It is Sunday evening. As you wind down for the week, you might be looking at your monthly bills and feeling a bit of weight on your shoulders. If you are a homeowner in Alabama, Missouri, or any of the vibrant markets from Virginia to California, you are sitting on a powerful financial tool that most people ignore until it is too late.

The current housing market has created a unique situation. Even with fluctuating interest rates, property values in states like Florida and Georgia have remained robust. This means you likely have a significant amount of equity locked away in your walls.

At Home Loans Network, we believe in transparency. We want to help you understand how to stop the cycle of high-interest debt and start using your home’s value to your advantage. Let’s explore the three common debt mistakes that might be holding you back and how a Home Equity Line of Credit (HELOC) can serve as your financial reset button.

Mistake 1: Falling into the Minimum Payment Trap

The most common mistake homeowners make is only paying the minimum balance on credit cards. It feels manageable in the short term, but it is a mathematical trap designed to keep you in debt for decades.

Minimum Payment: A small percentage of your total balance (usually 2-3%) that a lender requires you to pay each month to keep the account in good standing.

Practical Application: Making only minimum payments ensures that most of your money goes toward interest rather than reducing the actual debt you owe.

When you carry a balance on a card with a 24% APR, your "minimum payment" barely touches the principal. You are essentially renting your own money at an astronomical rate. If you are looking for a mortgage calculator to see how these numbers stack up against a home loan, you will quickly see the disparity.

Mistake 2: Using High-Interest Credit to Pay Other Debt

Many people try to "rob Peter to pay Paul" by opening new credit cards with 0% introductory rates to transfer balances. While this can work if you are disciplined, most people end up just adding more available credit and eventually more debt.

Using one high-interest vehicle to pay another is like treading water in a storm. Instead of seeking another revolving credit card, smart homeowners look toward their equity. Whether you are searching for an Alabama HELOC lender or looking at options in the Chicago suburbs, the goal is the same: lower the cost of your capital.

Mistake 3: Ignoring Your Home Equity Until There is a Crisis

The third mistake is treating your home equity like a "break glass in case of emergency" fund rather than a strategic financial asset. Many homeowners wait until their Debt-to-Income (DTI) ratio is too high to qualify for the best rates before they look into a HELOC.

DTI (Debt-to-Income Ratio): A personal finance measure that compares your monthly debt payments to your monthly gross income.

Practical Application: Lenders use this to determine your borrowing power; keeping this low by consolidating debt early helps you maintain a strong financial profile.

If you wait until you are struggling to make payments, your credit score might dip, making it harder to access the equity you’ve built. The best time to secure a reset is while your finances are stable.

How a HELOC Resets the Playing Field

A HELOC functions differently than a standard fixed-rate mortgage. It is a revolving line of credit, much like a credit card, but it is secured by your home. This security is why the interest rates are typically much lower than unsecured credit cards or personal loans.

HELOC (Home Equity Line of Credit): A revolving credit line secured by your home’s equity that allows you to borrow, repay, and borrow again during a set "draw period."

Practical Application: Use it to pay off $50,000 in credit card debt at a lower rate, then pay it back over time, saving thousands in interest.

Real-World Scenario: The $60,000 Debt Reset

Let’s look at a practical example of how a homeowner in Michigan or Virginia might use this strategy. Imagine you own a home valued at $500,000 and you owe $300,000 on your first mortgage. You also have $60,000 in combined credit card debt and a high-interest personal loan.

- Property Value: $500,000

- Current Mortgage: $300,000

- Max LTV (85%): $425,000

- Potential HELOC Limit: $125,000 ($425k minus $300k)

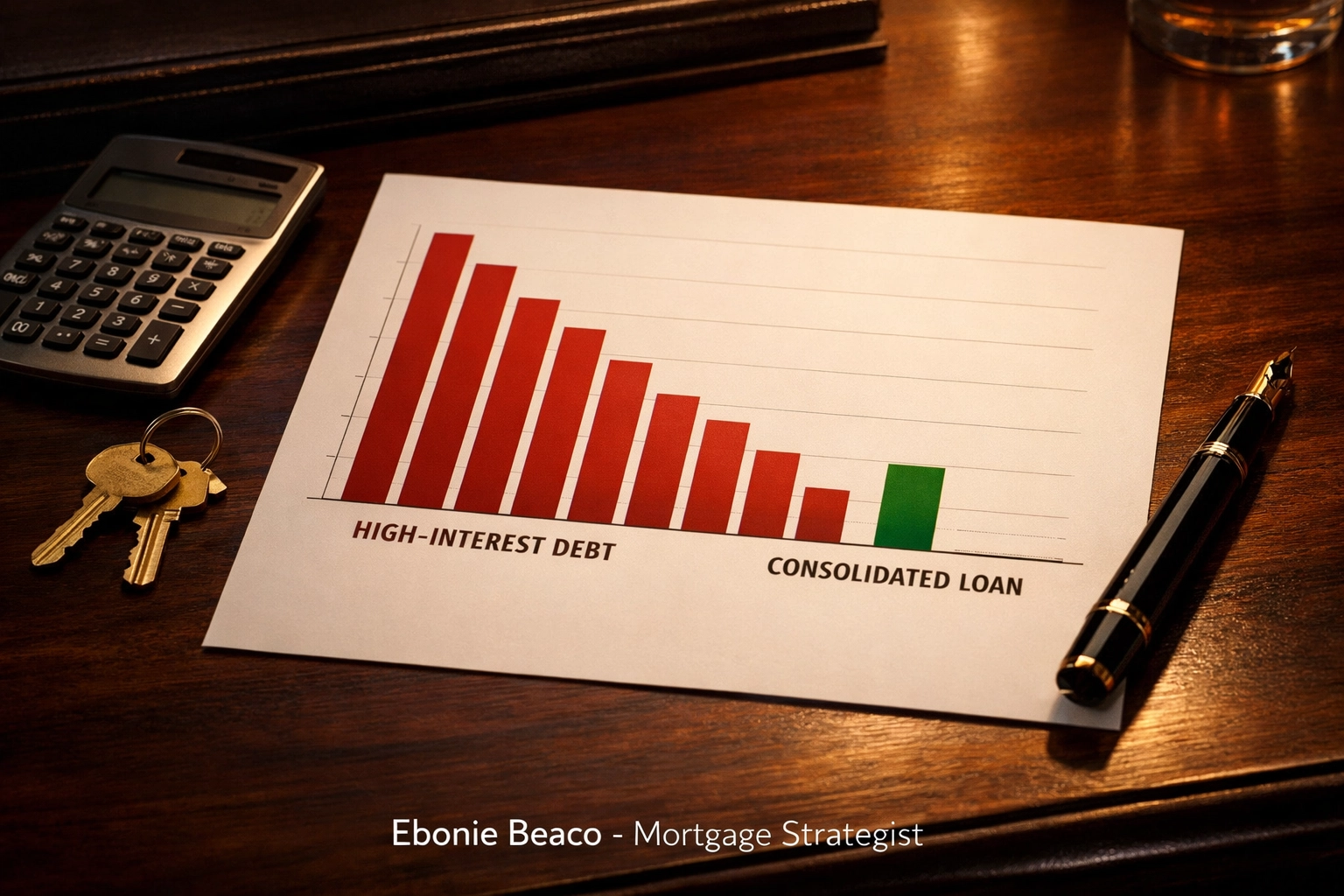

By taking out a HELOC for $60,000, you can pay off every single high-interest debt tonight. Instead of four different payments at 20%+ interest, you have one payment at a significantly lower rate.

LTV (Loan-to-Value): The ratio of your total loan amounts compared to the appraised value of your property.

Practical Application: This calculation determines exactly how much cash you can pull out or how large of a credit line you can establish.

Why Location Matters for Your HELOC

At Home Loans Network, we guide you through the specific nuances of your state’s lending laws. Whether you need a Missouri HELOC lender or you are looking for loan programs in California, the process varies slightly.

- Florida & Georgia: These markets have seen rapid appreciation, meaning your equity might be higher than you think.

- Illinois & Indiana: We see many investors using HELOCs on their primary residences to fund their next DSCR rental property.

- Arkansas & Kentucky: Homeowners here often use HELOCs for major renovations that further increase property value.

The Interest-Only Advantage

Many HELOC programs offer an "interest-only" payment option during the draw period (usually the first 10 years). This can drastically lower your monthly out-of-pocket costs compared to a traditional amortizing loan.

Interest-Only Period: A phase during the loan term where the borrower is only required to pay the interest on the principal balance.

Practical Application: This maximizes your monthly cash flow, allowing you to use that extra money to invest elsewhere or pay down the principal at your own pace.

Explore our interest-only mortgage resources to see if this flexibility fits your lifestyle.

Moving Forward with Confidence

Accessing your equity shouldn't feel like a gamble. It is a strategic move used by savvy investors and homeowners across the country. If you are tired of watching your hard-earned money disappear into interest payments, it is time to look at the numbers.

Jump in and compare your options. Whether you are considering a cash-out refinance or a HELOC, we are here to provide the transparency you need to make the right choice for your family.

Explore your equity potential and stop the debt cycle.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664

Disclaimer: All loan programs are subject to credit approval and property appraisal. Terms and conditions apply. Home Loans Network is an equal housing lender. For more information, visit our legal page and privacy policy.