What Is the Best Way to Fund My First Real Estate Investment?

Entering the real estate market in Mobile, Alabama, is more than just a financial move; it is a strategic step toward long-term wealth building. Whether you are eyeing a historic cottage in Midtown or a beachside rental near Dauphin Island, the most critical hurdle is always the same: How do you fund the deal?

For many aspiring investors, especially those entering their "legacy" years, the answer isn't always a traditional bank loan. In fact, relying solely on rigid bank terms can often stall your progress before you even close. As a mentor-advisor in this space, I see too many investors overlook the most powerful asset they already own: their home equity.

In this guide, we will break down the most effective ways to fund your first investment in the Port City, focusing on strategies that maximize cash flow and minimize out-of-pocket stress.

The Strategic Shift: Traditional Debt vs. Equity Optimization

Most new investors think funding starts with a 20% down payment from a savings account. While that works, it is often the least efficient way to scale. In Mobile’s competitive market, being "cash-heavy" in your personal accounts doesn't always translate to the best return on investment (ROI).

Instead, we look at Equity Optimization. If you are a homeowner aged 62 or older, you have a strategic advantage that younger investors lack: the ability to leverage a Reverse Mortgage (HECM) to fund your portfolio.

1. Leveraging a Reverse Mortgage for Investment Capital

A common "timing problem" for seniors is having high net worth tied up in their primary residence but limited liquid cash for a new down payment. By utilizing a Cash-Out Reverse Mortgage on your current Mobile home, you can access tax-free proceeds without adding a monthly mortgage payment to your primary residence.

The Logic: If you take $150,000 in equity via a reverse mortgage to buy a rental property in Spring Hill, you aren't just "spending" that money. You are moving it from a non-performing asset (your home’s equity) into a cash-flowing asset (a rental property). Because the reverse mortgage requires no monthly principal and interest payments on your primary home, your total monthly expenses remain low, allowing the rental income from the new property to be pure profit.

2. DSCR Loans: The "No-Income" Investor Weapon

If you aren't looking to tap into your primary home's equity, the next best tool for a first-time investor is the DSCR (Debt Service Coverage Ratio) Loan. This is a favorite for realtors and investors in Alabama because it doesn't look at your personal tax returns or W-2 income.

- Rigid Bank Terms: Require years of tax returns and deep DTI (Debt-to-Income) checks.

- Flexible Funding (DSCR): Qualifies the loan based entirely on the rental income of the property you are buying.

If the rental property in Downtown Mobile generates $2,000 a month and the mortgage/taxes/insurance cost $1,600, the DSCR is 1.25. As long as the property "covers" its own debt, the loan is typically approved. This is perfect for those who are self-employed or have complex tax write-offs that make traditional qualifying difficult.

3. Bank Statement Loans for the Mobile Entrepreneur

Mobile is a hub for logistics, maritime, and small business owners. If your tax returns don't reflect your true earnings due to legitimate business write-offs, Bank Statement Loans are your path forward. Instead of looking at your "bottom line" on a 1040, we look at 12–24 months of deposits into your business or personal accounts. This provides a pragmatic view of your ability to fund a rental property without the red tape of traditional underwriting.

Case Study: The Mobile "Equity Flip"

Let's look at a real-world scenario. Meet "Sarah," a 65-year-old homeowner in the West Mobile area. Her home is worth $450,000, and she owes nothing on it. She wants to buy her first rental property: a $200,000 condo: but doesn't want to drain her $250,000 retirement account.

The Strategy:

- Step 1: Sarah takes a Reverse Mortgage on her primary home, securing $150,000 in cash.

- Step 2: She uses that $150,000 as a 75% down payment on a $200,000 rental property.

- Step 3: She finances the remaining $50,000 with a traditional or DSCR loan.

The Result:

- Primary Home: No monthly mortgage payment (Sarah only pays taxes and insurance).

- Rental Property: $1,800/month rent.

- New Mortgage Payment: Approx. $400/month.

- Net Cash Flow: $1,400/month (before maintenance).

Sarah effectively created $16,800 in annual income without ever writing a check from her personal savings. That is thinking like an owner, not a borrower.

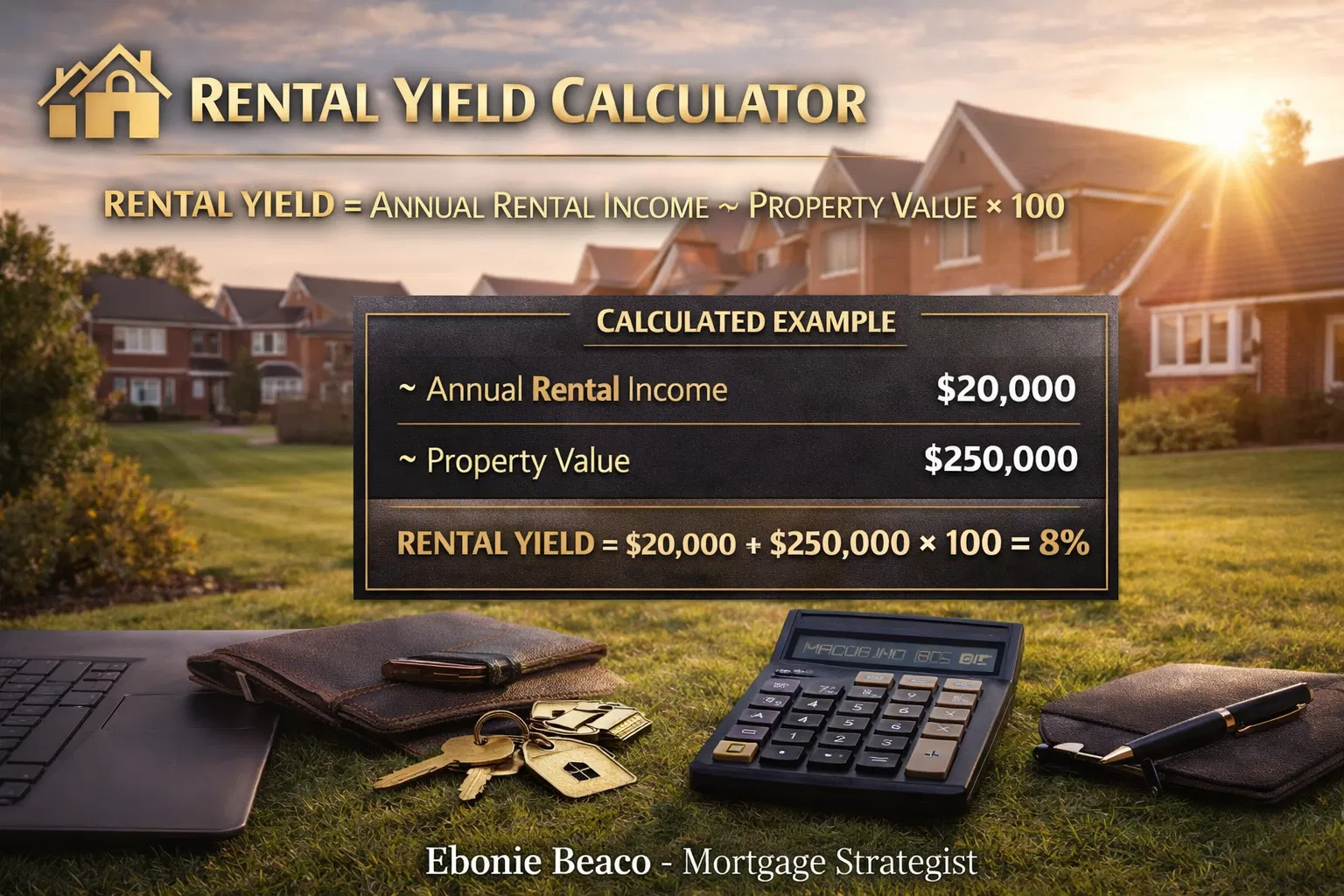

Understanding the Math: Mobile, AL Investment Calculation

When funding your first deal, you must run the numbers with a cold, calculated eye. Here is a simple breakdown for a typical Mobile residential investment:

| Category | Calculation | Result |

|---|---|---|

| Purchase Price | Target Property (e.g., Midtown) | $175,000 |

| Funding Source | 20% Down Payment (via Equity Access) | $35,000 |

| Monthly Rent | Local Market Average | $1,650 |

| PITI Payment | (Principal, Interest, Taxes, Insurance) | $1,200 |

| Net Cash Flow | Monthly Income - Expenses | $450/month |

| Cash-on-Cash Return | ($5,400 Annual Profit / $35,000 Invested) | 15.4% |

Note: In Alabama, property taxes are relatively low compared to the national average, which significantly boosts your "Residual Reality" and monthly cash flow.

Common Roadblocks and How to Pivot

New investors often face the "Analysis Paralysis" of high interest rates or market fluctuations. However, real estate is about time in the market, not timing the market.

- Objection: "Interest rates are too high for a first rental."

- Reality: Rates are temporary; the equity growth in Mobile’s port-driven economy is long-term. If the numbers cash-flow today, you can refinance when the cycle shifts.

- Objection: "I don't have the 20% down."

- Reality: This is where we use Seller Credits or Lender Credits. In some scenarios, we can structure the deal so the seller pays for your closing costs, keeping more cash in your pocket for repairs and reserves.

Frequently Asked Questions (FAQ)

Can I use a Reverse Mortgage to buy the investment property directly?

A standard HECM (Home Equity Conversion Mortgage) must be used for your primary residence. However, you can use the proceeds from a reverse mortgage on your primary home to purchase an investment property in full or as a down payment.

What is the minimum credit score for a DSCR loan in Alabama?

Typically, we look for a 620+ score, but the "strength of the deal" (the property's income) is more important than your personal credit history.

Is Mobile, AL a good market for first-time investors?

Absolutely. With the expansion of the Port of Mobile and the aerospace sector, rental demand remains high. Neighborhoods like Saraland and Tillman’s Corner are particularly strong for residential stability.

Do I need to be a W-2 employee to get funding?

No. Through our Non-QM programs, including 1099 and Bank Statement loans, we specialize in getting deals approved that traditional banks decline.

The Bottom Line: Start with Strategy

The best way to fund your first real estate investment in Mobile is the way that protects your liquidity and maximizes your long-term stability. Whether it is leveraging the equity in your current home through a reverse mortgage or utilizing a DSCR loan to focus on the property's potential, the goal is "deferred gratification" and compounding wealth.

Don't let rigid bank terms stop your progress. Thinking like an owner means looking at the whole board.

Ready to see how much equity you can unlock for your first deal? Let's build your Mobile portfolio today.

Contact:

Ebonie Beaco, Loan Officer (NMLS #2389954)

Phone: 312-392-0664

Website: www.HomeLoansNetwork.com

Powered by Loan Factory, Inc. (NMLS #320841)

Disclaimer: This content is for educational purposes only and does not constitute a loan approval or commitment. Loan programs, terms, and eligibility requirements are subject to change and vary by borrower and property.