HELOC Secrets Revealed: How Kentucky Homeowners Are Getting New Kitchens Without the Wait

Walking into a kitchen with chipped laminate countertops and 1990s oak cabinets can feel like stepping back in time.

Many homeowners in Kentucky and Indiana sit at their kitchen tables every morning, dreaming of white quartz and open shelving, but the price tag usually keeps those dreams parked in the driveway.

The "wait" is usually the hardest part: waiting to save up $40,000 in cash or waiting for interest rates on personal loans to drop.

However, savvy homeowners are skipping the line and getting those renovations started today by using a strategy that high net worth investors have used for decades.

They are tapping into the hidden wealth sitting right inside their walls.

The Hidden Vault in Your Home

You likely have a significant amount of money sitting in your home that you cannot see.

As property values have climbed across Kentucky and Indiana over the last few years, the gap between what you owe and what your home is worth has widened.

This gap is known as equity.

Equity: The market value of a homeowner's unencumbered interest in their real property. Practical Application: If your home is worth $450,000 and you owe $250,000, you have $200,000 in equity that can be used as collateral for a loan.

Instead of a traditional loan where you get a lump sum and start paying interest on the whole amount immediately, Kentucky homeowners are opting for a HELOC.

What is a HELOC?

Explore the concept of a "house credit card."

HELOC (Home Equity Line of Credit): A revolving line of credit secured by the equity in your home, allowing you to borrow, repay, and borrow again. Practical Application: You use the line of credit to pay your contractor for the new cabinets this month, and then draw more next month for the appliances.

This flexibility is exactly why it is the preferred tool for renovations.

Why Kentucky Homeowners Are Choosing HELOCs Over Other Loans

When you decide to fix up a home in Louisville, Lexington, or even across the river in Indianapolis, you have options.

You could use a credit card, but the interest rates are often north of 20%.

You could take out a personal loan, but those typically have shorter repayment terms and higher monthly costs.

A Kentucky HELOC lender can offer rates that are significantly lower because the loan is secured by the home itself.

This security reduces the risk for the lender, and those savings are passed on to you.

How the HELOC Draw Period Accelerates Your Kitchen Remodel

One of the biggest "secrets" to getting a kitchen done without the wait is the draw period.

Draw Period: A set timeframe, typically 10 years, during which a borrower can withdraw funds from their HELOC. Practical Application: During this phase, most HELOCs allow for interest-only payments on the amount you have actually spent.

Imagine your kitchen remodel costs $50,000 in total.

If you took out a traditional loan for $50,000, you would start paying interest on the full $50,000 on day one.

With a HELOC, if you only spend $5,000 on the initial demolition and flooring, you only pay interest on that $5,000.

This keeps your monthly costs low while the construction is actually happening.

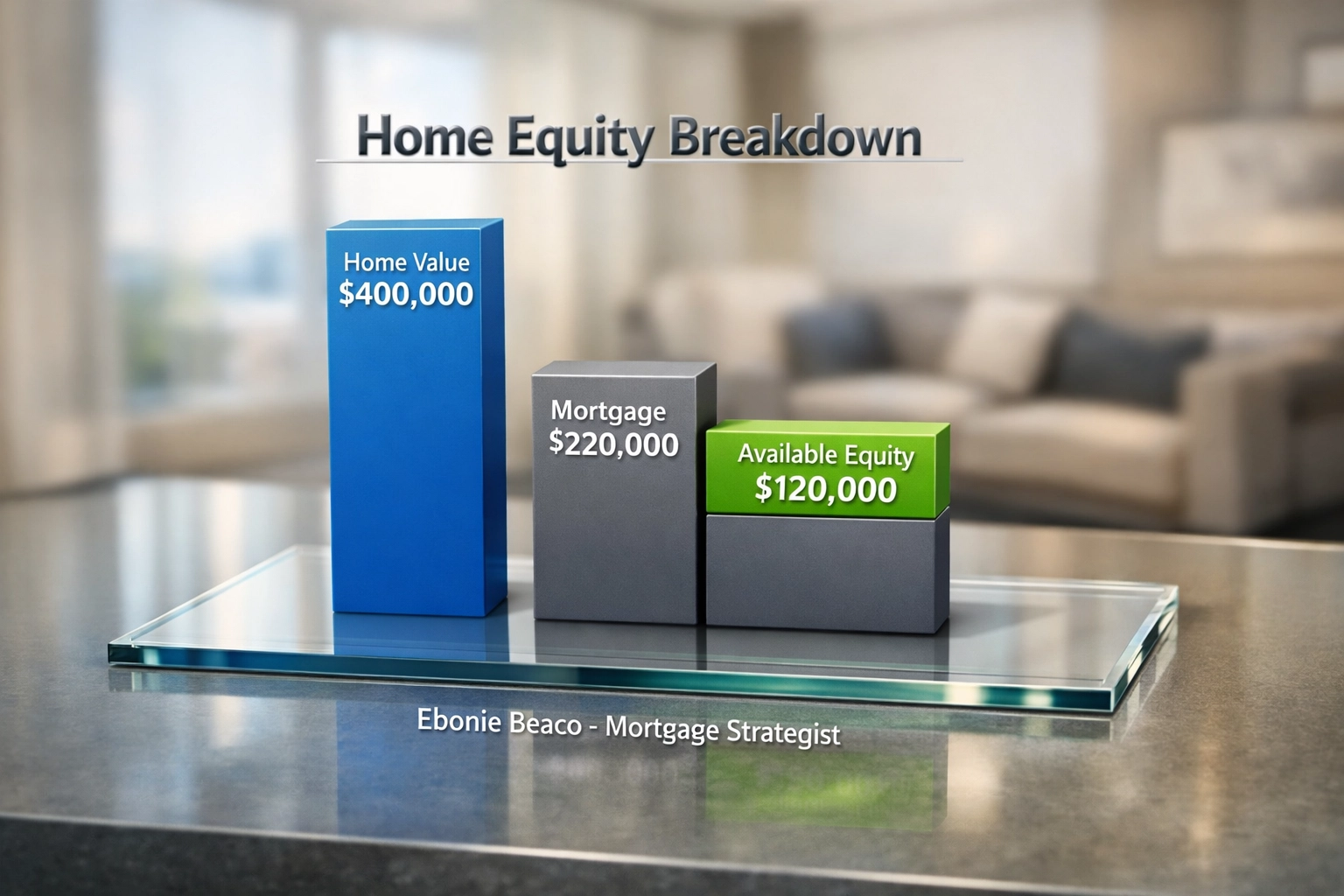

A Real World Kentucky Equity Example

Let's look at how the math works for a typical homeowner working with an Indiana HELOC lender or a Kentucky strategist.

Imagine you own a home in a growing neighborhood.

- Current Home Value: $400,000

- Current Mortgage Balance: $220,000

- Max Loan-to-Value (LTV): 85%

LTV (Loan-to-Value): A ratio used by lenders to express the amount of a first mortgage as a percentage of the total appraised value of real property. Practical Application: Lenders use this to determine how much equity you can actually touch.

To find your available credit, the calculation looks like this:

- Multiply the home value by the LTV limit ($400,000 x 0.85 = $340,000).

- Subtract your current mortgage balance ($340,000 - $220,000 = $120,000).

In this scenario, you have access to a $120,000 line of credit.

That is more than enough to handle a high-end kitchen remodel, a new deck, and perhaps some landscaping to go with it.

The ROI Secret: Why Kitchens Win

Real estate investors and homeowners alike focus on kitchens because they offer one of the highest returns on investment (ROI).

In the current market, a well-executed kitchen remodel can return between 60% and 80% of its cost in added home value.

If you are planning to sell your home in the future, the HELOC isn't just a way to get a pretty kitchen; it is a way to increase your net worth.

Access our mortgage calculators to see how your home value impacts your borrowing power.

Transparency in Lending: The Variable Rate Factor

At Home Loans Network, we believe in being transparent about how these programs work.

Most HELOCs come with variable interest rates.

This means your rate can fluctuate based on market conditions.

Variable Interest Rate: An interest rate on a loan or security that fluctuates over time because it is based on an underlying benchmark interest rate. Practical Application: If the Federal Reserve raises or lowers rates, your HELOC payment will likely adjust accordingly.

While this can be a benefit when rates are falling, it is something to plan for if rates rise.

If you prefer stability, you might also compare this with a fixed-rate mortgage cash-out refinance.

Tax Benefits You Shouldn't Ignore

Another reason Kentucky homeowners are jumping into HELOCs is the potential for tax deductibility.

Under current tax laws, interest paid on home equity debt is often deductible if the funds are used to "buy, build, or substantially improve" the home that secures the loan.

This effectively makes your renovation even more affordable.

Always consult with a tax professional to see how this applies to your specific situation, as every financial profile is unique.

Expanding Beyond Kentucky: Regional Equity Growth

While we are focusing on Kentucky and Indiana, the strategy is identical for our clients in Alabama, Arkansas, California, Florida, Georgia, Illinois, Michigan, Missouri, Virginia, and specifically the Chicago area.

Equity growth has been a nationwide trend.

Homeowners in Florida and California are using HELOCs to fund ADUs (Accessory Dwelling Units) to generate rental income.

Investors in Michigan and Virginia are using the loan process to bridge the gap between purchasing a property and completing the "flip."

How to Access Your Equity Today

Getting started is faster than most people realize.

You do not need to wait for a traditional 30-day closing in many cases.

- Check Your Equity: Use a tool or talk to a strategist to estimate your current LTV.

- Get a Quote: Compare the limits and rates offered by a specialized Kentucky HELOC lender.

- Define Your Scope: Have a clear idea of what your kitchen renovation will cost so you don't over-borrow.

- Open Your Line: Once approved, you can access the funds via a checkbook or a debit card linked to the account.

Explore our loan programs to see which equity tool fits your project best.

The Strategy for Real Estate Investors

If you are an investor using the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) method, a HELOC on your primary residence can be the perfect "seed money."

You can use the equity in your home to fund the down payment on a DSCR rental property loan.

DSCR (Debt Service Coverage Ratio): A measurement of a property's available cash flow to pay current debt obligations. Practical Application: Investors use this to qualify for loans based on the rental income of the property rather than their personal income.

This allows you to grow a portfolio without draining your personal savings account.

Is the Wait Finally Over?

The "secret" isn't magic; it is just using the tools available to you as a homeowner.

You have already done the hard work of paying your mortgage and maintaining your home.

Now, it is time for your home to work for you.

Jump in and see what your equity could do for your living space and your long-term financial health.

Whether you are looking for an Indiana HELOC lender or you are a homeowner in Virginia ready for a change, the path to a new kitchen is likely shorter than you think.

Stop waiting for the "perfect time" and start building the home you want to live in today.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664