California homeowners sit on a mountain of equity. Between the coastal appreciation in cities like San Diego and the steady growth in the Central Valley, your home is likely your most valuable financial tool. If you are looking to tap into that value without touching your low-rate first mortgage, a Home Equity Line of Credit (HELOC) is often the smartest move.

This guide explores the specific nuances of the California HELOC market while also providing context for property owners in Florida and Georgia who are looking for similar strategies. Whether you want to fund a massive kitchen remodel or consolidate high-interest credit card debt, understanding these seven points will help you navigate the process with confidence.

1. Understanding the LTV Ceiling

Lenders use a specific metric to decide how much you can borrow against your home. This is known as the Combined Loan-to-Value (CLTV) ratio.

CLTV (Combined Loan-to-Value): The total of all loans on a property divided by the property's appraised value.

Application: You use this figure to determine the maximum credit line a lender will extend after accounting for your primary mortgage.

In California, most lenders cap your CLTV at 80% or 85%. Because home values are so high in the Golden State, even a small percentage of equity can represent hundreds of thousands of dollars.

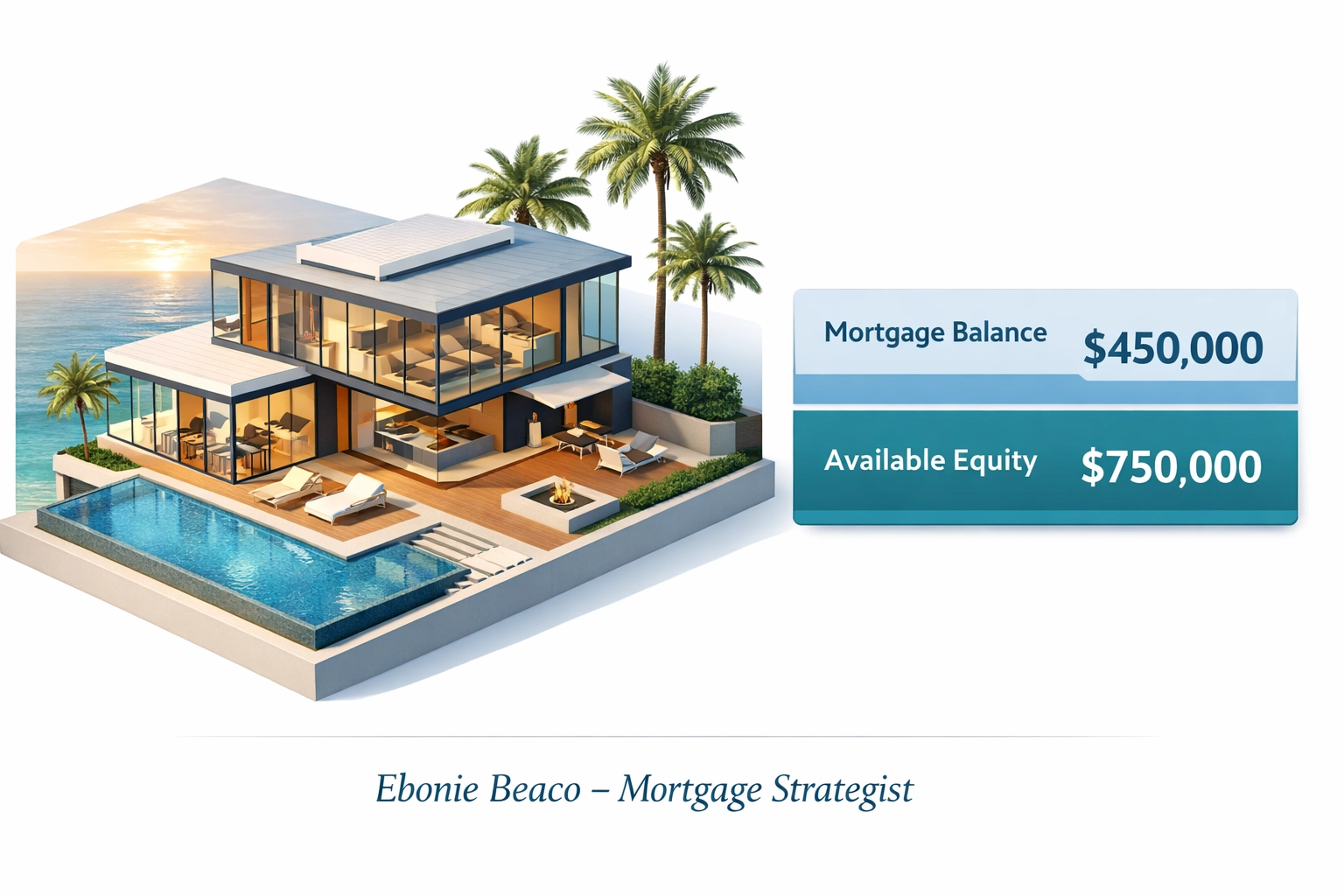

California Equity Calculation Example

Imagine you own a home in Los Angeles valued at $950,000. Your current mortgage balance is $550,000. If a lender allows an 85% CLTV, here is how the math works:

- $950,000 (Home Value) x 0.85 = $807,500 (Maximum Total Debt Allowed)

- $807,500 - $550,000 (Current Mortgage) = $257,500 (Available HELOC Limit)

2. The Flexibility of the Draw Period

A HELOC functions much like a credit card, but it is secured by your home. This revolving nature is what makes it different from a standard home equity loan.

Draw Period: The initial phase of a HELOC where you can access funds and typically make interest-only payments.

Application: Use this period to pay for ongoing expenses, like a multi-phase renovation, while keeping your monthly costs low.

Most HELOCs offer a 10-year draw period followed by a 20-year repayment period. During those first 10 years, you only pay interest on the amount you actually spend. If you have a $100,000 line but only use $20,000 for a new roof, you only owe interest on that $20,000. Explore different loan programs to see how draw periods vary by lender.

3. Credit Score Thresholds for the Best Rates

While you can find options with lower scores, the most competitive California HELOC rates are reserved for those with a 680 or higher.

Credit Score: A numerical expression based on a level analysis of a person's credit files.

Application: Maintaining a high score ensures you receive lower interest margins above the prime rate.

Lenders in competitive markets like Atlanta or Miami look at your credit history to assess risk. If you are working with a Georgia HELOC lender, you may find that a score above 720 unlocks significantly better terms. Before applying, jump in and check your current standing to ensure you are positioned for the best possible deal.

4. DTI Requirements and Income Verification

Your income must be sufficient to support both your primary mortgage and the new HELOC. Lenders measure this through your Debt-to-Income (DTI) ratio.

DTI (Debt-to-Income): The percentage of your gross monthly income that goes toward paying debts.

Application: This ratio helps a mortgage strategist determine if you can comfortably afford a new line of credit.

For a California HELOC, lenders typically want to see a DTI below 43%. This calculation includes your new HELOC payment at its fully indexed rate, not just the interest-only draw payment. If you are self-employed, you might need to provide two years of tax returns or explore non-QM mortgage loans that offer alternative documentation options.

5. Tax Deductibility and Home Improvements

Many homeowners choose a HELOC because of the potential tax benefits. However, the rules changed significantly a few years ago.

Tax Deductibility: The ability to subtract certain expenses from your taxable income.

Application: You may deduct HELOC interest if the funds are used to buy, build, or substantially improve the home that secures the loan.

If you are using a Florida HELOC to install hurricane-impact windows or a new pool, the interest may be deductible. If you use those same funds to pay off a car or fund a vacation, that interest is generally not deductible. Always consult with a tax professional to confirm how these rules apply to your specific financial situation.

6. Comparing HELOCs to Cash-Out Refinancing

In a high-interest-rate environment, many California homeowners are hesitant to touch their primary mortgage. This is where the HELOC shines compared to a cash-out refinance.

Cash-Out Refinance: Replacing your existing mortgage with a new, larger loan and taking the difference in cash.

Application: This is ideal when your current mortgage rate is higher than or equal to current market rates.

If you currently have a 3% interest rate on your first mortgage, doing a cash-out refinance would mean trading that 3% for today’s market rate on the entire balance. A HELOC allows you to keep that 3% rate untouched while only paying the higher market rate on the smaller amount you borrow. Access our mortgage calculators to compare the total interest cost of both options.

7. Appraisal and Closing Timelines

The California real estate market moves fast, but securing a HELOC takes some patience. The process usually hinges on the appraisal.

Home Appraisal: An unbiased professional opinion of a home's value.

Application: The appraisal confirms the amount of equity available for the lender to secure the line of credit.

In high-demand areas like San Francisco or Chicago, scheduling an appraiser can take time. From the moment you submit your online forms, expect a timeline of 30 to 45 days to close. Some lenders offer "automated valuation models" (AVMs) that can speed up the process, but a full interior appraisal usually yields a higher value, which means more borrowing power for you.

Leveraging Equity in Other Markets

While this guide focuses on California, the strategy of using equity is universal.

- Florida HELOC: Homeowners in cities like Orlando or Tampa often use these lines to fund property upgrades that increase resale value in a competitive market.

- Georgia HELOC Lender: Investors in the Atlanta metro area frequently use HELOCs as "bridge" capital to fund the down payment on a new rental property or a fix-and-flip project.

Using a HELOC for debt consolidation is another powerful strategy. If you are carrying $50,000 in credit card debt at a 24% interest rate, moving that balance to a HELOC at 9% or 10% can save you thousands of dollars in interest every year.

Debt Consolidation Comparison Example

- Scenario A: $50,000 Credit Card Debt at 24% APR = ~$1,000/month in interest alone.

- Scenario B: $50,000 HELOC Balance at 9% APR = ~$375/month in interest.

- Result: A monthly savings of $625, which can be redirected toward paying down the principal balance faster.

Navigating the Process

The path to securing a HELOC involves several clear steps. You will need to gather your documentation, including recent pay stubs and your most recent mortgage statement. You can review the full loan process on our website to see what to expect from application to funding.

Choosing the right structure is vital. Some HELOCs offer a fixed-rate option, allowing you to lock in a portion of your balance at a set interest rate, protecting you from future market increases. This hybrid approach is popular in volatile markets where homeowners want the flexibility of a line of credit with the stability of a fixed payment.

Compare your options carefully. Not all HELOCs are created equal, and some may have annual fees or inactivity fees. Always read the legal disclosures and ask about any early closure penalties if you plan on selling your home in the near future.

Explore your equity options today by reaching out for a personalized scenario review.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664