If you live in a high-appreciation market like Los Angeles, San Diego, or even the rapidly growing suburbs of Atlanta and Miami, you are likely sitting on a goldmine.

Your home equity has probably increased significantly over the last few years.

Big banks know this, and they are eager to help you tap into it: but often only on their terms.

Most traditional lenders want you to pursue a full Cash-Out Refinance, which might force you to give up a record-low interest rate on your primary mortgage.

There is a better way to leverage your wealth without resetting your entire financial foundation.

The Secret Home Equity Drain: Why Banks Push Refinances

Banks often steer homeowners toward products that generate the most profit for the institution rather than the most savings for the borrower.

When you hear a lender suggest a "simple" refinance to consolidate debt, they might be ignoring the fact that you currently hold a 3% or 4% interest rate.

Replacing that entire loan with a new one at current market rates can cost you tens of thousands of dollars in interest over the life of the loan.

A California HELOC allows you to keep your low-rate first mortgage exactly where it is.

You simply stack a second line of credit on top of it, giving you access to cash while keeping your primary housing cost stable.

Explore your options on our Home Refinance page to see how a second lien compares to a full reset.

Understanding the HELOC Framework

HELOC (Home Equity Line of Credit): A revolving line of credit secured by the equity in your primary residence or investment property.

Practical application: Think of this as a high-limit credit card backed by your home, where you only pay interest on the amount you actually spend.

Draw Period: The initial phase of a HELOC, usually lasting 10 years, during which you can access funds and typically make interest-only payments.

Practical application: This period offers maximum flexibility for homeowners who need to fund ongoing projects like renovations or college tuition.

Repayment Period: The phase following the draw period where you can no longer take out money and must pay back both principal and interest.

Practical application: Knowing when your repayment period starts helps you avoid "payment shock" when your monthly obligation suddenly increases.

CLTV (Combined Loan-to-Value): The ratio of all loans on a property compared to its total appraised value.

Practical application: If your home is worth $1,000,000 and you owe $600,000, a lender allowing an 80% CLTV would let you borrow up to a total of $800,000 across all loans.

The Multi-State Equity Shuffle: Investing from CA to AR

Homeowners in California are increasingly using their equity to become interstate real estate investors.

If you have $300,000 in accessible equity in a California home, that capital can go much further in markets like Arkansas, Alabama, or Missouri.

By securing a California HELOC, you can use those funds as a 20% or 25% down payment on multiple rental properties in the Midwest or South.

This strategy allows you to diversify your portfolio across different geographic regions while your primary residence continues to appreciate.

Many of our clients use this tactic to fund DSCR Investor Loans, which qualify based on the rental income of the property rather than personal income.

Jump in and learn more about Mortgage Basics to see how equity can fuel your investment journey.

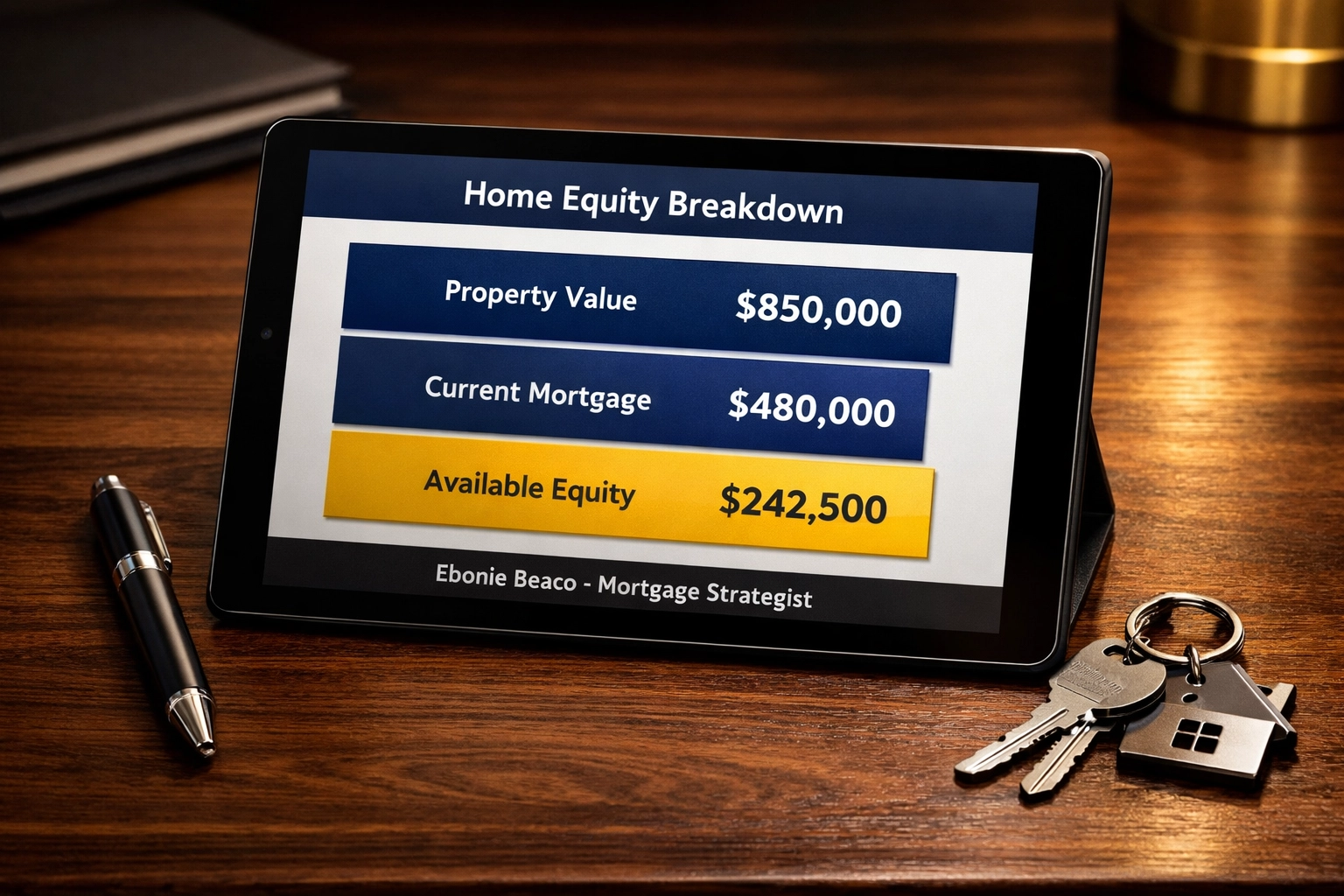

Real-World Equity Access Example

Let’s look at how a typical homeowner in a market like Orange County or a high-growth area in Florida might calculate their available funds.

- Property Value: $850,000

- Current Mortgage Balance: $480,000

- Maximum CLTV (85%): $722,500

- Available HELOC Limit: $242,500 ($722,500 minus $480,000)

In this scenario, the homeowner can access nearly a quarter-million dollars without touching their original $480,000 loan or its low interest rate.

This liquidity can be used for a Fix and Flip project in Georgia or to purchase a short-term rental in Virginia.

Access our Mortgage Calculators to run these numbers for your specific situation.

The "Fixed-Rate" Secret Most Lenders Hide

Most people assume all HELOCs are variable-rate products that fluctuate with the Prime Rate.

While the line of credit is variable by nature, many "hidden" programs allow for a Fixed-Rate Lock.

This allows you to draw a specific amount: say $50,000 for a kitchen remodel: and lock that specific balance into a fixed monthly payment.

This protects you from future interest rate hikes while keeping the rest of your unused line of credit available for emergencies.

Big banks rarely lead with this feature because they prefer the higher margins of variable-rate debt.

As a transparent Georgia HELOC lender, we believe you should have the choice to protect your budget from market volatility.

Strategies for Different Investor Profiles

The Landlord: Uses a HELOC to perform value-add renovations on existing units to increase monthly rent and property value.

The Fix-and-Flip Pro: Utilizes the line of credit as "gap funding" to cover renovation costs while a hard money loan covers the purchase price.

The BRRRR Investor: Draws from the HELOC to buy a distressed property in cash, renovates it, rents it out, and then refinances to pay the HELOC back.

The Airbnb Host: Leverages equity to furnish a new short-term rental property in a high-demand vacation market like Florida.

If you are looking for a Florida HELOC, you should know that the appraisal process is a critical hurdle.

Learn more about how property valuations impact your borrowing power at Appraisals.

The DTI Myth and Your HELOC Approval

DTI (Debt-to-Income Ratio): The percentage of your gross monthly income that goes toward paying your monthly debt obligations.

Practical application: Lenders use this to determine if you can afford the new HELOC payment along with your existing mortgage and lifestyle expenses.

Many homeowners believe they won't qualify for a HELOC because their income hasn't kept pace with their home's value.

However, some equity products are more flexible with DTI requirements than traditional mortgages.

For self-employed borrowers in Illinois or Michigan, Bank Statement Loans can sometimes be used in conjunction with equity strategies to prove cash flow.

Don't assume your "on-paper" income is a dealbreaker before speaking with a mortgage strategist.

You can check the Application Checklist to see what documents you really need.

Navigating the Costs: What to Watch Out For

While a HELOC is often cheaper than a refinance, it is not free.

Closing Costs: Fees associated with the processing and finalization of your loan, including appraisal and title fees.

Practical application: Always ask for a breakdown of these costs upfront so you aren't surprised at the signing table.

Compare these costs to other options on our Closing Costs page.

Some lenders offer "no-cost" HELOCs, but these usually come with a slightly higher interest rate.

Transparent lending means looking at the total cost over five or ten years, not just the fees due today.

We serve homeowners across Virginia, Kentucky, Indiana, and Illinois, providing clear guidance on which structure saves the most money long-term.

Why Location Influences Your HELOC Strategy

In Chicago, homeowners often use HELOCs to combat the rising costs of property taxes or to update older multi-unit buildings.

In California, the sheer volume of equity often makes a HELOC the primary tool for starting a business or buying a second home.

In Georgia and Florida, investors use HELOCs to move quickly on properties before the "big money" hedge funds can outbid them.

Having a "ready-to-go" line of credit makes you a cash buyer in the eyes of a seller.

This competitive edge is significant in tight markets where deals are won and lost in hours.

Your Equity is Your Engine

Stop viewing your home as just a place to live and start viewing it as a financial engine.

Whether you are in Alabama, Arkansas, or Missouri, the equity you have built is a tool that can generate more wealth.

The "secret" isn't that HELOCs are complicated; the secret is that they are often suppressed by big banks who want you to pay more in interest.

By keeping your first mortgage intact and using a smart second lien, you maintain control over your financial destiny.

Compare your options and see if you are ready to unlock the capital trapped in your walls.

Are You Ready to Unlock Your Potential?

The market is moving fast, and equity positions change with every economic shift.

Waiting too long could mean missing the window for the best LTV guidelines or the lowest margin rates.

If you have questions about how these strategies apply to your specific property in California, Florida, or Georgia, let’s talk.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664

What most homeowners don't realize is that once a HELOC is in place, it costs you nothing to keep it open if you aren't using it... but what happens when the bank decides to freeze those lines of credit during a market shift?

We'll dive into how to "recesssion-proof" your equity in our next update.