Wholesaling is often the entry point for many real estate investors. It is the practice of finding a distressed property, securing it under contract at a discount, and then passing that contract or the property itself to a cash buyer for a profit. While the concept sounds simple, the execution involves specific legal and financial logistics.

When you reach the point of closing a deal, you generally face two paths: an assignment of contract or a double closing. Each method has specific advantages depending on your profit margins, your need for privacy, and the specific regulations in states like California, Florida, and Georgia.

To navigate these waters successfully, you need to understand the mechanics of each strategy and how they impact your bottom line.

Understanding the Assignment of Contract

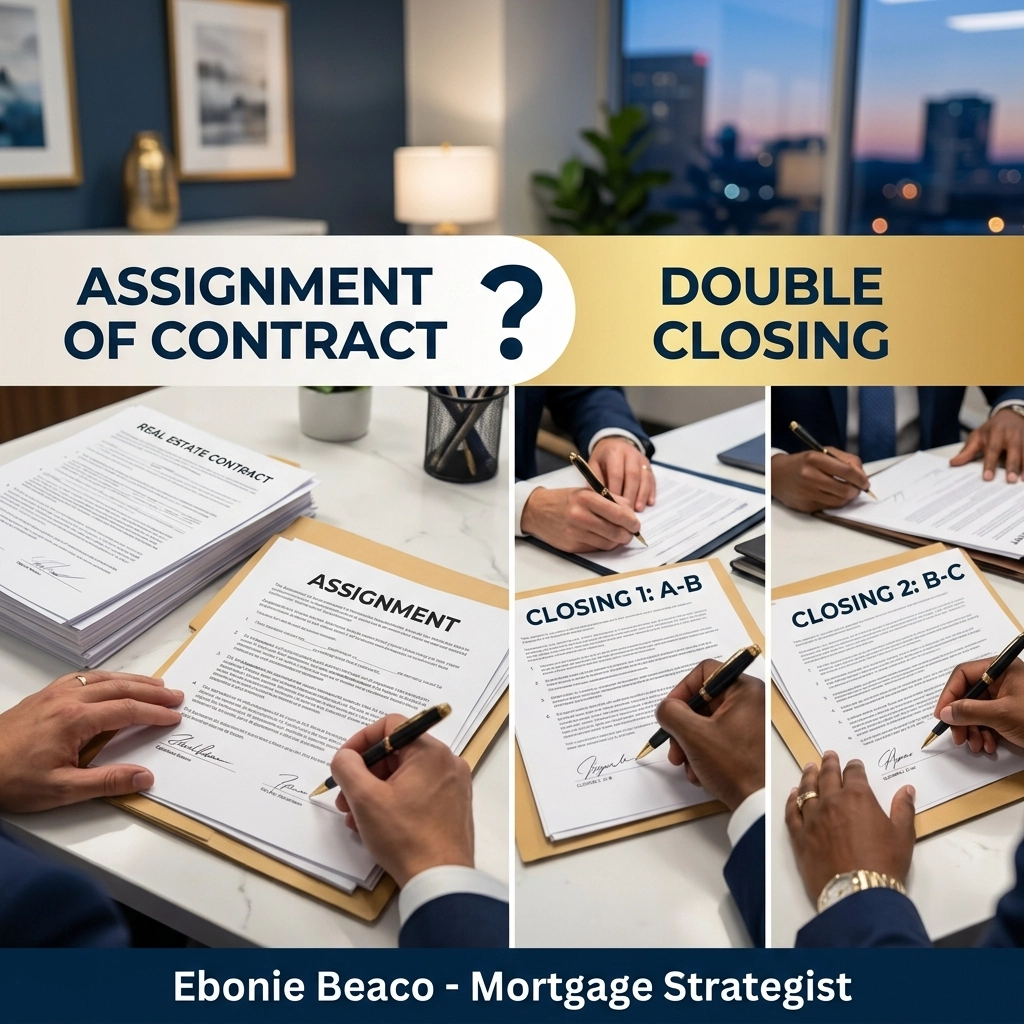

An assignment of contract is the process where the original buyer (the wholesaler) transfers their rights and obligations under a purchase agreement to a new buyer (the end investor).

In this scenario, you are not actually buying the house. You are selling the right to buy the house. You sign a contract with a seller, then you sign an Assignment of Real Estate Purchase and Sale Agreement with your end buyer.

How the Assignment Process Functions

Explore the steps of a typical assignment. First, you find a motivated seller and sign a purchase agreement that includes an "assignment clause." This clause is critical because it explicitly allows you to hand off the contract to someone else.

Once you find a cash buyer, you charge them an assignment fee. This fee represents your profit. The end buyer pays the purchase price to the seller and the assignment fee to you. Everything happens at a single closing conducted by a title company or an attorney.

Benefits of the Assignment Method

- Low Capital Requirement: You do not need to bring significant funds to the table because you aren't purchasing the property.

- Minimal Closing Costs: Since there is only one transaction between the seller and the end buyer, the wholesaler typically avoids paying traditional closing costs.

- Simplicity: It is a straightforward process involving less paperwork than a double closing.

Challenges to Consider

The primary drawback is transparency. The seller and the end buyer both see your assignment fee on the closing statement (the HUD-1 or ALTA settlement statement). If you are making a $5,000 fee, most people won't care. However, if your fee is $50,000 on a $200,000 house, the seller might feel they left too much money on the table, and the buyer might feel they are overpaying.

Navigating the Double Closing

A double closing, also known as a "back-to-back" closing, involves two distinct real estate transactions that occur almost simultaneously.

In this setup, there are two separate contracts:

- A-to-B Transaction: The seller (A) sells the property to the wholesaler (B).

- B-to-C Transaction: The wholesaler (B) sells the property to the end buyer (C).

Transactional Funding and Logistics

Because you are technically purchasing the property in the first transaction, you need the funds to close the A-to-B side. Most wholesalers use transactional funding.

Transactional Funding is a short-term loan (often 24 to 48 hours) specifically designed for wholesalers to facilitate double closings.

Jump in and look at the logistics: You use transactional funds to buy the property from the seller in the morning. In the afternoon, you sell the property to your cash buyer. You use the proceeds from the second sale to pay back the transactional lender (plus their fee) and keep the remaining profit.

Benefits of the Double Closing Method

- Privacy: This is the biggest selling point. The seller doesn't know how much you are selling the property for, and the buyer doesn't know how much you paid. Your profit stays confidential.

- No Assignment Clause Needed: If you are dealing with a property listed on the MLS or a bank-owned REO that prohibits assignments, a double closing allows you to bypass those restrictions.

- Professionalism: For large-scale commercial deals or high-end residential flips, a double closing can sometimes appear more professional to institutional sellers.

Challenges to Consider

- Higher Costs: You will pay two sets of closing costs: one for the purchase and one for the sale. You also have to pay the interest or fees associated with your transactional funding.

- Complexity: Coordinating two closings in one day requires an experienced title company or escrow officer who understands "wet" vs. "dry" funding.

Comparing the Two Strategies

Choosing between these two methods requires you to analyze your specific deal.

Compare the costs: If your expected profit is slim, the double sets of closing costs in a back-to-back transaction might eat up a significant portion of your gain. In that case, an assignment is usually the better route.

Access privacy needs: If you have negotiated an incredible deal where your spread is 20% or 30% of the property value, a double closing protects you from "deal fatigue" or "fee envy" from the other parties involved.

| Feature | Assignment of Contract | Double Closing |

|---|---|---|

| Capital Needed | None (only Earnest Money) | Transactional Funding or Cash |

| Closing Costs | Paid by End Buyer | Two sets of costs |

| Privacy | Low (Fee is disclosed) | High (Profit is hidden) |

| Complexity | Simple | Moderate to High |

| Speed | Very Fast | Fast |

Regional Nuances: California, Florida, and Atlanta

Real estate laws vary significantly by state, and wholesaling logistics are no exception.

Wholesaling in California

In California, disclosure is the name of the game. The California Association of Realtors (CAR) has specific language regarding assignments. Many wholesalers in cities like Los Angeles or San Diego prefer double closings for high-end deals because the profit margins are often large enough to absorb the extra closing costs, and the privacy helps keep the transaction smooth.

The Florida Market

Florida is a massive hub for wholesaling, particularly in Miami, Orlando, and Tampa. Florida title companies are very familiar with transactional funding. However, wholesalers must be careful not to engage in the "unlicensed practice of real estate." Focus on selling your equitable interest in the contract rather than the property itself if you are using the assignment method.

The Atlanta Landscape

Atlanta, Georgia is an attorney-closing state. This means a licensed attorney must oversee the closing. Many Atlanta attorneys are "investor-friendly" and specialize in assignment fees and back-to-back closings. When wholesaling in Georgia, ensure your attorney is comfortable with the "A-to-B / B-to-C" structure before you get too deep into the deal.

Financing the Exit Strategy

While the wholesaler might not need a traditional long-term mortgage, the end buyer (the "C" party) often does. If your end buyer is a "fix and flip" investor or a "buy and hold" landlord, they will need specialized financing to take the property off your hands.

This is where understanding various loan programs is useful for a wholesaler. If you can point your buyer toward reliable funding, you increase the chances of your deal closing successfully.

DSCR Investor Loans

A DSCR (Debt Service Coverage Ratio) Loan is a mortgage product for investment properties that qualifies the borrower based on the property’s rental income rather than their personal income. Practical application: Your end buyer can use a DSCR loan to purchase the property you assigned to them, ensuring they have the capital to close the deal even if they have reached their limit on conventional loans.

Explore more about DSCR investor loans to understand how your buyers qualify.

Hard Money and Bridge Loans

For investors in Chicago, Virginia, or California who are looking to renovate a property quickly, a Bridge Loan or a Fix and Flip Loan is common. These are short-term, asset-based loans that allow the investor to buy the property and fund the repairs.

If you are working with an end buyer who needs to move quickly, recommending a Fixed-Rate Mortgage isn't always the right move: they likely need an investor-specific product that prioritizes speed over long-term interest rates.

Key Technical Terms to Know

- Equitable Interest: The legal right to obtain full ownership of a property. When you sign a contract, you don't own the dirt yet, but you own the interest in the contract.

- Wholesale Assignment Fee: The compensation paid to the wholesaler for finding the deal and transferring the contract.

- Transactional Funding: Short-term financing used by wholesalers to buy and sell a property on the same day.

- Earnest Money Deposit (EMD): A sum of money put down by the buyer to demonstrate they are serious about the purchase. In an assignment, the end buyer usually replaces the wholesaler’s EMD.

Which Strategy Should You Use?

Deciding which path to take depends on your specific business model.

Choose Assignment of Contract when:

- You are working with a relatively small profit margin (under $10,000).

- The seller is a sophisticated investor who understands how wholesaling works.

- You want to avoid the fees associated with transactional funding.

- You are operating remotely in a state like Florida or Alabama and want the simplest paperwork possible.

Choose Double Closing when:

- Your profit margin is substantial ($15,000+).

- You are buying a property from the MLS, a bank, or a government entity (HUD).

- The original contract has a "No Assignment" clause.

- You want to maintain maximum privacy regarding your earnings.

Wholesaling is a powerful tool for building capital in real estate. Whether you choose to assign or double close, your success relies on your ability to find great deals and your network of reliable cash buyers.

Understanding how your buyers will finance these properties is equally important. If your buyer is looking to scale their portfolio using the BRRRR method or a Cash-Out Refinance, being able to speak their language will make you a much more valuable partner in the transaction.

If you have questions about how to structure your next deal or if you're an investor looking for the right financing to close on a wholesale contract, reach out for a strategy session.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664