If you own a home in Florida, California, or Georgia, you are likely sitting on a goldmine of equity. While your home value has climbed over the last few years, your credit card balances might have done the same. Carrying high-interest debt is like trying to swim with a weighted vest on. No matter how hard you paddle, the interest charges keep pulling you under.

Many homeowners feel stuck between a rock and a hard place. They don't want to touch their low-interest first mortgage, but they are tired of seeing 20%, 25%, or even 29% interest rates on their monthly statements. This is where a strategic financial tool comes into play.

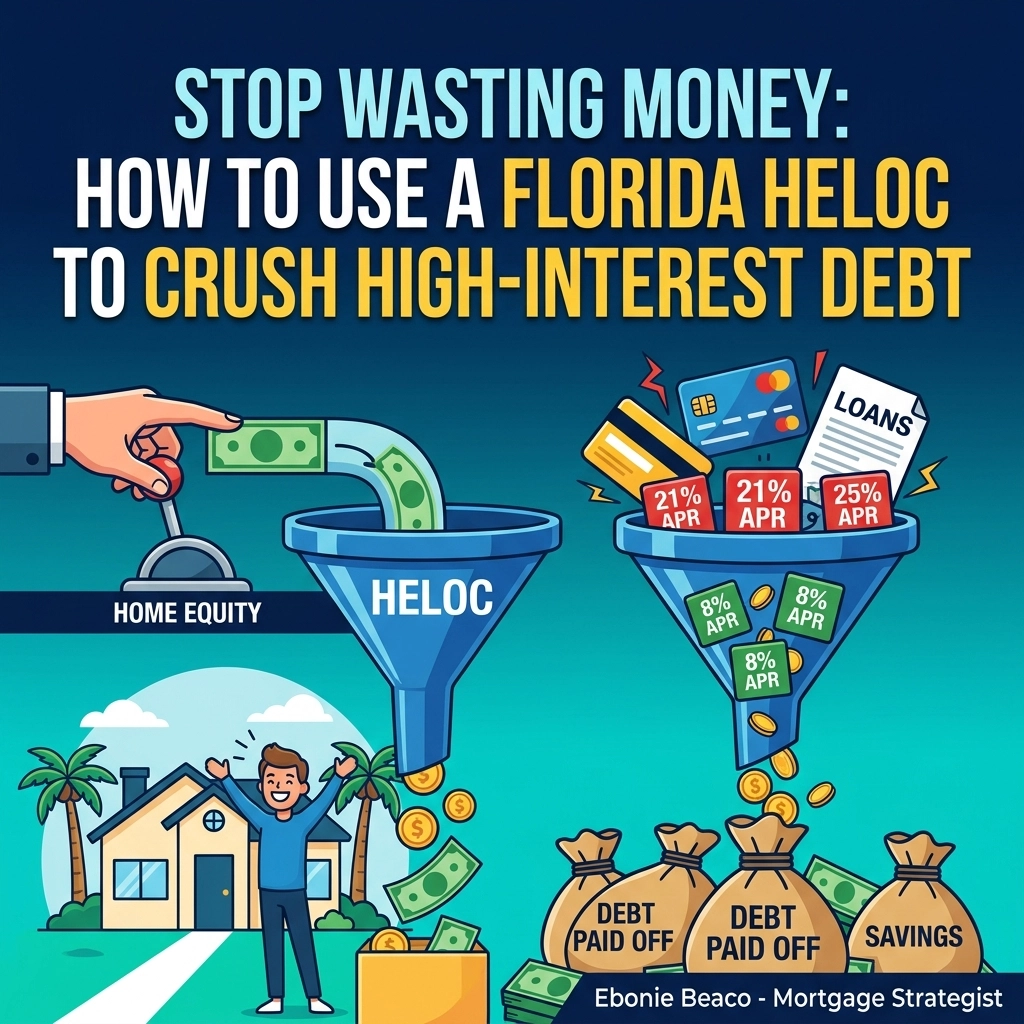

The Secret Home Equity Drain: Why Your Credit Cards Are Winning

Every month you carry a balance on a high-interest credit card, you are effectively draining the wealth you’ve built in your home. You work hard to pay down your mortgage, but the interest you pay to credit card companies cancels out those gains.

HELOC (Home Equity Line of Credit): A revolving line of credit that allows you to borrow against the equity in your home.

- Practical Application: It functions like a credit card with a much higher limit and a significantly lower interest rate, secured by your property.

By using a Florida HELOC to pay off those balances, you stop the bleeding. Instead of paying 24% interest to a big bank, you might pay 7% or 8% on a line of credit. This shift immediately increases your monthly cash flow.

How a Florida HELOC Works for Debt Consolidation

The process is more straightforward than most people realize. You don't have to refinance your entire mortgage. If you have a 3% or 4% rate on your primary loan, you should keep it. A HELOC sits in the "second position," meaning it is a separate loan that runs alongside your current mortgage.

Explore the loan process to see how quickly you can move from application to funding. Generally, the steps look like this:

- Calculate Your Equity: Determine the current value of your home minus your existing mortgage balance.

- Apply for the Line: A lender reviews your credit, income, and property value.

- Draw Funds: Once approved, you use the funds to pay off every high-interest credit card and personal loan you own.

- Repay at a Lower Rate: You make one monthly payment to the HELOC at a much lower interest rate.

Jump in and compare your options by looking at different loan programs that offer flexibility for your specific financial profile.

Comparing the Numbers: A Real-World Scenario

Let’s look at how this works for a typical homeowner in a market like Orlando, Florida, or even a California HELOC scenario in San Diego.

Assume your home is worth $500,000. Your current mortgage balance is $300,000. Most lenders will allow a Combined Loan-to-Value (CLTV) of up to 80% or 85%.

The Calculation:

- Home Value: $500,000

- 85% CLTV Limit: $425,000

- Current Mortgage: $300,000

- Available HELOC Limit: $125,000

In this example, the homeowner has access to $125,000. If they have $40,000 in credit card debt at a 22% interest rate, their monthly interest charge alone is roughly $733. If they move that $40,000 to a HELOC at 8.5%, the monthly interest charge drops to approximately $283.

That is an immediate savings of $450 per month. That money stays in your pocket rather than going to a credit card company.

Geographic Opportunities: From California to Virginia

While we are focusing on the Florida HELOC, these strategies apply across many states. Whether you are looking for a Georgia HELOC lender or exploring options in Michigan, Indiana, or Illinois, the mechanics remain the same.

- California HELOC: Home values in cities like Los Angeles or San Francisco are exceptionally high, often providing massive equity pools for debt consolidation or even further real estate investment.

- Georgia HELOC Lender: Markets in Atlanta are seeing steady growth, making it a prime location for homeowners to tap into their equity to renovate or consolidate debt.

- Virginia and Kentucky: Homeowners in these regions often use HELOCs to manage life's larger expenses without disrupting their primary low-rate mortgage.

Access our mortgage calculators to run your own numbers based on your specific city and home value.

The Draw Period vs. The Repayment Period

It is vital to understand how a HELOC is structured over time. It typically consists of two distinct phases.

Draw Period: The initial timeframe (usually 10 years) during which you can withdraw money and often pay only the interest on the balance.

- Practical Benefit: This offers the lowest possible monthly payment while you focus on clearing other financial hurdles.

Repayment Period: The phase after the draw period ends (usually 15 to 20 years) where you can no longer withdraw funds and must pay back both principal and interest.

- Practical Benefit: This ensures the loan is fully paid off by the end of the term, building your equity back up to 100%.

During the draw period, the flexibility is unmatched. If you pay down the balance, those funds become available to use again, much like a credit card. This makes it a popular tool for real estate investors in Alabama or Arkansas who need quick access to cash for a down payment on a rental property.

Managing Your Debt-to-Income (DTI) Ratio

When you consolidate high-interest debt into a HELOC, you aren't just saving on interest; you are potentially improving your credit profile. Credit cards look at "utilization." If your cards are maxed out, your credit score suffers.

When you pay off those cards with a HELOC, your revolving credit utilization on your credit cards drops to zero. Even though you still owe the money on the HELOC, the credit scoring models often view mortgage-related debt more favorably than credit card debt.

DTI (Debt-to-Income): A calculation that divides your total monthly debt payments by your gross monthly income.

- Application: A lower DTI makes it easier to qualify for future loans, such as conventional loans or jumbo loans for an investment property.

Transparency: Is a HELOC Right for You?

We believe in being transparent. A HELOC is a powerful tool, but it requires discipline. Because the loan is secured by your home, failing to make payments puts your property at risk.

If you are the type of borrower who will pay off the credit cards and then immediately run the balances back up again, a HELOC is not the right move. However, for the disciplined homeowner or the savvy investor in Missouri or Virginia, it is the ultimate shortcut to financial freedom.

The interest on a HELOC may also be tax-deductible if the funds are used to "buy, build, or substantially improve" the home that secures the loan. Always consult with a tax professional to see how this applies to your specific situation.

Leveraging Equity for Investment

Many of our clients in Illinois and California don't just stop at debt consolidation. Once the high-interest debt is gone, they use the remaining line of credit as a "ready-to-go" fund for real estate investing.

Imagine finding a distressed property in Birmingham, Alabama. Instead of waiting weeks for a hard money loan, you can draw from your Florida HELOC or California HELOC to make a cash offer. This speed is why many successful investors keep a HELOC open even if they don't plan on using it immediately.

Taking the Next Step

Stop letting high-interest rates erode your hard-earned equity. Whether you are looking for a Georgia HELOC lender or want to see how much you can access from your home in Michigan, the first step is a clear strategy.

You don't have to navigate the complexities of equity alone. We provide the guidance you need to compare options and choose the path that aligns with your long-term wealth goals.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664

Consolidating debt is the first step toward building a real estate empire, but there is an even more powerful way to use your home’s value. What if you could skip the monthly payments entirely while still accessing your cash? Next time, we’ll dive into a strategy that most banks don't want you to know about...