What is a DSCR Loan and How Does It Work for Florida Vacation Rentals?

For many experienced homeowners and seniors looking to diversify their portfolios, the Florida vacation rental market represents more than just a sunshine-filled getaway, it represents a high-yield asset class. However, the traditional path of using personal income to qualify for a secondary property often hits a wall. This is where the Debt Service Coverage Ratio (DSCR) loan enters the conversation.

While many of our clients are familiar with tapping into their primary residence equity through a Reverse Mortgage to secure their retirement, the next logical step is often: How do I put that trapped equity to work?

In this guide, we will break down the mechanics of DSCR loans and, more importantly, how you can strategically use a reverse mortgage on your primary home to "seed" a lucrative Florida rental business without the burden of monthly personal mortgage payments.

Understanding the DSCR Loan: The Investor's Weapon

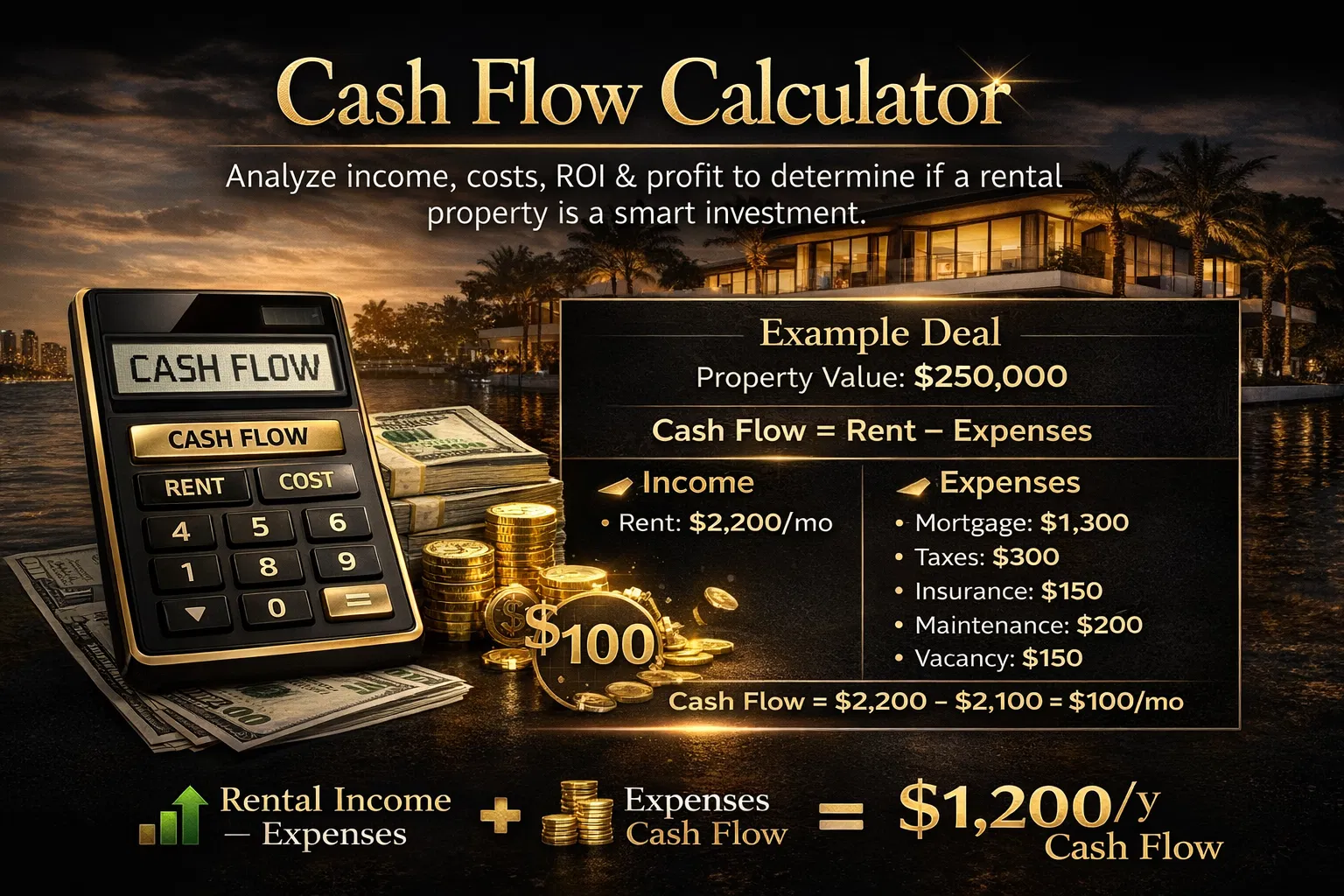

A DSCR loan is a type of "Non-QM" (Non-Qualified Mortgage) loan that focuses on the property’s ability to pay for itself. Unlike a conventional loan that scrutinizes your W-2s, tax returns, and personal debt-to-income (DTI) ratio, a DSCR loan only cares about one thing: Cash Flow.

The formula is straightforward:

DSCR = Monthly Gross Rental Income / Monthly Debt Service (PITIA)

- Principal

- Interest

- Taxes

- Insurance

- Association Dues (HOA)

If the property generates $3,000 in rent and the total mortgage payment is $2,400, your ratio is 1.25. Generally, a ratio of 1.0 or higher is the "sweet spot" for approval. Moreover, in the high-demand Florida market, from the STR (Short-Term Rental) hubs of Orlando to the luxury shores of Miami, projected Airbnb income can often be used to qualify, even if the property hasn't been rented yet.

The Strategy: Reverse Mortgage vs. Traditional Funding

For homeowners over the age of 62, the traditional route of taking out a new mortgage to buy an investment property can be restrictive. Traditional lenders look for high active income. If you are semi-retired or living on a fixed income, your "on-paper" earnings might not reflect your actual net worth.

This is where the "Reverse to Rental" strategy shines.

By utilizing a Reverse Mortgage on your primary residence, you can unlock a lump sum or a line of credit without a monthly mortgage payment requirement. As a result, you have the liquidity needed for a down payment on a Florida vacation rental. You then use a DSCR loan for the rental itself.

Thus, you protect your personal cash flow while building a new revenue stream in Florida's vacation market.

Why Florida? A Hyper-Local Breakdown

Florida remains a powerhouse for real estate investors because of its year-round tourism and tax-friendly environment. However, "Florida" isn't one single market. Your strategy must be localized.

- Orlando (The STR Capital): Properties near Disney and Universal offer massive DSCR potential due to high occupancy rates.

- Miami & Fort Lauderdale: High barrier to entry but incredible appreciation and premium nightly rates for luxury rentals.

- Tampa & Clearwater: A blend of steady long-term growth and seasonal vacation demand.

- Destin & Panama City Beach: High seasonal peaks that can cover an entire year’s debt service in just six months.

When you use a DSCR loan in these areas, you aren't tied down by the standard 10-property limit found in conventional financing. Therefore, you can scale as fast as your cash flow allows.

Case Study: The Florida "Sun & Sea" Strategy

Let’s look at a pragmatic example of how a senior homeowner in Jacksonville or Naples might execute this.

The Scenario:

- Primary Residence Value: $800,000 (Owned outright or low balance).

- Strategy: Secure a Reverse Mortgage (HECM) to pull $250,000 in tax-free proceeds.

- Investment Goal: Purchase a $600,000 vacation rental in Kissimmee (Orlando area).

The Calculations:

- Down Payment (25%): $150,000

- Closing Costs & Furnishings: $50,000

- Total Initial Investment: $200,000 (Funded by the Reverse Mortgage).

- DSCR Loan Amount: $450,000

- Estimated PITIA (at 7.5%): $3,650

- Projected STR Income (Avg. Monthly): $5,500

- DSCR Ratio: 1.50 ($5,500 / $3,650)

In this case, the investor has successfully acquired a $600,000 asset without using a dime of their monthly retirement income. The vacation rental pays for itself, and the primary home remains their own with no monthly mortgage bill.

Technical Deep Dive: Qualifications and Terms

When you approach us at REI Invest Capital for a DSCR loan, we cut through the red tape. Here is what you need to know:

- Credit Scores: We typically look for a 620 minimum, but higher scores unlock better rates.

- No Income Verification: We do not ask for your tax returns. We look at the appraisal’s 1007 or 1025 rent schedule or third-party STR data (like AirDNA).

- Prepayment Penalties: Most DSCR loans have a 1-5 year prepayment penalty. We can often buy this down or structure it to fit your exit strategy if you plan to sell or refi in a few years.

- Ownership: You can close in your personal name or a business entity (LLC), which is highly recommended for vacation rentals to protect your other assets.

The Mentor-Advisor Perspective: Stability over Hype

At REI Invest Capital, we don't believe in "get rich quick" schemes. We believe in portfolio health. While the DSCR loan is a powerful lever, it must be used with a "thinking like an owner" mindset.

You must account for the "deferred gratification" of real estate. Florida is prone to insurance fluctuations and seasonal dips. Therefore, we always advise our clients to keep a robust reserve fund. By using a Reverse Mortgage on your primary home to fund the acquisition, you aren't stressing your personal bank account when the "off-season" hits.

Frequently Asked Questions (FAQ)

1. Can I use a DSCR loan for a property I plan to live in?

No. DSCR loans are strictly for investment properties. If you are looking for a primary residence solution, a Conventional or FHA loan is the better path.

2. Is a Reverse Mortgage the same as a HELOC?

Not quite. A HELOC requires monthly payments (usually interest-only at first). A Reverse Mortgage (HECM) does not require monthly mortgage payments as long as you live in the home, pay your taxes, and maintain the property. This makes it a far more stable source of investment capital for seniors.

3. What if my vacation rental is empty for a month?

This is why the DSCR ratio is calculated on an annual basis. Lenders look for a property that, on average, covers the debt. We also recommend having 3-6 months of reserves to handle vacancies.

4. Can I get a DSCR loan in Florida if I live in Illinois or Michigan?

Absolutely. We specialize in out-of-state investors. Florida is one of our most active markets for investors from across the country.

Conclusion: Strategic Growth for the Long Term

The combination of a Reverse Mortgage for liquidity and a DSCR loan for acquisition is a sophisticated strategy that balances risk and reward. It allows you to leverage your greatest asset: your home: to build a legacy in the world’s most famous vacation destination.

If you are ready to stop letting your equity sit idle and start building a Florida rental portfolio that pays for itself, it’s time to talk strategy.

Contact:

Ebonie Beaco, Loan Officer (NMLS #2389954)

Phone: 312-392-0664

Website: www.HomeLoansNetwork.com

Powered by Loan Factory, Inc. (NMLS #320841)

Disclaimer: This content is for educational purposes only and does not constitute a loan approval or commitment. Loan programs, terms, and eligibility requirements are subject to change and vary by borrower and property.