Home equity functions as a powerful tool for wealth building, yet many homeowners across the Midwest and the South treat it like a bottomless ATM. Whether you are sitting on a property in the suburbs of Chicago or managing a rental portfolio in Birmingham, the way you access your equity dictates your long term financial health.

A Home Equity Line of Credit (HELOC) offers flexibility that a traditional fixed rate mortgage simply cannot match. However, that flexibility often leads to expensive oversights.

Explore the most common pitfalls currently affecting homeowners from Alabama to Illinois and identify the one mistake that could jeopardize your entire property portfolio.

The ATM Mentality: Using Equity as a Second Income

Definition: Equity Erosion

The reduction of home equity caused by continuous borrowing without a primary repayment strategy.

Practical Application: Maintaining a high equity position ensures you have a safety net for future real estate investments or market downturns.

The most dangerous habit homeowners develop is treating their HELOC like a standard checking account. When you use your home as a source of funds for daily expenses or vacations, you are essentially puting your roof at risk for items that lose value instantly.

In states like Michigan and Indiana, where property values have seen steady growth, it is tempting to spend that "new money" before it is truly yours. This mistake ranks as the most costly because it is habitual.

Over time, small draws for groceries or weekend trips accumulate into a massive balance. Unlike a credit card, this debt is secured by your primary residence or investment property.

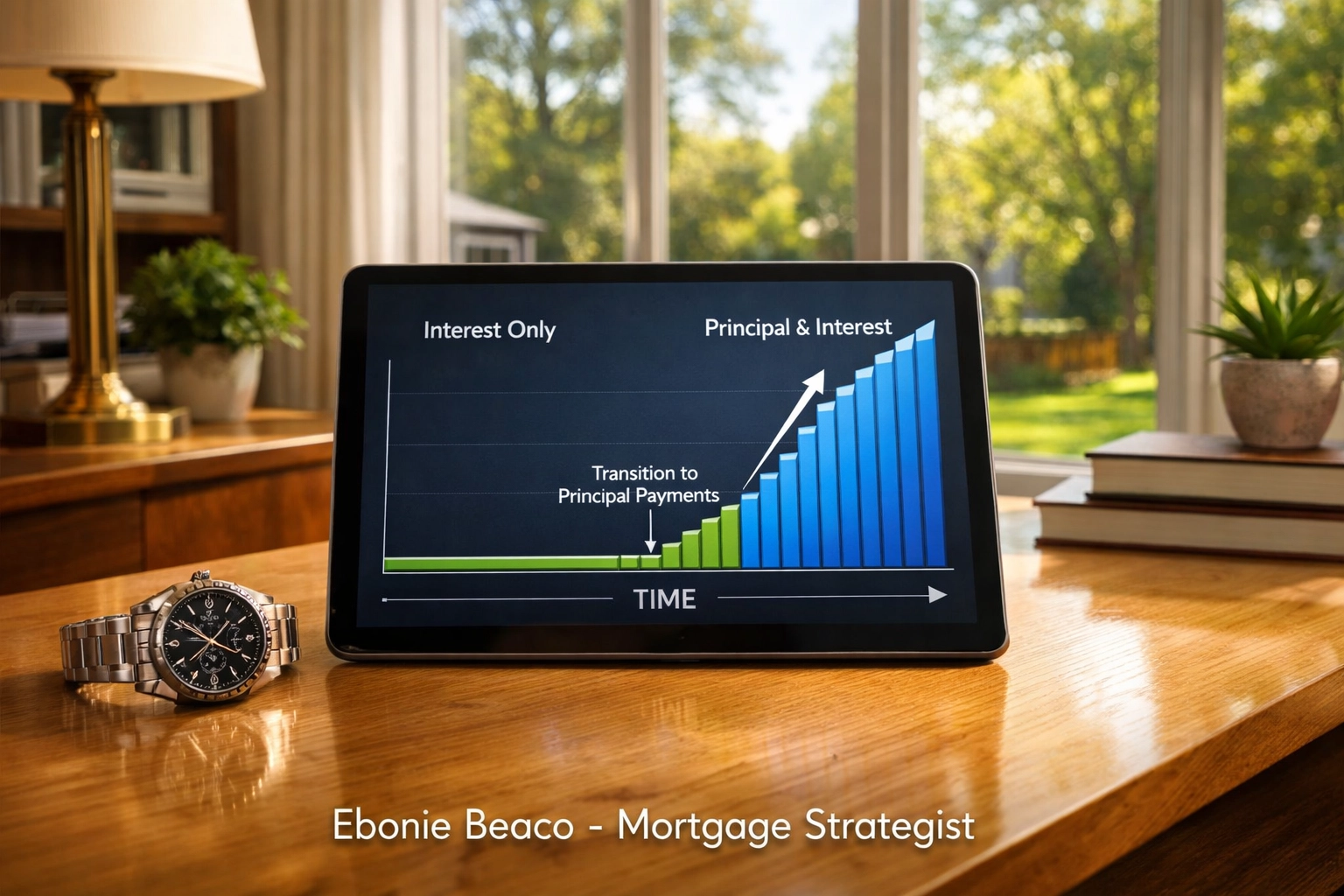

The Invisible Reset: When Interest Only Becomes Unmanageable

Definition: Draw Period

The initial phase of a HELOC, typically 10 years, where the borrower is often allowed to make interest only payments.

Practical Application: Understanding when this period ends allows you to prepare for a significant jump in monthly payment obligations.

Many homeowners in Virginia and Florida enjoy the low monthly costs during the draw period. They often forget that eventually, the loan enters the repayment phase.

Jump in and look at your loan documents today. If you are only paying interest, you are not reducing the principal balance. When the repayment period kicks in, your monthly payment could double or even triple as the principal is amortized over the remaining term.

The Variable Rate Gamble in an Unpredictable Market

Definition: Adjustable Rate

An interest rate that changes periodically based on an index, such as the U.S. Prime Rate.

Practical Application: Being aware of rate caps helps you calculate the maximum possible payment you might face in the future.

HELOCs typically feature variable rates. While this is great when rates are falling, it becomes a liability when they climb.

Homeowners from Missouri to Kentucky often overlook the fact that their monthly interest cost can change with very little notice. If you are operating on a tight budget, even a 1% or 2% increase in the Prime Rate can tighten your cash flow significantly.

Compare this to an adjustable rate mortgage which often has fixed periods. Most HELOCs adjust much more frequently.

The Debt Consolidation Trap That Doubles Your Debt

Definition: DTI (Debt-to-Income Ratio)

The percentage of your monthly gross income that goes toward paying debts.

Practical Application: Keeping this ratio low improves your ability to qualify for future financing, such as DSCR loans for rental properties.

Using a HELOC to pay off high interest credit cards is a popular strategy in Illinois and Georgia. It makes sense on paper because the HELOC rate is usually much lower than a credit card's 20% interest.

The mistake happens when the homeowner does not close the credit card accounts. Without a change in spending habits, they run the credit cards back up to their limits.

Now, instead of just having credit card debt, you have the original debt balance on your HELOC plus the new credit card balances. This trap often leads to a cycle of debt that is difficult to escape without a cash out refinance.

Ignoring the Fine Print of Total Borrowing Costs

When looking for a Michigan HELOC lender or a Virginia HELOC lender, many homeowners focus solely on the starting interest rate. They forget to account for the secondary costs associated with opening and maintaining the line.

Access the full picture by looking at:

- Annual maintenance fees.

- Inactivity fees if you don't use the line.

- Early closure penalties (often if you close the line within the first 3 years).

- Appraisal fees and closing costs.

These fees can eat into the benefits of the lower interest rate, especially if you only plan to borrow a small amount.

Over-Leveraging in a Correcting Market

Definition: LTV (Loan-to-Value)

A ratio that compares the amount of your mortgage or loan to the appraised value of the property.

Practical Application: Maintaining an LTV below 80% protects you from becoming "underwater" if property values decrease.

In areas like California or parts of Florida where the market can be volatile, over-leveraging is a significant risk. If you draw your HELOC to the maximum limit and property values dip, you could owe more than the home is worth.

This prevents you from selling the home or refinancing into a fixed rate mortgage without bringing cash to the closing table. Always leave a cushion of equity for market fluctuations.

Funding Speculative Investments Without a Safety Net

Real estate investors in Alabama and Arkansas often use HELOCs to fund the down payment on a new rental or a fix and flip project. While this is a common strategy, using a HELOC for speculative investments: like high risk stocks or crypto: is a recipe for disaster.

If the investment fails, you still owe the money to the bank, and your home is the collateral. Professional investors typically use home equity for assets that produce income, such as DSCR rental properties, which help cover the HELOC payment.

A Practical Look: How Much Can You Actually Borrow?

Understanding the math behind a HELOC is essential for any homeowner or investor. Let's look at a scenario for a homeowner in Chicago with a primary residence.

The Financial Calculation:

- Current Home Value: $500,000

- Existing First Mortgage Balance: $300,000

- Maximum LTV Allowed by Lender: 85%

- Total Allowable Debt ($500,000 x 0.85): $425,000

- Available HELOC Limit ($425,000 - $300,000): $125,000

In this example, the homeowner has $125,000 available to use. However, just because you can borrow $125,000 does not mean you should. A smart mortgage strategist would suggest only drawing what is necessary for improvements that increase the home's value or for high yield investment opportunities.

Which Mistake Will Cost You the Most?

While all these errors are expensive, treating home equity like personal income is the most devastating. It creates a structural deficit in your personal finances that is hard to fix.

When you spend your equity on lifestyle rather than assets, you are consuming your future wealth. For many in the Home Loans Network states, the home is the largest asset they own. Protecting that equity is the key to long term stability.

Navigating the HELOC Landscape Clearly and Confidently

If you are considering a HELOC in Alabama, Illinois, or anywhere in between, transparency is your best friend. Don't be swayed by "teaser rates" that jump after six months. Instead, focus on how the line of credit fits into your total financial plan.

Whether you are a landlord looking to expand your portfolio or a homeowner planning a renovation, understanding these pitfalls helps you avoid the common traps that catch others off guard.

Explore your options with a focus on long term goals. Use our mortgage calculators to see how different scenarios impact your monthly cash flow and total interest paid over time.

Resolve your uncertainty about home equity strategies today.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664