Credit card companies love it when you carry a balance.

They thrive on those 22%, 25%, and even 29% interest rates that keep you locked into a cycle of monthly payments that barely touch the principal.

If you own a home in Alabama, Missouri, or any of the states we serve, you have a secret weapon that big banks rarely advertise as a debt relief tool.

High-interest debt is often a choice, not a permanent condition.

By leveraging a Home Equity Line of Credit (HELOC), you can effectively "fire" your high-interest creditors and replace them with a significantly lower-cost option.

This isn't just about moving numbers around; it is about changing the trajectory of your personal wealth.

The HELOC Defined: Your Personal Credit Reservoir

HELOC (Home Equity Line of Credit): A revolving credit line secured by the equity in your primary residence or investment property.

Think of a HELOC as a credit card that uses your house as collateral.

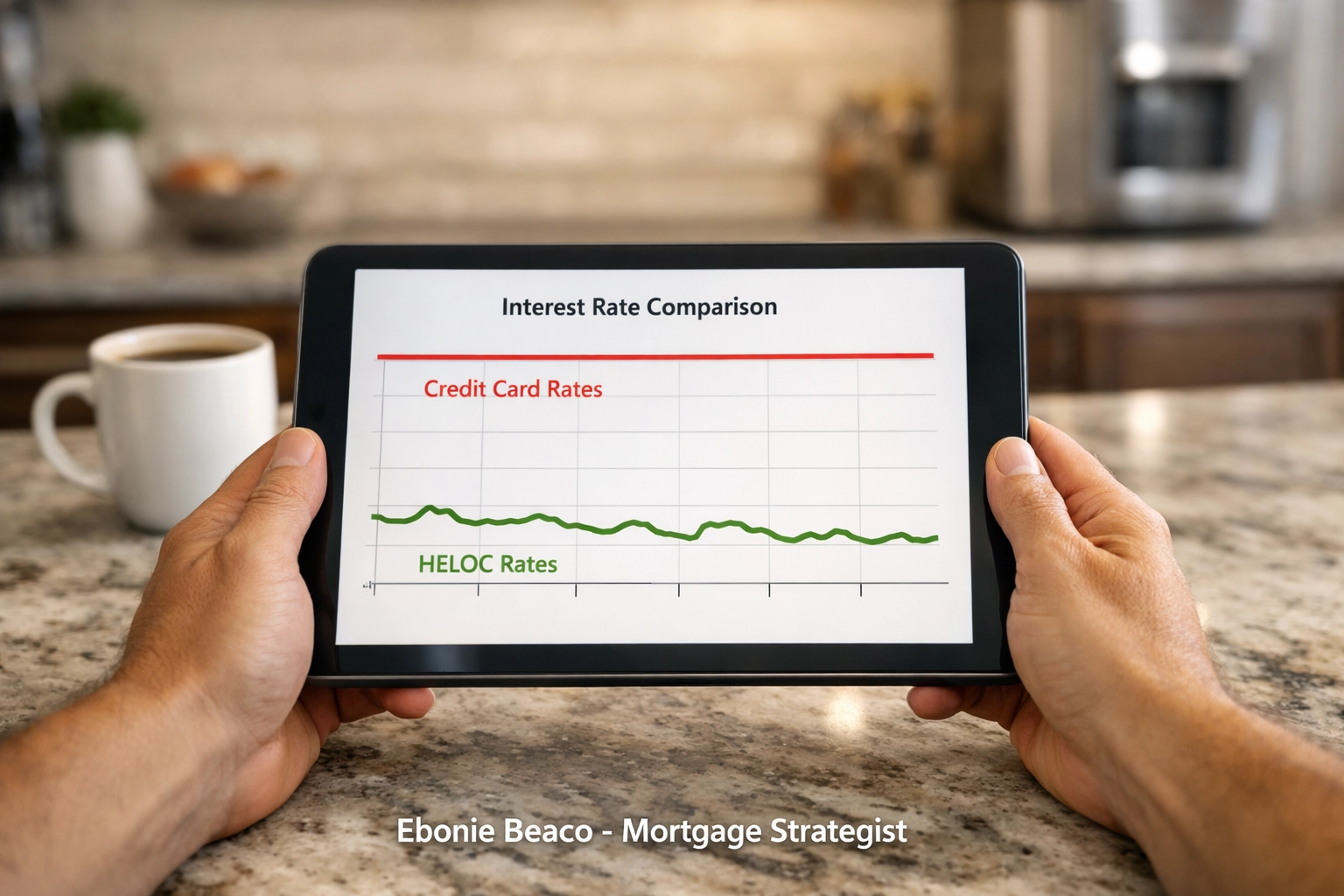

Because the loan is secured by real estate, the interest rates are typically a fraction of what you would pay for unsecured personal loans or credit cards.

As an Alabama HELOC lender and Missouri HELOC lender, we see homeowners use these lines to regain control of their cash flow every single day.

Why Banks Want You to Keep Your Credit Cards

Banks make billions from "unsecured" debt.

When you have a credit card balance, the bank has nothing to seize if you stop paying.

To compensate for that risk, they charge you astronomical interest rates.

When you switch to a HELOC, you are moving that debt into a "secured" category.

Because your home backs the loan, the risk to the lender decreases, and your interest rate drops accordingly.

The "truth" is that banks would much rather you pay 24% on a credit card than 8% or 9% on a HELOC.

One keeps you in debt for decades; the other provides a clear path to becoming debt-free.

Strategic Debt Consolidation in Action

Explore how this works in a real-world scenario.

Imagine a homeowner in Florida or Illinois with the following debt profile:

- Credit Card A: $15,000 at 26% APR ($325/mo interest)

- Credit Card B: $10,000 at 22% APR ($183/mo interest)

- Personal Loan: $15,000 at 15% APR ($187/mo interest)

Total Debt: $40,000

Total Monthly Interest Cost: $695

Now, look at the HELOC alternative.

If this homeowner accesses a HELOC at a 9% interest rate to pay off those balances:

- HELOC Balance: $40,000 at 9% APR

- Total Monthly Interest Cost: $300

By simply shifting the debt, this homeowner saves $395 every single month.

That is nearly $4,800 a year that stays in your pocket instead of going to a credit card company.

Understanding the LTV Equation

LTV (Loan-to-Value): The ratio of all loans on a property compared to the current appraised value of that property.

To access a HELOC, lenders typically look at your Combined Loan-to-Value (CLTV).

Most programs allow you to borrow up to 80% or 85% of your home's value, minus your existing mortgage balance.

Example Calculation: The Michigan Homeowner

Let’s say you own a home in Michigan valued at $450,000.

Your current mortgage balance is $280,000.

If a lender allows an 85% CLTV, the math looks like this:

- $450,000 (Value) x 0.85 = $382,500 (Max Total Debt Allowed)

- $382,500 - $280,000 (Current Mortgage) = $102,500 (Available HELOC)

In this scenario, you could access over $100,000 to consolidate debt, handle home renovations, or invest in further real estate.

The Draw Period vs. The Repayment Period

One of the most powerful features of a HELOC is the flexibility in how you pay it back.

Draw Period: The initial timeframe (usually 10 years) during which you can borrow money and often make interest-only payments.

Repayment Period: The subsequent timeframe (usually 15 to 20 years) where the line is closed to new draws and you must pay back both principal and interest.

Jump in during the draw period to maximize your monthly cash flow.

By making interest-only payments on your consolidated debt, you free up the maximum amount of "found money" to either save, invest, or aggressively pay down the principal on your own terms.

Geographic Advantages: From California to Virginia

Real estate markets vary, but the power of equity is universal.

In high-appreciation states like California or Virginia, homeowners often find they have much more equity than they realized.

A simple appraisal might reveal that your home value has climbed significantly over the last few years.

This "hidden wealth" is exactly what you use to fuel a HELOC.

Even in markets with more steady growth, like Kentucky or Arkansas, the gap between your mortgage and your home's value is a resource that often sits idle.

Using that equity to kill high-interest debt is one of the smartest moves a homeowner can make.

Is a HELOC Right for You?

Compare your current financial situation against these criteria:

- High Credit Card Balances: If you are paying more than 15% interest on any significant amount of debt.

- Sufficient Equity: You owe significantly less than what your home is worth.

- Disciplined Spending: You have the discipline to not run the credit card balances back up once they are paid off.

- Stable Income: You can comfortably manage the variable interest rate associated with most HELOCs.

Accessing your equity requires a clear strategy.

You should always review the application checklist to ensure your credit and documentation are in order.

The "Variable Rate" Reality

Transparency is vital in mortgage lending.

Unlike a standard refinance where you might lock in a fixed rate, most HELOCs feature variable interest rates.

These rates are often tied to the Prime Rate.

If the Federal Reserve raises rates, your HELOC payment will likely go up.

However, even with rate hikes, HELOC rates historically stay much lower than the "fixed" high rates found on credit cards.

You are trading a very high fixed rate (credit cards) for a much lower variable rate (HELOC).

For most homeowners, the savings are still substantial even if rates fluctuate.

Real Estate Investors and the HELOC

If you are a landlord or real estate investor in Georgia or Indiana, a HELOC on your primary residence can serve as a "down payment fund."

Many investors use a HELOC to acquire a new rental property, then use a DSCR loan to finance the asset based on its rental income.

This strategy allows you to scale your portfolio without draining your liquid cash reserves.

It is a common tactic among professionals to keep their capital moving and working.

Final Thoughts on Home Equity

Your home is likely your largest asset.

Leaving all that equity "trapped" in the walls while you pay 20% interest to a bank is a missed opportunity.

Whether you are in the heart of Chicago or a quiet suburb in Florida, the math remains the same.

Lowering your interest expense is the fastest way to increase your net worth.

Resolve your uncertainty by exploring what your equity can do for your monthly budget.

Taking the Next Step

Stop letting high-interest debt dictate your financial future.

The path to financial clarity starts with understanding your options.

Whether you need a Missouri HELOC lender to help you consolidate debt or an Alabama HELOC lender to fund your next investment, we are here to guide you clearly and confidently.

Use our mortgage calculators to see how much you could potentially save by switching to a home equity solution.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664