The Ultimate Guide to DSCR Loans for Chicago Multi-Family Investors

If you have spent any time looking at the real estate market in Chicago, you know that multi-family properties are the backbone of the city’s housing landscape. From the classic grey-stones in Logan Square to the sprawling brick four-units in Avondale, these buildings represent one of the most effective ways to build wealth. However, traditional financing often creates a bottleneck for active investors. This is where the Debt Service Coverage Ratio (DSCR) loan comes in as a game-changer.

As a Chicago DSCR loan lender, we see investors hitting walls with conventional banks because their tax returns show high write-offs or their personal debt-to-income ratio is stretched thin. DSCR loans bypass these personal financial hurdles by focusing entirely on the property’s ability to generate cash flow.

Understanding the DSCR Concept

DSCR (Debt Service Coverage Ratio): A financial metric used by lenders to measure a property's ability to cover its debt obligations based on its annual net operating income.

In practical terms, a DSCR loan means the lender looks at the rental income of the property versus the mortgage payment (Principal, Interest, Taxes, Insurance, and Association dues). If the property makes enough money to pay for itself, you qualify. Your personal income, employment history, and DTI (Debt-to-Income) are not part of the calculation.

Explore how this works for a typical Chicago investor looking to scale their portfolio without the red tape of traditional underwriting.

A classic Chicago four-unit multi-family building in the Logan Square neighborhood, showcasing the type of high-demand rental property ideal for DSCR financing.

A classic Chicago four-unit multi-family building in the Logan Square neighborhood, showcasing the type of high-demand rental property ideal for DSCR financing.

The Logan Square Cash-Out Scenario

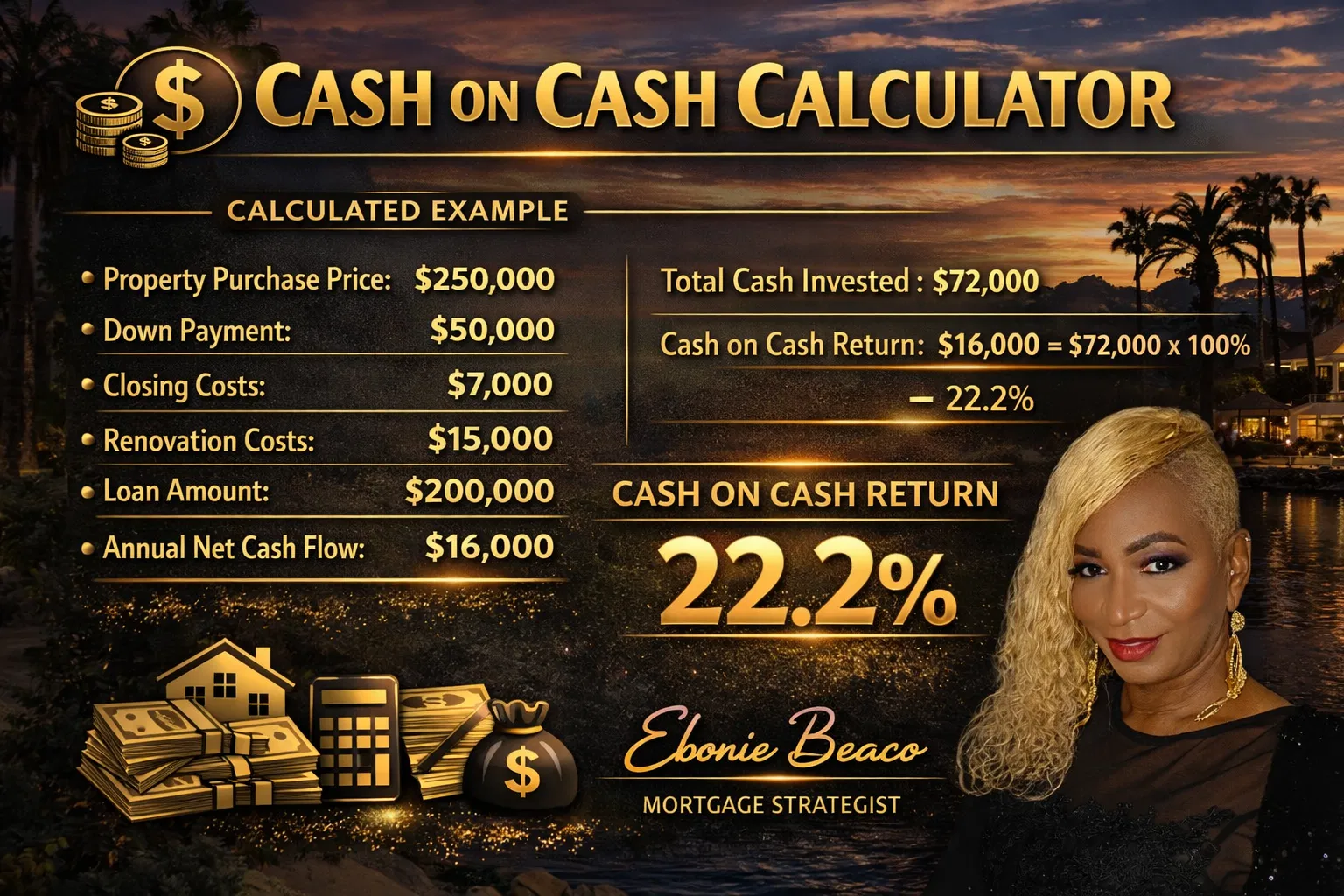

Let’s look at a real-world example of how a Chicago investor can use a DSCR loan to fuel growth. Imagine you own a 4-unit building in Logan Square that has seen significant appreciation over the last few years. You want to buy another property, but you don't want to sell your current "cash cow." Instead, you decide to perform a cash-out refinance.

The Property Profile

- Property Type: 4-Unit Multi-Family (Logan Square)

- Current Appraised Value: $950,000

- Existing Mortgage Balance: $600,000

- Goal: Pull out $100,000 in equity for a down payment on a new investment property.

The DSCR Calculation

To qualify, the lender will analyze the rental income against the new proposed debt service.

- Gross Monthly Rental Income: $9,000 (4 units at $2,250 each)

- Proposed Monthly Mortgage Payment (PITI): $7,200

- The Formula: $9,000 / $7,200 = 1.25 DSCR

In this case study, a 1.25 DSCR ratio is considered very strong. Most Chicago DSCR loan lenders look for a ratio of 1.0 to 1.25. Because the ratio is 1.25, the property is generating 25% more income than the cost of the debt, making it a low-risk loan for the lender and a profitable asset for you.

By using this strategy, you successfully pull out $100,000 to fund your next deal while keeping the Logan Square property in your portfolio. You can jump in on new opportunities quickly without waiting for a traditional bank to spend 60 days reviewing your personal tax returns.

Why Chicago Investors Choose DSCR Over Conventional Loans

The Chicago market moves fast. Whether you are looking at Lincoln Park real estate insights or exploring the suburbs, the competition for multi-family buildings is fierce. Here is why DSCR is often the superior choice for serious investors:

No Personal Income Verification

Traditional loans require W-2s, pay stubs, and years of tax returns. For self-employed investors or those with many business write-offs, this is a major hurdle. DSCR loans do not care about your personal income.

Faster Closing Times

Because the underwriting is focused on the property and not your entire life’s financial history, the process is streamlined. This is critical when you need to close a deal before another investor outbids you.

Flexibility for LLCs

Many savvy investors hold their properties in an LLC for liability protection. Conventional lenders often struggle with this, but DSCR loans are specifically designed for properties held in an LLC or corporate entity.

Unlimited Portfolio Scaling

Conventional lenders often cap the number of financed properties you can have (usually 10). DSCR lenders typically have no such limit. This allows you to grow from a 4-unit building to a 50-unit portfolio without hitting a wall.

Key Requirements for Chicago DSCR Loans

While the property does the heavy lifting, there are still basic requirements you need to meet to access the best rates and terms.

- Credit Score: Usually a minimum of 620, though higher scores (720+) unlock much better interest rates.

- Loan-to-Value (LTV): For a purchase, you usually need a 20% to 25% down payment. For a cash-out refinance, you can typically access up to 75% of the property's value.

- Property Condition: The units must be in "tenant-ready" condition. If the property is a total gut-rehab, you might look into fix and flip loans instead.

- Prepayment Penalties: DSCR loans often come with a prepayment penalty (e.g., 3-year or 5-year). It is important to compare options to ensure the penalty aligns with your long-term exit strategy.

A professional financial chart showing the breakdown of a DSCR calculation, comparing gross rental income against total monthly debt service for a Chicago investment property.

A professional financial chart showing the breakdown of a DSCR calculation, comparing gross rental income against total monthly debt service for a Chicago investment property.

Navigating the Current Market

The economy is always shifting. Many investors ask, should I buy now or wait? In Chicago, waiting often means missing out on appreciation and rental growth. While interest rates have been a topic of discussion, the DSCR model allows you to focus on the spread between your rent and your payment. If the math works today, the deal works today.

For those managing short-term rentals, DSCR loans can also be applied to Airbnb properties. Lenders will often use "AirDNA" data or documented rental history to prove the property’s income potential. This is a massive advantage in neighborhoods like the West Loop or River North, where nightly rates can far exceed traditional monthly rents.

Accessing Your Equity for Growth

If you already own property in the Chicago suburbs or city limits, you are likely sitting on a significant amount of equity. A DSCR cash-out refinance is one of the most efficient ways to tap into that wealth without selling the asset.

Selling a property often triggers capital gains taxes, which can eat into your profits. By refinancing, you keep the asset, benefit from future appreciation, and get the liquid cash you need to buy your next property.

Compare your current mortgage rate and property value. If your building has a DSCR of 1.2 or higher, you are in a prime position to expand.

Strategy for Realtors and Professionals

If you are a realtor working with investors, understanding the DSCR product is essential. It allows you to help your clients close deals that a traditional bank would reject. When you can show a client how to buy a 4-unit building using only the building’s income to qualify, you become more than an agent: you become a strategist.

We are built for realtors who want more closings. By partnering with a Chicago DSCR loan lender, you can provide your clients with creative financing solutions that keep the wheels of the local real estate market turning.

Final Steps to Securing Your Loan

Securing a DSCR loan starts with a clear analysis of your property’s income potential. Before you apply, gather your current lease agreements or, if the property is vacant, look at market rent comparables (Form 1007 or 1025).

- Analyze the Income: Ensure your gross rents cover at least 1.2 times the estimated mortgage payment.

- Check Your Credit: Even though it is a business-purpose loan, your credit score determines the interest rate.

- Identify Your Next Deal: If you are doing a cash-out refi, have your next purchase target ready so you can move quickly once the funds hit your account.

The Chicago multi-family market offers incredible opportunities for those who know how to use the right tools. DSCR loans are the lever that allows you to move larger assets with less personal friction.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664