High-interest debt often feels like a weight that grows heavier the more you try to move it.

Many homeowners across Alabama, Florida, and Missouri find themselves trapped in a cycle where monthly payments barely scratch the surface of the principal balance.

You might be working hard to stay afloat, but specific strategic errors could be keeping you anchored to high-interest rates.

Understanding how to leverage your home equity can change the trajectory of your financial future.

Explore the common pitfalls of debt management and learn how a Home Equity Line of Credit (HELOC) can serve as a powerful tool for consolidation and recovery.

1. Only Making the Minimum Payments

The most common mistake is sticking strictly to the minimum payment requested by your credit card issuer.

Minimum Payment: The lowest amount of money you are required to pay on a credit card or loan each month to keep the account in good standing.

Benefit: This prevents late fees but ensures the maximum amount of interest is charged over the life of the debt.

When you only pay the minimum, a significant portion of that money goes toward interest rather than the balance.

In many cases, it can take 20 to 30 years to pay off a $10,000 balance if you never pay more than the minimum.

This strategy keeps you in debt longer and costs you thousands in unnecessary interest charges.

Jump in and look at your most recent statement to see the "Minimum Payment Warning" to see exactly how long your current path will take.

2. Continuing to Spend While Paying Down Balances

Many people try to pay off their credit cards while simultaneously using them for daily purchases.

This creates a "one step forward, two steps back" scenario that prevents real progress.

You are essentially feeding the debt monster while trying to starve it.

It becomes impossible to track your progress when the balance fluctuates every week due to new charges.

Access a clear path to freedom by freezing your spending on high-interest accounts the moment you start a repayment plan.

3. Ignoring the Impact of High Utilization

Your credit score is heavily influenced by how much of your available credit you are using.

Credit Utilization Ratio: The percentage of your total available credit that you are currently using.

Benefit: Keeping this ratio below 30% typically helps maintain or improve your credit score.

When you carry balances close to your limits, your credit score drops, even if you make every payment on time.

A lower credit score means you will likely receive higher interest rates on future loans or refinances.

High utilization signals to lenders that you may be overextended, making it harder to qualify for better financial products.

Compare your current balances to your limits and notice how high utilization might be holding your score back.

4. Treating All Debt as Equal

Not all debt is created equal, and treating it that way can be a costly error.

Some homeowners in Virginia or Illinois might pay extra on a low-interest car loan while carrying a high-interest credit card balance.

Unsecured Debt: Debt that is not backed by collateral, such as credit cards or personal loans.

Benefit: While riskier for lenders, these loans usually carry much higher interest rates for the borrower.

Prioritizing a 5% interest loan over a 24% interest card is a mathematical mistake.

You should focus your aggressive payments on the debt with the highest interest rate first.

Explore the "Avalanche Method" to see how targeting high interest saves you the most money over time.

5. Missing the "Debt Avalanche" Opportunity

Many individuals lack a formal system for choosing which debts to pay first.

Debt Avalanche: A debt repayment strategy where you pay the minimum on all debts and put all remaining funds toward the debt with the highest interest rate.

Benefit: This method minimizes the total interest paid and shortens the overall repayment period.

Without this structure, you might feel like you are making progress, but you are likely losing money to compounding interest.

A structured plan provides a psychological boost because you can see a definitive end date for each account.

Accessing a debt calculator via https://www.homeloansnetwork.com/mortgage-calculators can help you visualize these payoff timelines.

6. Using Credit to Cover Monthly Shortfalls

Using high-interest credit cards to pay for basic living expenses like groceries or utilities is a sign of a structural budget issue.

This behavior turns temporary cash flow problems into long-term financial burdens.

The interest on those groceries will continue to compound long after the food is gone.

This cycle often leads to a "debt spiral" where you eventually run out of available credit and have no safety net.

Transparently evaluating your monthly budget is the first step toward stopping the cycle.

7. Paying High Interest When You Have Home Equity

The biggest mistake homeowners make is sitting on a mountain of equity while paying 20% or 30% interest on credit cards.

If you own a home in California, Georgia, or Michigan, your property value has likely increased significantly over the last few years.

Leaving that equity untouched while struggling with high-interest payments is like having a savings account you refuse to use while paying for a high-interest loan.

Home Equity: The difference between the current market value of your property and the outstanding balance of all liens on the property.

Benefit: This represents wealth you can leverage to secure lower-interest financing.

How a HELOC Fixes the Debt Cycle

A Home Equity Line of Credit (HELOC) is one of the most effective tools for debt consolidation.

HELOC (Home Equity Line of Credit): A revolving line of credit secured by your home that allows you to borrow against your equity as needed.

Benefit: It typically offers much lower interest rates than credit cards and provides flexible repayment options.

By using a HELOC to pay off high-interest credit cards, you immediately reduce the interest rate on that debt.

For example, you might move debt from a 25% APR credit card to a 9% or 10% HELOC.

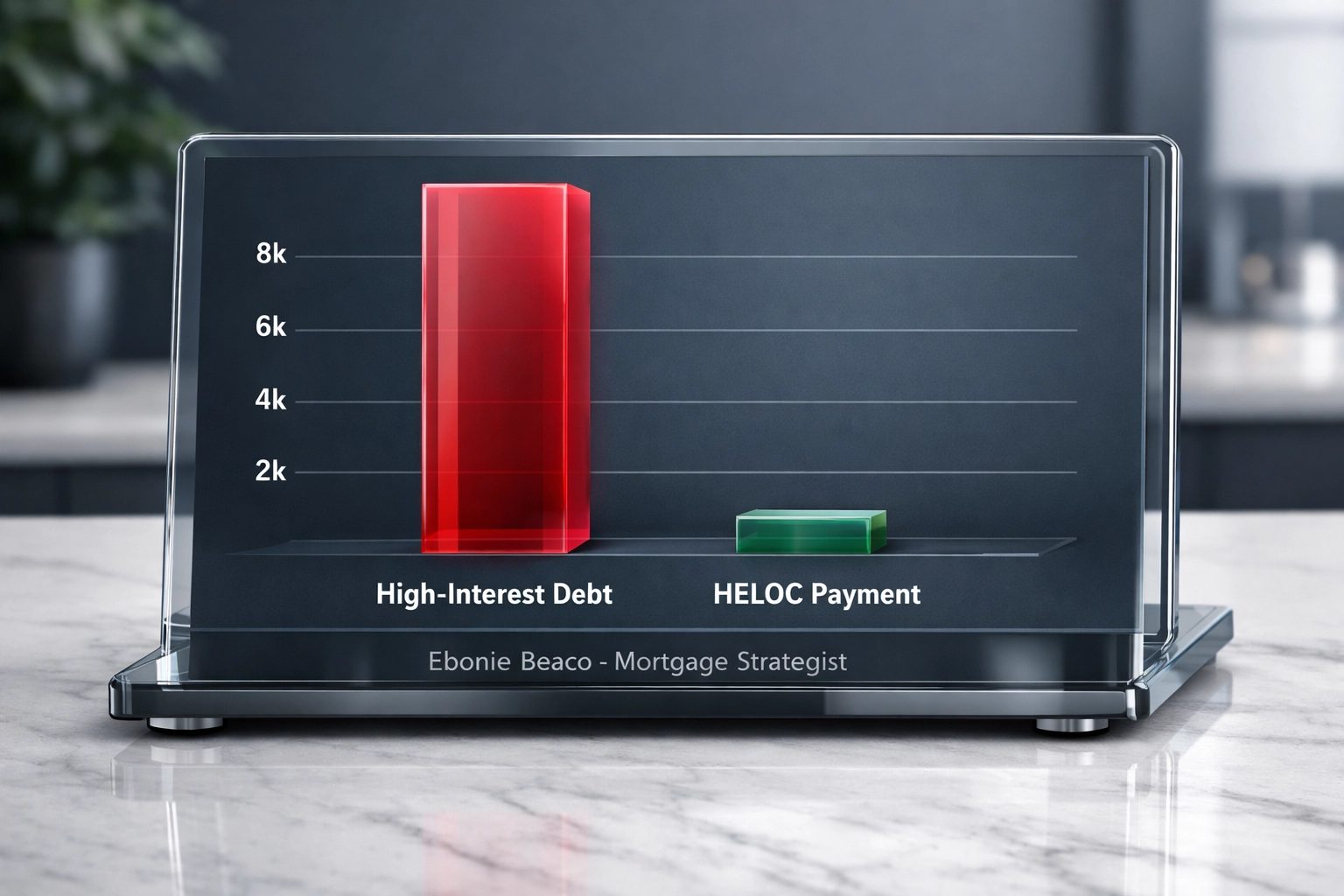

Real World Example: The Equity Rescue

Imagine a homeowner in St. Louis working with a Missouri HELOC lender.

They have $35,000 in credit card debt with an average interest rate of 24%.

Their monthly minimum payments total roughly $1,050, and most of that is just interest.

| Debt Type | Balance | Interest Rate | Monthly Payment |

|---|---|---|---|

| Credit Cards | $35,000 | 24% | $1,050 |

| New HELOC | $35,000 | 9.5% | $277 (Interest Only) |

By using the HELOC to wipe out the cards, the homeowner reduces their required monthly payment significantly.

Even if they continue to pay the original $1,050 toward the HELOC, the debt is paid off years earlier because more money goes toward the principal.

Explore your options at https://www.homeloansnetwork.com/loan-programs to see if a HELOC fits your profile.

Strategic Advantages of the HELOC

A HELOC offers flexibility that a standard home equity loan does not.

Draw Period: The initial phase of a HELOC (usually 10 years) during which you can borrow money and often make interest-only payments.

Benefit: This provides maximum cash flow flexibility during the years you are aggressively paying down debt.

You only pay interest on the amount you actually use.

If you have a $50,000 line of credit but only use $30,000 to pay off cards, you only owe interest on the $30,000.

This makes it an excellent tool for investors in Florida or Indiana who need to manage cash flow across multiple properties.

Whether you are a landlord managing rental properties or a homeowner looking to breathe easier, the math usually favors equity.

Why Your Location Matters

Interest rates and lending guidelines can vary based on your state.

If you are looking for an Alabama HELOC lender, you may find different loan-to-value (LTV) requirements than a borrower in Virginia.

LTV (Loan to Value): A ratio that compares the amount of your mortgage or loan to the appraised value of the property.

Benefit: Lenders use this to determine the risk level and the amount of equity you can access.

Home Loans Network works across various markets, including Kentucky, Arkansas, and the major metropolitan areas of Chicago and Northern Virginia.

Each of these markets has unique property value trends that impact how much equity you can access.

Jump in and check your local property values to see how much "hidden" cash you might have in your walls.

The Importance of Discipline

While a HELOC is a powerful fix, it requires a change in behavior.

A HELOC moves your debt from an unsecured card to a secured loan tied to your home.

Transparently speaking, you must commit to not running up the credit card balances again after you pay them off with the HELOC.

If you use the HELOC to pay the cards and then spend on the cards again, you have doubled your debt and put your home at risk.

Use the HELOC as a "reset button" to consolidate and then follow a strict budget.

Access our loan process guide to understand how we help you navigate this transition: https://www.homeloansnetwork.com/loan-process.

Is a HELOC Right for You?

If you have significant equity and high-interest debt, a HELOC is likely a smart move.

It is particularly useful for:

- Homeowners with credit card balances over $15,000.

- Real estate investors looking to consolidate renovation debt.

- Families in high-cost markets like California or Florida needing to lower monthly outflows.

- Individuals who want to improve their credit score by lowering their utilization ratio.

DTI (Debt to Income): A calculation used by lenders to determine if a borrower can manage monthly payments and repay debts.

Benefit: Lowering your monthly payments with a HELOC can improve your DTI for future investment property loans.

Lowering your monthly payments through consolidation makes you a stronger candidate for future financing, such as DSCR loans or traditional refinances.

Compare your options and see how your equity can start working for you instead of sitting idle.

Explore more about home equity strategies at https://www.homeloansnetwork.com/mortgage-basics.

Take Control of Your Equity

You don't have to be a victim of rising interest rates on consumer debt.

Your home is likely your largest asset; it should be helping you build wealth, not just serving as a place to live.

By avoiding these 7 common mistakes and utilizing a HELOC, you can save thousands of dollars and shave years off your debt-free timeline.

Whether you are in Missouri, Alabama, or anywhere in between, the strategy remains the same: use low-cost debt to eliminate high-cost debt.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664