Unlocking Home Equity: The Complete Guide to Reverse Mortgages for Alabama Investors

For many Alabama homeowners over the age of 62, the family home is more than just a place of memories: it is a significant, yet illiquid, financial asset. In the current real estate market, where property values in Birmingham, Huntsville, and Mobile have seen substantial appreciation, many residents find themselves "house rich and cash poor." A reverse mortgage, specifically the Home Equity Conversion Mortgage (HECM), offers a strategic pathway to unlock that equity without the burden of monthly mortgage payments.

While traditionally viewed as a tool for retirement stability, savvy real estate investors are increasingly utilizing the reverse mortgage as a sophisticated leverage tool. By shifting from a "debt-paydown" mindset to an "equity-utilization" strategy, homeowners can transform stagnant brick-and-mortar into a liquid engine for portfolio growth.

Understanding the Reverse Mortgage: The Alabama Context

A reverse mortgage is a unique financial product that allows homeowners to convert a portion of their home equity into cash. Unlike a traditional forward mortgage, where you make monthly payments to a lender to build equity, a reverse mortgage pays you. The loan is typically repaid when the last surviving borrower sells the home, moves out permanently, or passes away.

In Alabama, the HECM remains the most popular option because it is federally insured by the FHA. As of 2026, the FHA has increased the maximum claim amount to $1,249,125. This limit is crucial for residents in higher-end markets like Mountain Brook or the coastal properties in Baldwin County, as it determines the maximum value of equity the FHA will consider when calculating your available funds.

The Residency Requirement

It is imperative to understand that a HECM must be placed on your primary residence. Therefore, you cannot take out a reverse mortgage on a rental property in Montgomery while living in Hoover. However, the strategic "investor move" involves extracting equity from your primary Alabama residence to fund the down payments or outright purchases of secondary investment properties.

Strategic Tips for Seniors and Real Estate Investors

Navigating the reverse mortgage landscape requires a transition from emotional homeownership to pragmatic asset management. Here are several expert tips to consider:

- The 60% Rule Awareness: Under HUD guidelines, you are generally limited to accessing 60% of your available loan proceeds in the first year. Therefore, if you are planning to buy an investment property, timing is everything. Plan your acquisition cycles around this disbursement schedule.

- Maintain Your Asset: To keep the loan in good standing, you must continue to pay property taxes and homeowners insurance. In Alabama, where property taxes are relatively low compared to the national average, this is often a manageable requirement that protects your long-term equity.

- HECM for Purchase: Investors often overlook the "HECM for Purchase" program. If you are looking to downsize or move to a more profitable location: such as relocating closer to the Gulf Coast: you can buy a new primary residence with a reverse mortgage, preserving more of your cash for other investments.

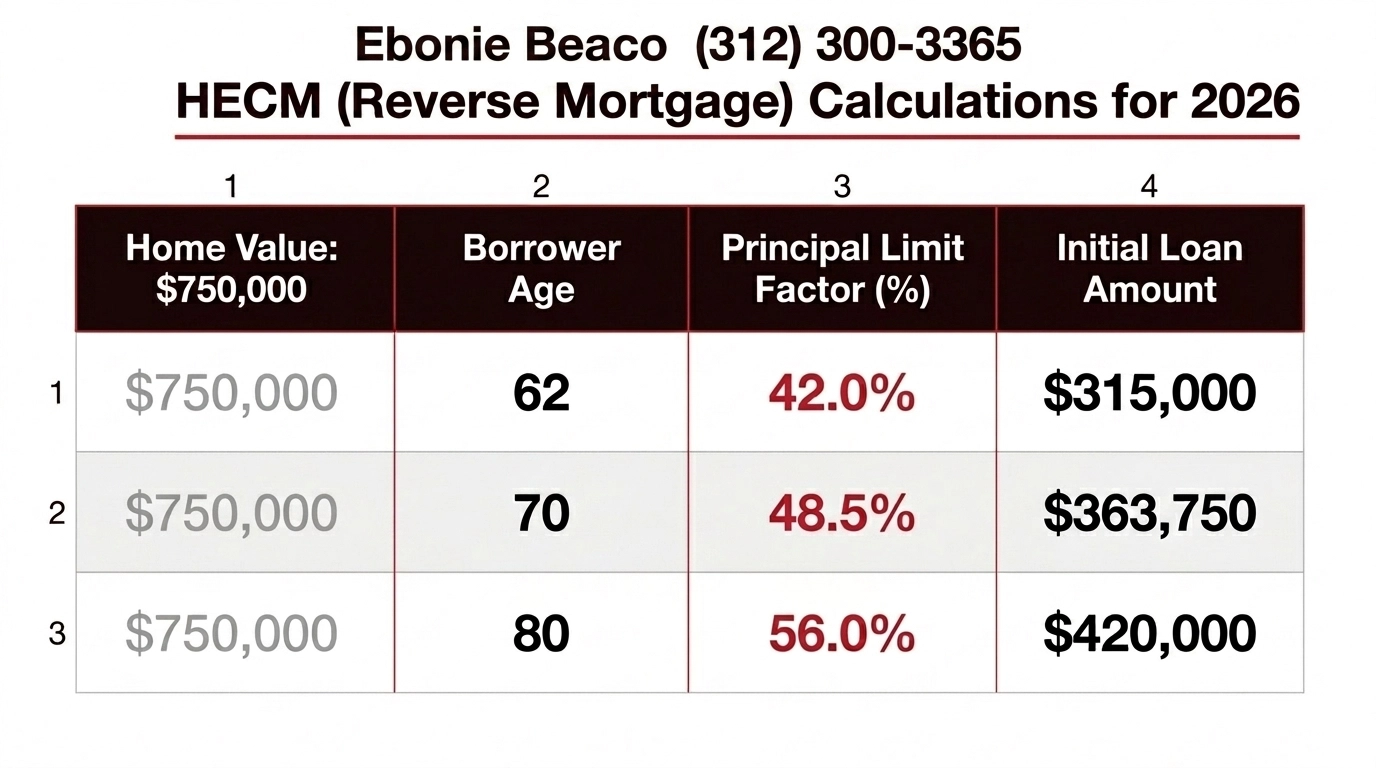

The Math Behind the Money: Reverse Mortgage Calculations

The amount of money you can receive is determined by the "Principal Limit." This calculation is not arbitrary; it is based on three primary factors: the age of the youngest borrower, the current interest rate, and the lesser of the home’s appraised value or the FHA limit.

As illustrated in the table above, the older the borrower, the higher the Principal Limit Factor (PLF). Thus, an 80-year-old borrower in Birmingham with a $750,000 home will have access to significantly more capital than a 62-year-old in the same neighborhood. This is due to the shorter projected life expectancy, which reduces the lender’s risk.

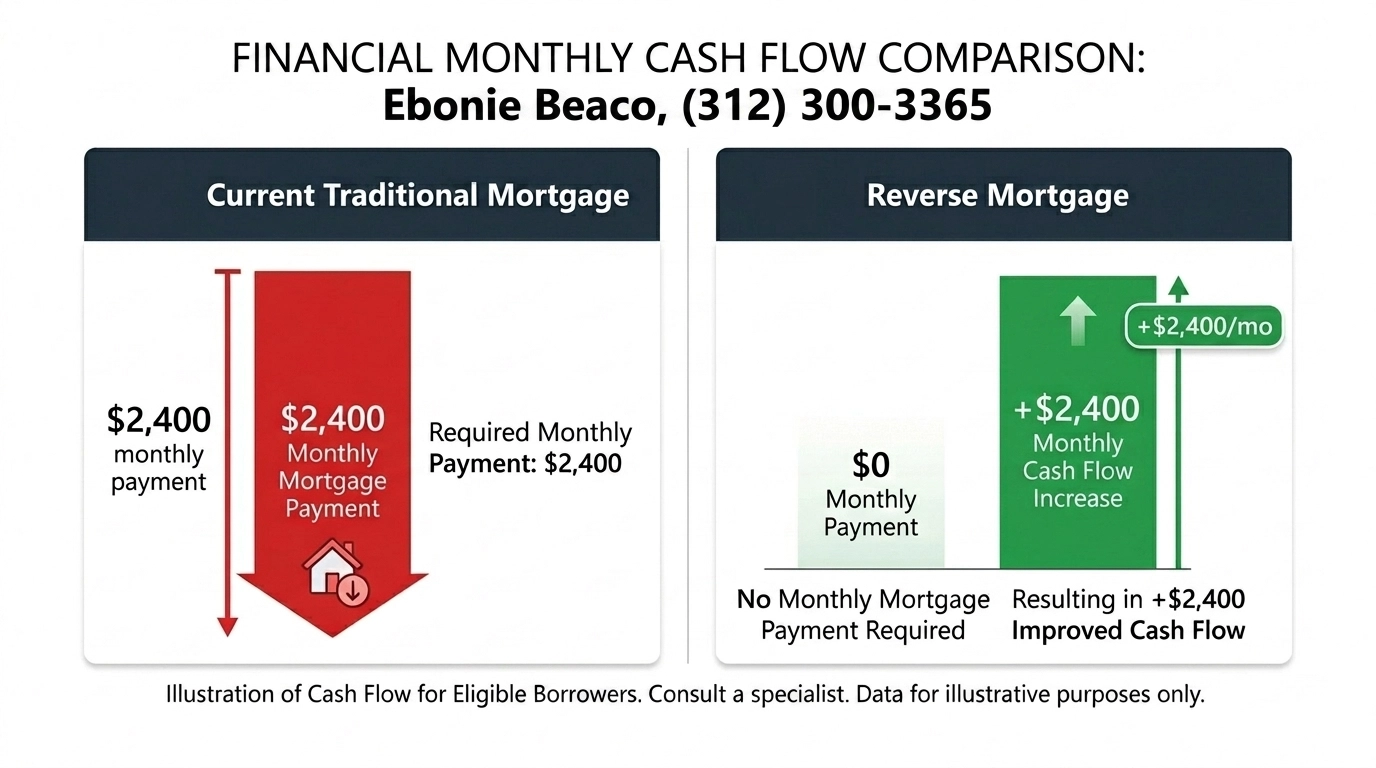

Fixed Debt vs. Liquid Equity

Moreover, the reverse mortgage eliminates the monthly principal and interest payment. If you currently owe $150,000 on a traditional mortgage with a $1,500 monthly payment, a reverse mortgage would pay off that existing debt first. Consequently, you instantly increase your monthly cash flow by $1,500: capital that can be redirected into a REIT or a property management fund.

Case Study: Birmingham and Mobile Investment Scenarios

Scenario 1: The Birmingham Equity Extraction

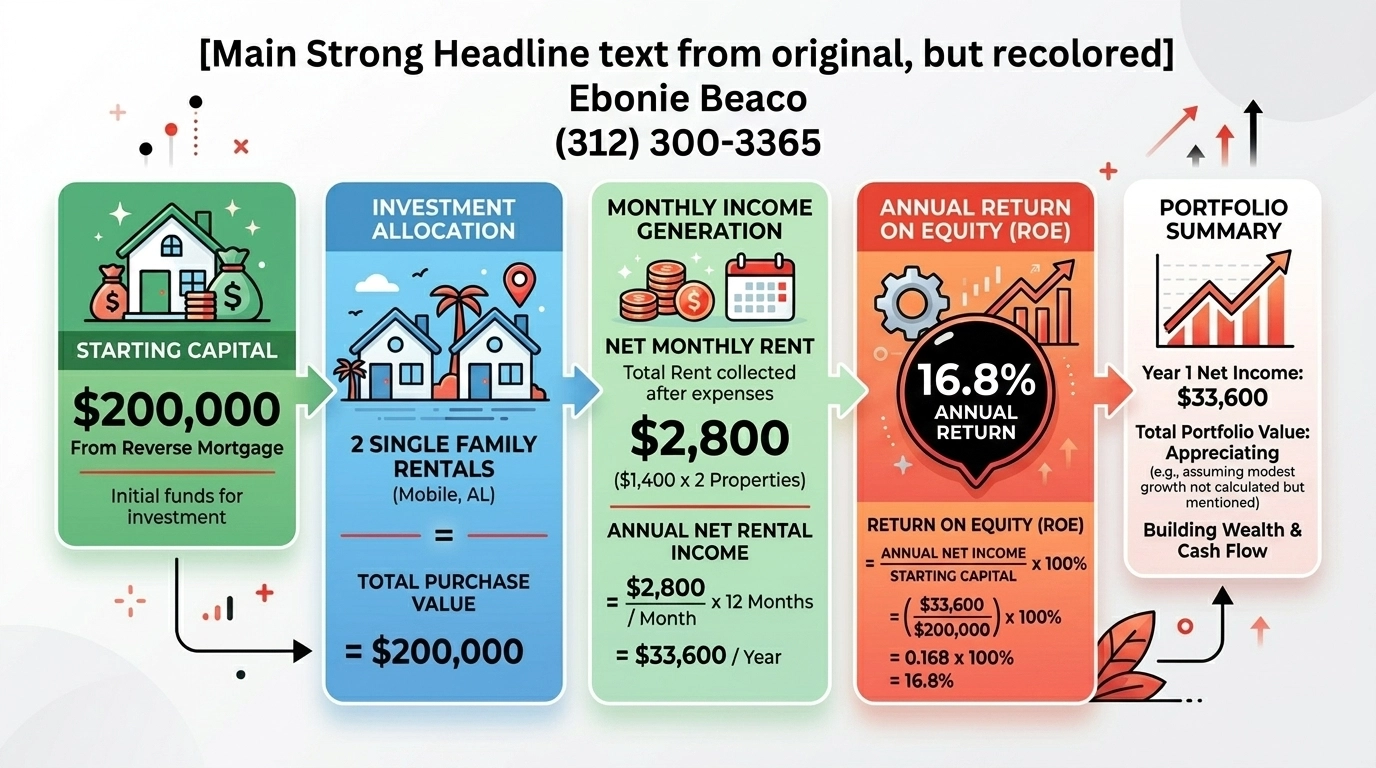

Consider a couple in Vestavia Hills, AL, aged 68, living in a home valued at $600,000 with no existing mortgage. By securing a reverse mortgage, they access approximately $250,000 in a line of credit. Instead of using this for lifestyle expenses, they utilize $200,000 to purchase a duplex in the revitalized Avondale area.

- Result: They remain in their primary home with $0 monthly mortgage payments while generating $2,400 in gross monthly rental income from the new duplex. Their net worth remains stable, but their liquid cash flow has exploded.

Scenario 2: The Mobile Retirement Relocation

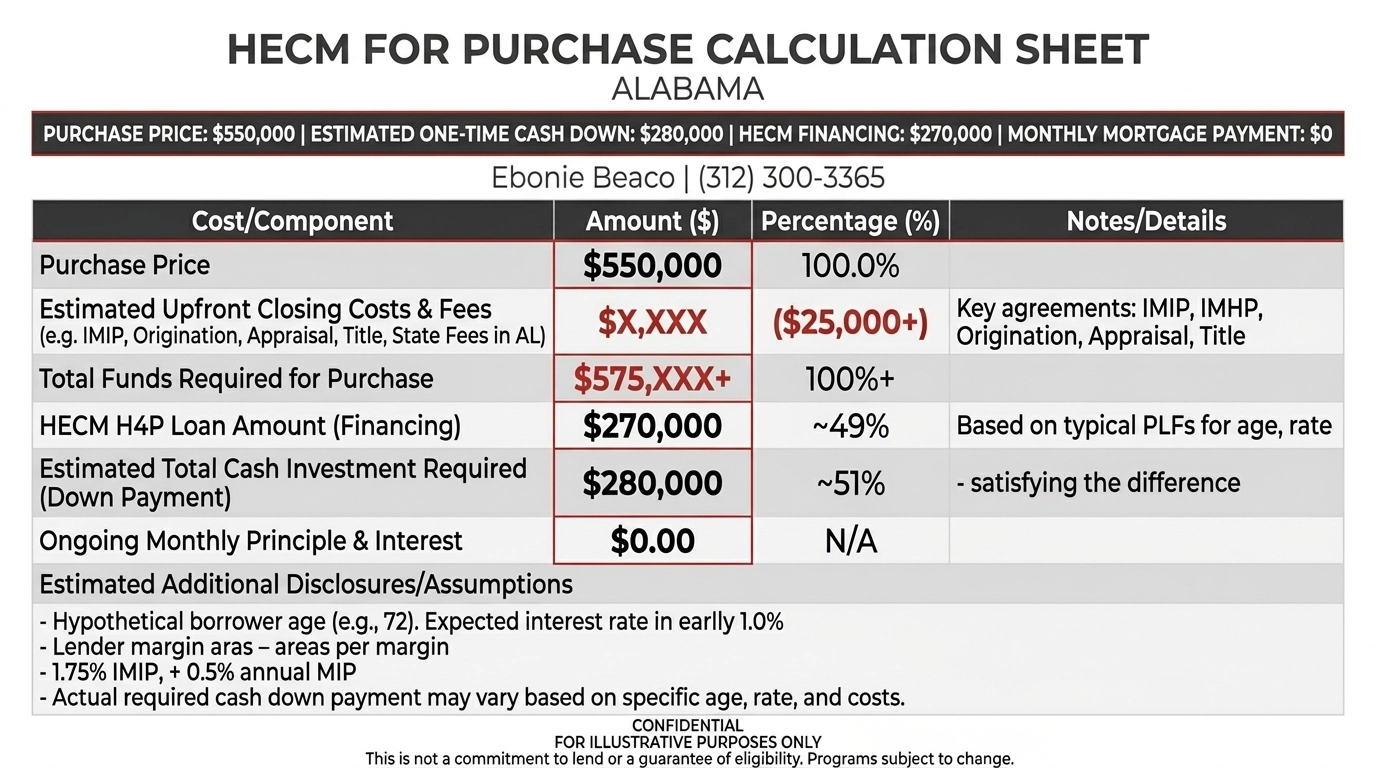

A 72-year-old homeowner in Mobile wants to move into a smaller condo near the bay. Using the HECM for Purchase, they buy a $400,000 condo with a one-time investment of approximately $210,000.

- Result: They sell their previous large family home, keep the remaining proceeds as cash reserves for future real estate flips, and live in the new condo without a monthly mortgage payment for life.

How to Use a Reverse Mortgage to Invest in Real Estate

The most effective way to grow your portfolio using this tool is through equity recycling. When you have substantial equity sitting in your primary residence, it is effectively a "lazy asset." It earns nothing but market appreciation.

- Extract: Use a HECM Line of Credit to access the equity. Unlike a Home Equity Line of Credit (HELOC), the HECM line of credit cannot be frozen or reduced by the bank as long as you meet the loan terms, and it actually grows over time at the same rate as the loan’s interest.

- Deploy: Use the funds as a cash down payment on a high-yield rental property in Alabama’s growing markets, such as Huntsville (driven by the aerospace industry) or Tuscaloosa (driven by the university).

- Compound: Use the rental income from the new property to fund a life insurance policy or a brokerage account, or even to pay down the balance of the reverse mortgage if you wish to preserve equity for your heirs.

Growing Your Investment Portfolio: The HECM Advantage

For the strategic investor, the HECM is not an "end-of-life" product; it is a "mid-life" financial catalyst. By leveraging the non-recourse nature of the loan: meaning you or your heirs will never owe more than the home is worth: you mitigate significant risk.

Furthermore, because the proceeds from a reverse mortgage are typically considered loan advances rather than income, they are generally tax-free. This allows you to invest "100-cent dollars" rather than "70-cent dollars" after taxes, drastically increasing your purchasing power in the Alabama real estate market.

Frequently Asked Questions

Does the bank own my home?

No. You remain the owner of the home and keep the title. The lender simply holds a lien on the property, much like a traditional mortgage.

What happens if the home value drops in Alabama?

The HECM is a non-recourse loan. If the home value in Birmingham or Mobile drops below the loan balance, the FHA insurance fund covers the difference. You or your heirs are not personally liable for the deficit.

Can I still leave the home to my children?

Yes. Your heirs can choose to pay off the reverse mortgage balance and keep the home, or sell the home and keep any remaining equity after the loan is paid.

Is this a good strategy for every investor?

This is a long-term strategy. If you plan to move out of your primary residence within 2-3 years, the upfront costs (such as mortgage insurance premiums) may not be worth the investment. However, for those planning to age in place while building a legacy, it is a powerful tool.

Ready to Strategize Your Alabama Real Estate Future?

Unlock the hidden potential in your home equity today. Whether you are looking to increase your monthly cash flow or expand your rental portfolio, I am here to provide the expert guidance you need to make a calculated move.

Ebonie Beaco - Mortgage Strategist | NMLS #2389954 📞 312-392-0664 🌐 www.HomeLoansNetwork.com

#ReverseMortgage #AlabamaRealEstate #PropertyInvestment #HomeEquity #FinancialPlanning