs. Our team can help you navigate these regional nuances.

If you are ready to see which high-balance program fits your financial profile, you can select a loan officer who specializes in your target market.

Final Steps in the Jumbo Journey

Securing a jumbo loan is a complex process that requires preparation. Start by gathering your last two years of tax returns, two months of bank statements, and a detailed list of your assets and liabilities.

LTV (Loan-to-Value): The ratio of the loan amount to the appraised value of the property.

Application: Most jumbo lenders prefer an LTV of 80% or lower, though some programs go higher for primary residences.

Review our mortgage basics to brush up on terminology before you start your application.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664