Finding your dream home in Florida often means looking at properties that carry a premium price tag.

Whether you are eyeing a waterfront estate in Miami, a modern condo in downtown Tampa, or a sprawling property in Orlando, the price often climbs above the standard lending limits.

This is where Florida Jumbo Loans come into play.

In this guide, we will break down exactly how these high-balance loans work, what you need to qualify in 2026, and how to navigate the luxury market with confidence.

What is a Jumbo Loan?

A Jumbo Loan is a type of mortgage that exceeds the conforming loan limits set by the Federal Housing Finance Agency (FHFA).

Because these loans are too large to be purchased by Fannie Mae or Freddie Mac, they are considered non-conforming.

Lenders keep these loans on their own books or sell them to private investors, which means the rules for qualifying are often stricter than a standard loan.

Explore our Jumbo Loans page to see the foundational requirements.

The 2026 Conforming Loan Limits in Florida

To know if you need a jumbo loan, you first have to look at the conforming limits for your specific county.

For the year 2026, the FHFA has adjusted these limits to reflect the rising property values across the country.

Most Florida Counties: The baseline limit for a single-family home is $832,750.

Monroe County (The Florida Keys): This is considered a high-cost area, with a limit reaching $990,150.

If your loan amount is even one dollar over these thresholds, you are officially in jumbo territory.

This same logic applies if you are looking at California Jumbo Loans or Chicago Jumbo Loans, where limits can vary significantly based on local market costs.

Key Requirements to Qualify for a Florida Jumbo Loan

Since the lender is taking on more risk with a larger loan amount, they want to see a rock-solid financial profile.

Credit Score Standards

Your credit score is the first thing a lender looks at.

For a jumbo loan, a minimum FICO score of 700 is typically the baseline.

If you are looking to secure the most competitive rates or are borrowing over $2 million, many lenders will look for a score of 740 or higher.

The Down Payment Reality

Gone are the days when you could get a jumbo loan with 3% down.

Expect to put down at least 10% to 20%.

Putting 20% down is generally the gold standard because it eliminates the need for private mortgage insurance (PMI) and often unlocks lower interest rates.

Debt-to-Income (DTI) Ratio

Lenders want to ensure you aren't overextended.

While conventional loans might allow a DTI up to 50%, jumbo lenders usually cap this at 43%.

This ensures you have plenty of breathing room for property taxes, insurance, and lifestyle expenses.

Cash Reserves

Lenders will ask to see "reserves," which is liquid cash left over after you close on the house.

For Florida Jumbo Loans, it is common to require 6 to 12 months of mortgage payments (Principal, Interest, Taxes, and Insurance) in a bank or brokerage account.

Jumbo Loans for Real Estate Investors

Many people assume jumbo loans are only for primary residences, but they are incredibly useful for investors too.

If you are building a portfolio of high-end short-term rentals in Miami or luxury condos in Destin, jumbo financing is a powerful tool.

Investors often use these to acquire "trophy" properties that command high nightly rates on platforms like Airbnb.

Jump in and learn more about Airbnb and Short-Term Rental Financing options.

For those focusing on cash flow rather than just personal income, you might also consider DSCR Investor Loans, which focus on the property's income rather than your tax returns.

Comparing Conventional vs. Jumbo Loans

| Feature | Conventional Loan | Jumbo Loan |

|---|---|---|

| Loan Limit (2026) | Up to $832,750 (Base) | Above $832,750 |

| Credit Score | 620+ | 700+ |

| Down Payment | 3% - 20% | 10% - 20% |

| DTI Ratio | Up to 50% | Typically 43% or lower |

| Reserves | 0 - 3 months | 6 - 12 months |

| Underwriting | Automated | Manual / Intensive |

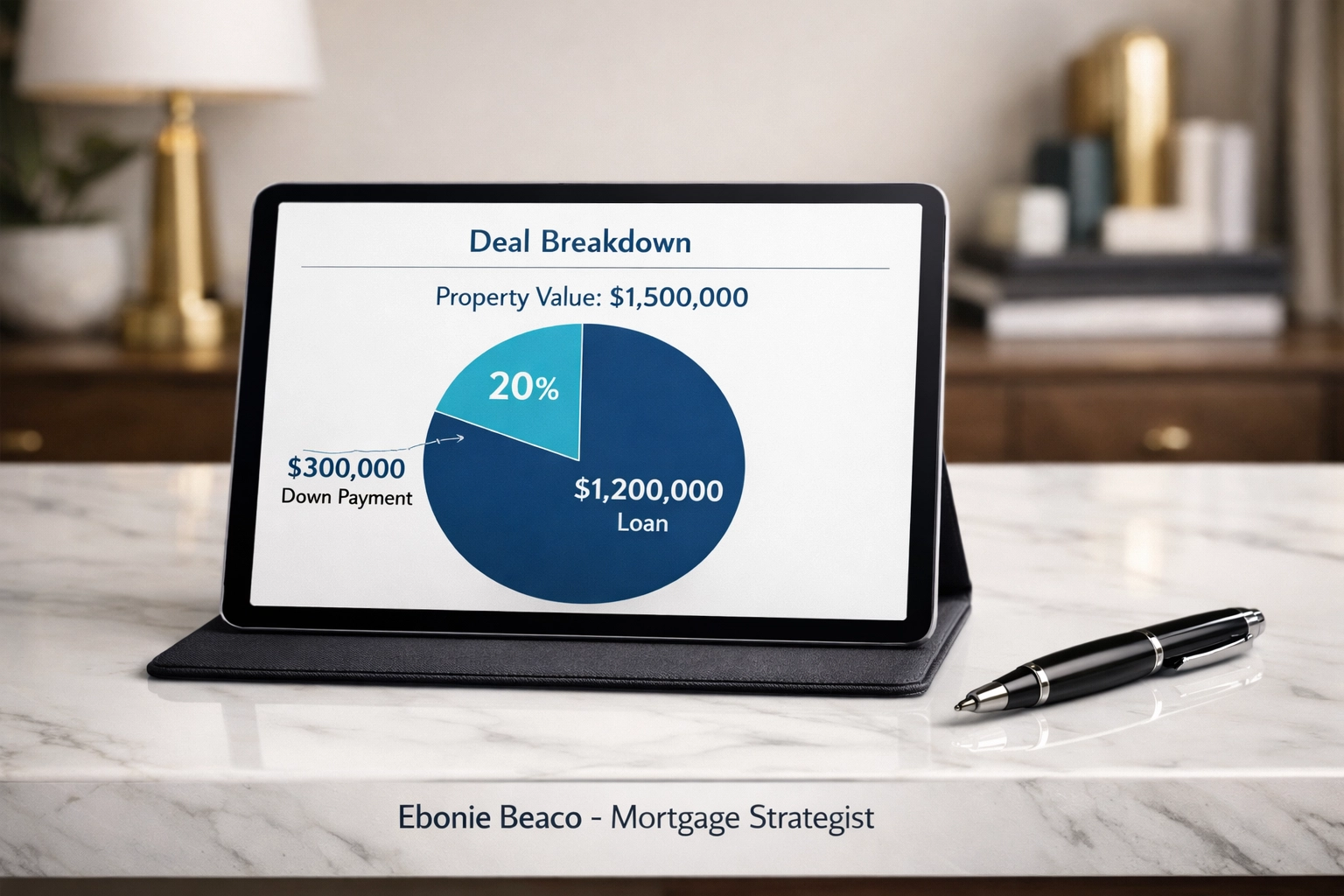

A Real-World Financial Example

Let’s look at how a jumbo loan structure might look for a luxury purchase in a city like Fort Lauderdale or even a high-end suburb of Atlanta.

The Scenario:

- Property Purchase Price: $1,500,000

- Down Payment (20%): $300,000

- Loan Amount: $1,200,000

- Interest Rate: 6.75%

- Estimated Monthly Payment (P&I): $7,783

In this case, the buyer would need to show they have the $300,000 for the down payment, plus closing costs, and likely another $60,000 to $90,000 in liquid reserves to satisfy the lender's safety requirements.

Strategic Options: Interest-Only Jumbo Loans

For high-net-worth individuals or investors with fluctuating income, an Interest-Only Mortgage can be a smart move.

This allows you to pay only the interest for a set period (usually 5 to 10 years), keeping your monthly cash flow higher.

This is a popular strategy in the luxury markets of California and Florida, where buyers may plan to sell or refinance before the principal repayment period begins.

Access more details on Interest-Only Mortgages to see if this fits your strategy.

The Importance of Manual Underwriting

Unlike standard loans that go through an automated system, jumbo loans involve manual underwriting.

A human being will look at every line of your tax returns, bank statements, and asset reports.

They are looking for stability and consistency.

If you are self-employed, you might find that Bank Statement Loans are a better fit if your tax returns don't tell the full story of your success.

Navigating Different Markets: FL, CA, and GA

While this guide focuses on Florida, the luxury market is booming in other areas too.

California Jumbo Loans are common in cities like Los Angeles and San Francisco, where almost every single-family home exceeds the conforming limit.

Similarly, we see a huge demand for jumbo financing in Atlanta’s high-end neighborhoods like Buckhead.

Each state has its own nuances regarding property taxes and insurance (like flood insurance in Florida), so working with a strategist who understands these regional variations is key.

Pro Tips for Jumbo Loan Success

- Get Pre-Approved Early: Because the documentation is extensive, don't wait until you find the house. Get your paperwork reviewed upfront.

- Check Your Appraisal: Jumbo properties are unique, and appraisals can be tricky. Sometimes lenders require two separate appraisals for loans over a certain amount (e.g., $2 million).

- Keep Your Credit "Frozen": Once you apply, don't open new credit cards or buy a new car. Jumbo lenders often do a final credit refresh right before closing.

- Verify Your Reserves: Make sure your reserve funds are in accounts that are easily documented. Transfers between multiple accounts can create a "paper trail" headache.

Why Transparency in Lending is Vital

At Home Loans Network, we believe in being transparent about the hurdles and the wins.

Jumbo loans aren't "harder" to get; they just require a higher level of preparation.

We work with buyers across Alabama, Arkansas, California, Florida, Georgia, Illinois, Indiana, Kentucky, Michigan, Missouri, and Virginia to find the right structure for their high-balance needs.

Whether you are looking for Fixed-Rate Mortgages or more complex Adjustable-Rate Mortgages, we can guide you clearly and confidently.

Do you have questions about a specific property or loan scenario?

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664