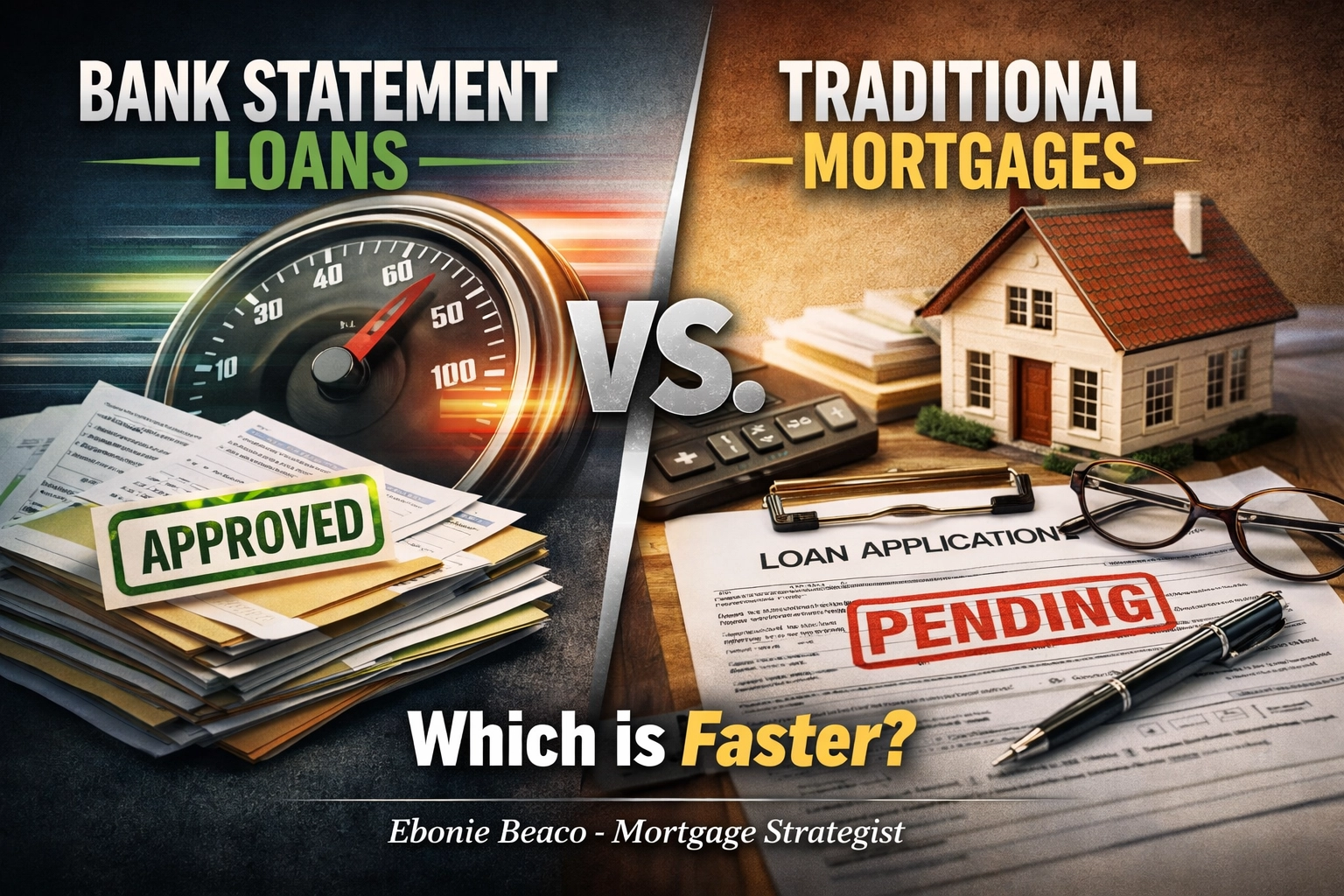

Bank Statement Loans vs. Traditional Mortgages: Which is Faster?

When you are ready to purchase a home or an investment property, the clock starts ticking the moment your offer is accepted. For many self-employed professionals, freelancers, and small business owners in states like Florida, California, or Illinois, the primary hurdle isn't the credit score or the down payment: it is the speed of the income verification process.

The debate between Bank Statement Loans and Traditional Mortgages often centers on interest rates, but for those in fast-moving markets like Chicago or Atlanta, the real question is: Which one gets you to the closing table faster?

While traditional financing is the standard for W-2 employees, it often creates significant bottlenecks for those with complex income streams. Explore the nuances of these two paths to determine which strategy aligns with your timeline and financial profile.

Defining the Financing Paths

To compare speed, we must first define the mechanisms of each loan type.

Traditional Mortgage: A conventional or government-backed loan that requires standard income documentation, such as W-2s, pay stubs, and federal tax returns.

- Practical Benefit: Offers the lowest available interest rates for borrowers who can easily prove a stable, predictable income through standard tax forms.

Bank Statement Loan: A Non-QM (Non-Qualified Mortgage) program that allows borrowers to prove their ability to repay using 12 to 24 months of personal or business bank statements instead of tax returns.

- Practical Benefit: Enables self-employed individuals to use their actual cash flow and gross deposits as qualifying income, bypassing the "paper losses" often found on tax write-offs.

The Documentation Bottleneck

The primary reason a mortgage process slows down is the "back-and-forth" between the underwriter and the borrower.

In a Traditional Mortgage, the underwriter must verify your income against what you reported to the IRS. For a self-employed borrower, this means analyzing Schedule C, K-1s, and corporate tax returns. If there are discrepancies or if you haven't filed your most recent returns, the process can grind to a halt. You can learn more about these requirements on our Mortgage Basics page.

Bank Statement Loans bypass this entirely. Because these loans do not require tax returns, there is no need to wait for IRS transcripts or explanations for complex business deductions. You simply provide your statements, and the lender calculates your qualifying income based on average monthly deposits.

Document Checklist Comparison

Traditional Loan Requirements:

- Two years of federal tax returns.

- Two years of W-2s or 1099s.

- Recent pay stubs (30 days).

- Signed 4506-C form (allowing the lender to pull IRS transcripts).

- Profit and Loss (P&L) statements for self-employed borrowers.

Bank Statement Loan Requirements:

- 12 or 24 months of consecutive bank statements.

- A valid business license or a letter from a CPA.

- A brief summary of business expenses.

- Credit report and asset verification.

Visual: A side-by-side comparison chart titled 'Bank Statement vs. Traditional Loans' showing the reduced document count for Bank Statement options. Ebonie Beaco - Mortgage Loan Officer at the bottom.

Visual: A side-by-side comparison chart titled 'Bank Statement vs. Traditional Loans' showing the reduced document count for Bank Statement options. Ebonie Beaco - Mortgage Loan Officer at the bottom.

The Underwriting Timeline

You might assume that "manual underwriting" for bank statement loans takes longer, but the opposite is often true in real-world scenarios.

A traditional loan usually targets a 30-day closing. However, for a business owner in Michigan or Virginia with multiple entities, the verification of employment and income can extend that to 45 or 60 days. The lender must ensure the business is stable and that the income is likely to continue, often requiring third-party verification that can be slow to respond.

A Bank Statement Loan typically closes within a 21 to 35-day window. While the underwriter must manually add up every deposit and subtract an expense factor, this is a linear process controlled entirely by the lender. There is no waiting on the IRS. This predictability is vital when you are competing for a property in a high-demand area like Miami or Los Angeles.

Access our Loan Process guide to see how we streamline these steps.

Real-World Scenario: The Chicago Entrepreneur

Consider a self-employed graphic designer in Chicago looking to buy a $500,000 condo.

The Traditional Path: The designer’s gross income is $150,000, but after smart business deductions, their taxable income on their tax returns is only $45,000. Under traditional Debt-to-Income (DTI) rules, they cannot qualify for a $400,000 loan. They must spend weeks working with a CPA to find alternative documentation or wait a year to file taxes differently.

The Bank Statement Path: The designer provides 12 months of business bank statements showing consistent deposits averaging $12,500 per month. The lender applies a 50% expense factor, resulting in a qualifying monthly income of $6,250 ($75,000 annually).

The Calculation:

- Property Value: $500,000

- Down Payment (20%): $100,000

- Loan Amount: $400,000

- Avg Monthly Deposits: $12,500

- Qualifying Income (50% Expense Ratio): $6,250

- Estimated Monthly Payment (PITI): $3,100

- Resulting DTI: 49.6% (Within Non-QM limits)

Because the documentation was straightforward, the file moved from submission to "Clear to Close" in 24 days.

Visual: A financial deal breakdown titled 'Bank Statement vs. Traditional Loans' showing the Chicago Entrepreneur scenario: $500k Purchase, $100k Down, $12,500 Monthly Deposits, $6,250 Qualifying Income. Ebonie Beaco - Mortgage Loan Officer at the bottom.

Visual: A financial deal breakdown titled 'Bank Statement vs. Traditional Loans' showing the Chicago Entrepreneur scenario: $500k Purchase, $100k Down, $12,500 Monthly Deposits, $6,250 Qualifying Income. Ebonie Beaco - Mortgage Loan Officer at the bottom.

Interest Rates vs. Opportunity Costs

It is transparent to note that Bank Statement Loans usually carry a higher interest rate than traditional conventional loans: often by 1% to 2.5%.

However, you must evaluate the opportunity cost. If a traditional loan takes 60 days and you lose the house to a cash buyer, or if you simply cannot qualify because of your tax write-offs, the "lower rate" is irrelevant.

Investors in Arkansas, Kentucky, and Georgia often use bank statement loans to secure properties quickly, then look into a Home Refinance later once their tax documentation is structured differently. The speed of the initial acquisition is the priority.

Why Speed is a Strategy

In the world of real estate investing: whether you are looking at DSCR Investor Loans or Fix and Flip Financing: speed is a form of currency.

When you can tell a seller in Missouri or Alabama that you are using a Non-QM lender that doesn't need to wait on IRS transcripts, your offer becomes much more attractive. It signals that you have a clear path to funding without the typical bureaucratic hurdles of big-box retail banks.

Jump in and explore our FAQ to see how these programs differ in various market conditions.

Key Considerations for Borrowers

Before choosing a path, review these three factors:

- Consistency of Deposits: Bank statement lenders look for stability. Large, unexplained "one-time" deposits may be backed out of the average.

- Expense Ratios: Lenders typically assume your business has costs. If you are a service-based consultant with low overhead, we can often use a lower expense factor with a letter from your CPA, increasing your qualifying income.

- Credit Profile: While bank statement loans are flexible on income, they still value a solid credit history. You can check your potential scenarios using our Mortgage Calculators.

Making the Decision

If you have a clean W-2 and your tax returns show high net income, a traditional mortgage is likely your fastest and most cost-effective route.

However, if you are self-employed and your tax returns do not reflect your true buying power, the Bank Statement Loan is the clear winner for speed and accessibility. It eliminates the friction of traditional underwriting and allows your actual cash flow to do the talking.

Compare your options carefully and consider the impact of closing dates on your overall investment strategy. If you need clarity on which program fits your specific business structure in California, Virginia, or beyond, seeking expert guidance is the next logical step.

Reach out to Ebonie Beaco for bank statement loan options or mentoring at www.homeloansnetwork.com.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664