You probably remember the feeling of signing your mortgage papers back in 2020 or 2021. Maybe you scored a rate of 2.75% or 3.25%. At the time, it felt like winning the lottery. Today, that low rate feels a bit different. While it keeps your monthly payment low, it also feels like a set of golden handcuffs.

You want to renovate the kitchen in your Chicago bungalow. You want to buy a rental property in Florida. Or perhaps you need to consolidate some high-interest credit card debt that has crept up over the last two years. Usually, you would just look into a home refinance to pull out some cash.

But there is a problem.

If you do a traditional cash-out refinance today, you lose that beautiful 3% rate and replace the entire balance with a rate that is likely double what you are currently paying. It is a financial move that rarely makes sense. Does this mean your equity is trapped until rates drop?

Not exactly. There is a strategic way to bypass this trap without touching your primary mortgage.

The Secret Mechanism That Keeps Your Primary Rate Intact

The "simple trick" isn't a loophole or a magic trick; it is a strategic use of a HELOC (Home Equity Line of Credit).

HELOC (Home Equity Line of Credit): A revolving line of credit secured by your home that allows you to borrow against your equity as needed.

Practical Application: You use a HELOC to access cash for a down payment on an investment property while keeping your 3% first mortgage exactly where it is.

When you use a HELOC, you are adding a second "layer" of debt on top of your existing mortgage. You are not replacing your first mortgage. You are simply inviting a second lender to the party. This allows you to keep your low-rate first mortgage locked in while only paying the current market rate on the specific amount of cash you actually draw from the line of credit.

Why a Cash-Out Refinance Could Be Your Biggest Financial Mistake

Many homeowners make the mistake of looking at the "blended rate" and thinking a refinance is fine. Let’s look at why that logic is often flawed in the current market.

If you have a $300,000 mortgage at 3% and you need $50,000 for a renovation, a cash-out refinance would result in a new $350,000 loan at roughly 6.5% or 7%. You are essentially "paying" an extra 4% interest on the original $300,000 just to get your hands on $50,000.

That is an expensive way to borrow money.

By contrast, a Michigan HELOC lender or a Virginia HELOC lender can set up a second lien. You keep the $300,000 at 3%. You only pay the higher interest rate on the $50,000 you actually spend. This keeps your overall interest expense significantly lower and protects your long-term wealth.

The Math Behind the Freedom: A Real-World Scenario

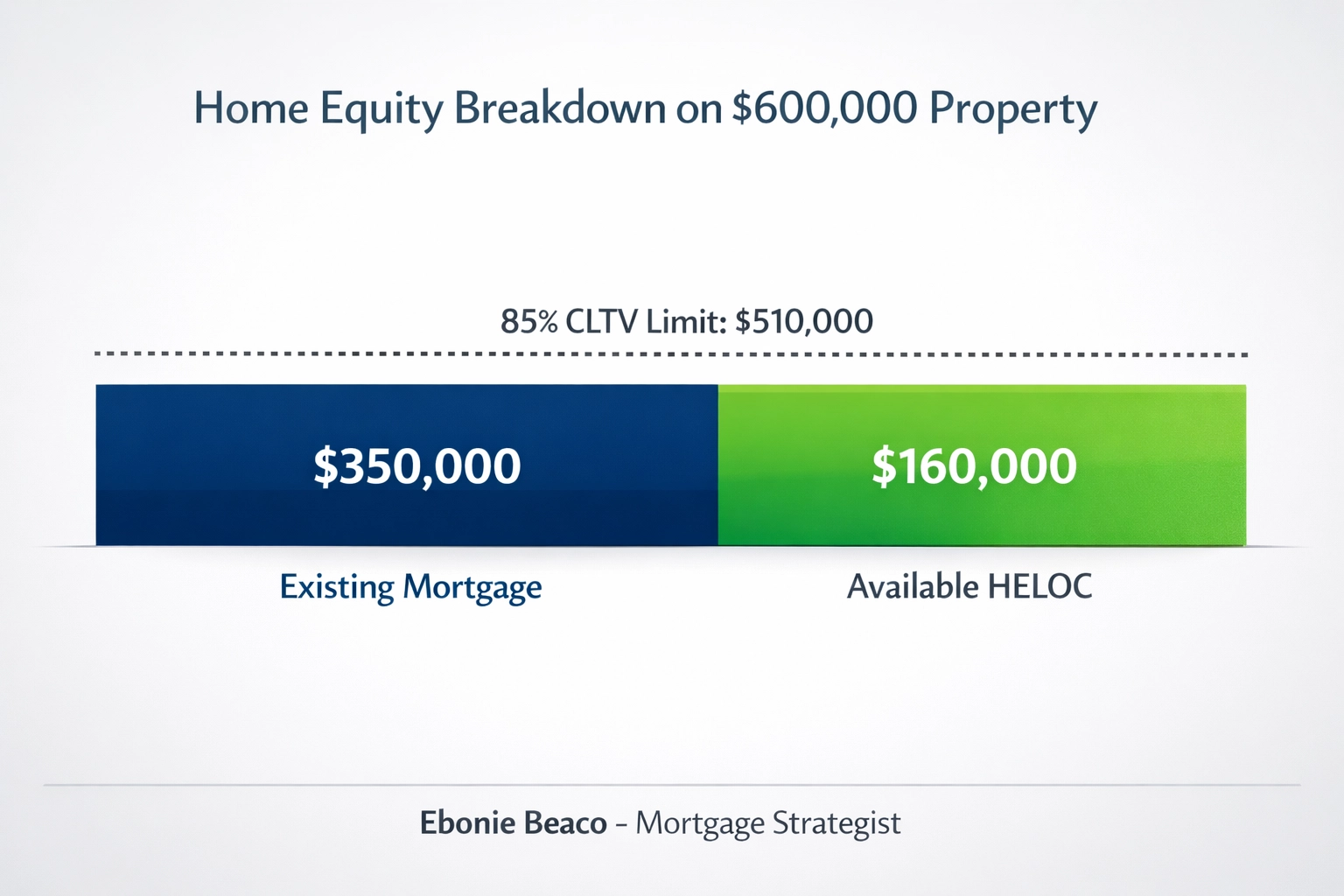

To understand how this works for a homeowner or an investor, we need to look at the numbers. Let’s imagine a homeowner in a growing market like Atlanta, Georgia or Virginia Beach.

Scenario:

- Current Home Value: $600,000

- Current Mortgage Balance: $350,000 (at 3.25%)

- Desired Cash for Investment: $100,000

In this situation, the homeowner wants to maintain their low payment on the $350,000. Most lenders will allow a CLTV (Combined Loan-to-Value) up to 80% or 85% for a primary residence.

CLTV (Combined Loan-to-Value): The ratio of all loans on a property compared to the property's total appraised value.

Practical Application: Lenders use CLTV to determine the maximum amount you can borrow across all mortgages on a single home.

As shown in the calculation, with an 85% CLTV limit on a $600,000 home, the total allowable debt is $510,000. Since the first mortgage is $350,000, the homeowner has access to a HELOC of up to $160,000. They can take their $100,000, keep their 3.25% rate on the bulk of their debt, and only pay interest on the $100,000 they use.

Why Savvy Investors Are Ignoring Refinancing Altogether

Real estate investors in states like Indiana, Missouri, and Arkansas are increasingly using HELOCs as "ready-to-go" capital. In the world of real estate investing, speed is often more important than the interest rate itself.

DSCR (Debt Service Coverage Ratio): A metric used by lenders to qualify a property based on its ability to cover mortgage payments with its own rental income.

Practical Application: Investors use HELOC funds for a down payment on a property, then use a DSCR loan to finance the rest, ensuring the property pays for itself.

If you are a landlord in Michigan looking to add a duplex to your portfolio, having a HELOC in place means you can make a cash-offer or a heavy down payment without waiting 45 days for a new cash-out refinance to close. You are using your "trapped" equity to build a larger portfolio.

The Hidden Advantage of the "Draw Period"

One of the most transparent benefits of a HELOC that many homeowners overlook is the flexibility of the draw period.

Draw Period: The initial phase of a HELOC (usually 10 years) during which the borrower can take money out and typically only owes interest-only payments.

Practical Application: This allows you to have a massive "emergency fund" or "investment fund" available without paying a dime in interest until you actually use the money.

Explore the loan process to see how simple it is to get this safety net in place. Unlike a standard loan where you get a lump sum and start paying interest on the whole amount immediately, a HELOC is there when you need it and silent when you don’t.

Local Market Insights: From California to Florida

The strategy of using a HELOC varies slightly depending on where you live. In high-appreciation states like California or parts of Florida, equity has skyrocketed over the last five years.

- California: Homeowners in cities like San Diego or San Francisco often have massive amounts of equity but very high cost of living. A HELOC provides a "pressure valve" to access cash for ADU (Accessory Dwelling Unit) construction, which can then generate rental income.

- Florida and Georgia: These markets have seen significant influxes of new residents. Homeowners here are using HELOCs to fund renovations that further boost their property values in a competitive market.

- Illinois (Chicago): With property taxes being a significant factor, keeping a low primary mortgage rate is essential for maintaining monthly affordability. A HELOC allows Chicagoans to handle major repairs or upgrades without blowing up their monthly budget.

Is a HELOC Right for Your Specific Situation?

While the HELOC is a powerful tool to break free from the "golden handcuffs" of a low rate, it is not a one-size-fits-all solution. You should consider a HELOC if:

- Your current mortgage rate is below 4.5%.

- You have at least 15% to 20% equity in your home.

- You have a specific use for the money, such as home improvement or a down payment on an investment property.

- You prefer a flexible payment structure during the initial years of the loan.

Jump in and use our mortgage calculators to see how an additional payment might look for your specific budget.

How to Access Your Equity Without the Stress

The process of securing a HELOC is generally faster and involves fewer closing costs than a full refinance. Because you aren't replacing your primary mortgage, the paperwork is often more streamlined.

As a Michigan HELOC lender and a Virginia HELOC lender, we see many homeowners hesitate because they fear the complexity. The reality is that modern lending has made this process incredibly accessible. You can start by filling out online forms to get an idea of your home's current value and your available equity.

Breaking Free Starts With a Conversation

Your home is likely your largest financial asset. Letting that equity sit idle while you struggle with high-interest debt or miss out on investment opportunities is a choice, not a requirement. You do not have to give up your 3% rate to live the life you want or grow your wealth.

The "simple trick" is simply choosing the right tool for the job. In a high-rate environment, the HELOC is the surgical tool that lets you extract what you need without damaging the healthy financial foundation you’ve already built.

Explore your options and see how much equity you can unlock today.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664