Strategic Wealth in Arkansas: Using Reverse Mortgages to Build Your Real Estate Portfolio

For many homeowners in Arkansas, whether you are settled in the historic neighborhoods of Little Rock or the rapidly expanding corridors of Fayetteville, home equity is often viewed as a static asset. It is the "safety net" that sits idle while the rest of your portfolio works. However, in the current economic landscape, leaving hundreds of thousands of dollars in "dead equity" is a strategic oversight.

A reverse mortgage, specifically the Home Equity Conversion Mortgage (HECM), is no longer just a "loan of last resort." In fact, it has evolved into a sophisticated financial instrument used by savvy investors to increase liquidity, hedge against market volatility, and aggressively expand real estate portfolios. This article explores how Arkansas residents aged 62 and older can transition from a "Commission Mindset" to a "Residual Reality" by leveraging their primary residence to build long-term wealth.

Understanding the HECM: Moving Beyond the Myths

To understand the strategic value of a reverse mortgage, one must first strip away the common misconceptions. A reverse mortgage is a non-recourse loan that allows you to convert a portion of your home equity into cash without the requirement of a monthly mortgage payment. You still own the home; you simply defer the repayment of the loan until you move out, sell the home, or pass away.

How It Works in Arkansas

In Pulaski and Washington counties, property values have seen steady appreciation. Under the Federal Housing Administration (FHA) guidelines, the HECM limit is currently substantial, allowing homeowners in higher-value areas like the Heights in Little Rock or the hills of Fayetteville to access significant capital.

- No Monthly Payments: While you must continue to pay property taxes, homeowners insurance, and maintain the property, you are not required to make a monthly principal or interest payment.

- Non-Recourse Protection: You or your heirs will never owe more than the home is worth at the time of sale. If the market dips in Arkansas, the FHA insurance covers the gap.

- Flexible Distribution: You can receive funds as a lump sum, a monthly tenure, or a growing line of credit.

Strategic Reverse Mortgage Tips for the Arkansas Investor

If you are considering this path, you must approach it with an owner’s perspective. This isn’t about spending; it’s about reallocation.

- Prioritize the Line of Credit (LOC): If you don’t need the cash immediately for a purchase, opt for the Line of Credit. The unused portion of the HECM LOC grows over time at the same interest rate as the loan balance. This is "compounding liquidity" that can be used for future investments.

- Timing is Everything: Many homeowners wait until they are 75 or 80 to look at a reverse mortgage. However, starting at 62 allows the Line of Credit more time to grow, providing a larger "war chest" for when Arkansas real estate opportunities arise.

- Consult with Heirs: A reverse mortgage affects the estate. Strategic owners treat this as a family business discussion, explaining how the increased liquidity today will lead to a larger overall family portfolio tomorrow.

Case Studies: The Arkansas "Property Swap" Strategy

Case Study 1: The Little Rock Downsize-to-Invest

A couple in Little Rock owned a large family home in Chenal Valley worth $650,000, fully paid off. They wanted to downsize but didn't want to tie up all their cash in a new smaller home. The Strategy: They sold their home and used a HECM for Purchase to buy a $400,000 bungalow in a quieter neighborhood. The Result: Instead of paying $400,000 in cash, they put down roughly $180,000 (based on their age) and kept $470,000 in liquid cash. They used $300,000 of that cash to purchase two rental properties in North Little Rock, generating $3,500 in monthly passive income while living in their new home with no mortgage payment.

Case Study 2: The Fayetteville Equity Growth Hedge

An investor in Fayetteville with a $500,000 home and a remaining $100,000 traditional mortgage was struggling with cash flow. The Strategy: They replaced the traditional mortgage with a HECM. The Result: This eliminated their $1,500 monthly mortgage payment. Moreover, they secured a $150,000 Line of Credit. When a small apartment complex became available near the University of Arkansas, they used the LOC for the down payment, securing a commercial loan for the rest. They effectively used the "dead equity" in their primary home to acquire a high-yield asset.

The Mathematics of Wealth: Reverse Mortgage Calculations

Understanding the numbers is the difference between a guess and a strategy. Below are the key calculations that drive these decisions.

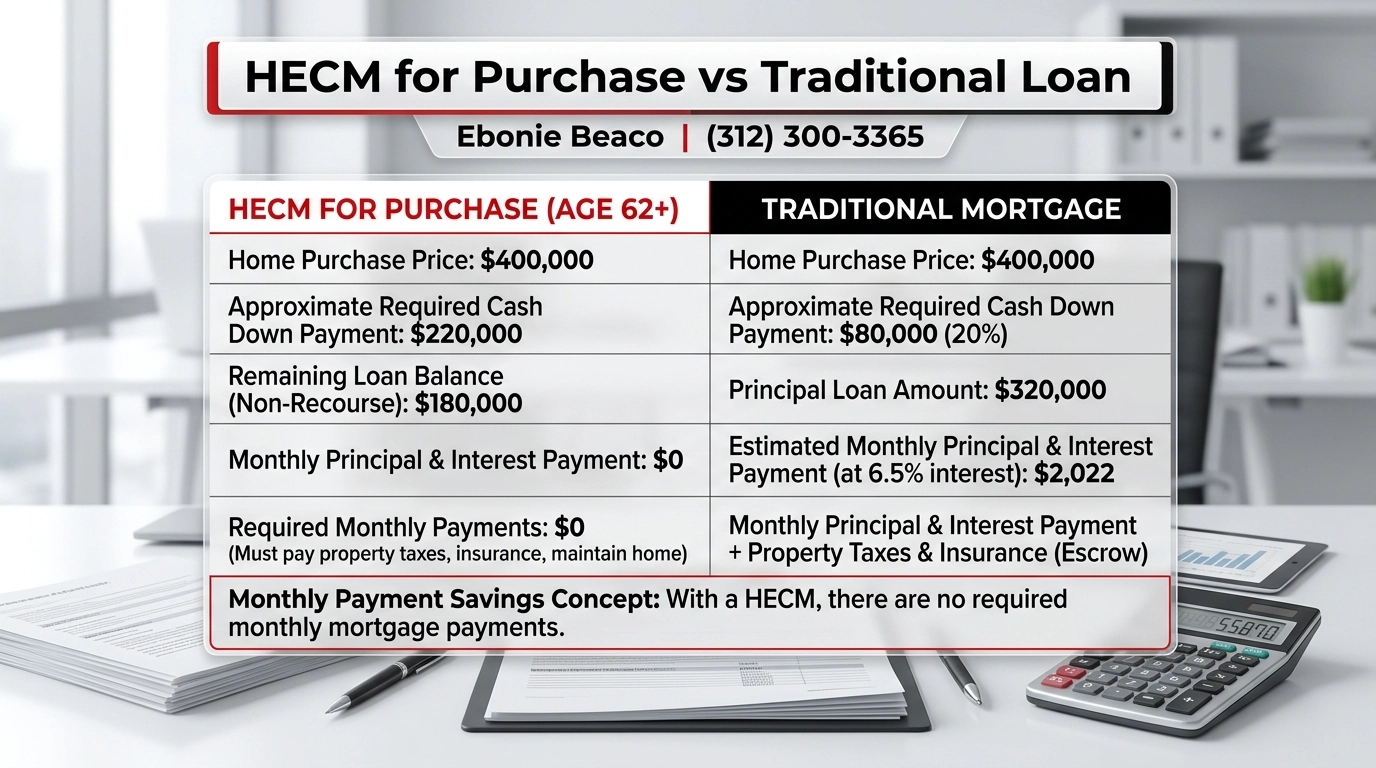

1. Traditional vs. HECM for Purchase

When purchasing a new home, the HECM for Purchase (H4P) allows you to preserve significantly more of your liquid capital.

As shown in the table, the HECM for Purchase requires a larger initial down payment than a 20% traditional loan, but it eliminates the $2,800 monthly drain on your cash flow. For an investor, that $2,800 is better served being reinvested into a diversified portfolio or used to service debt on a multi-family property.

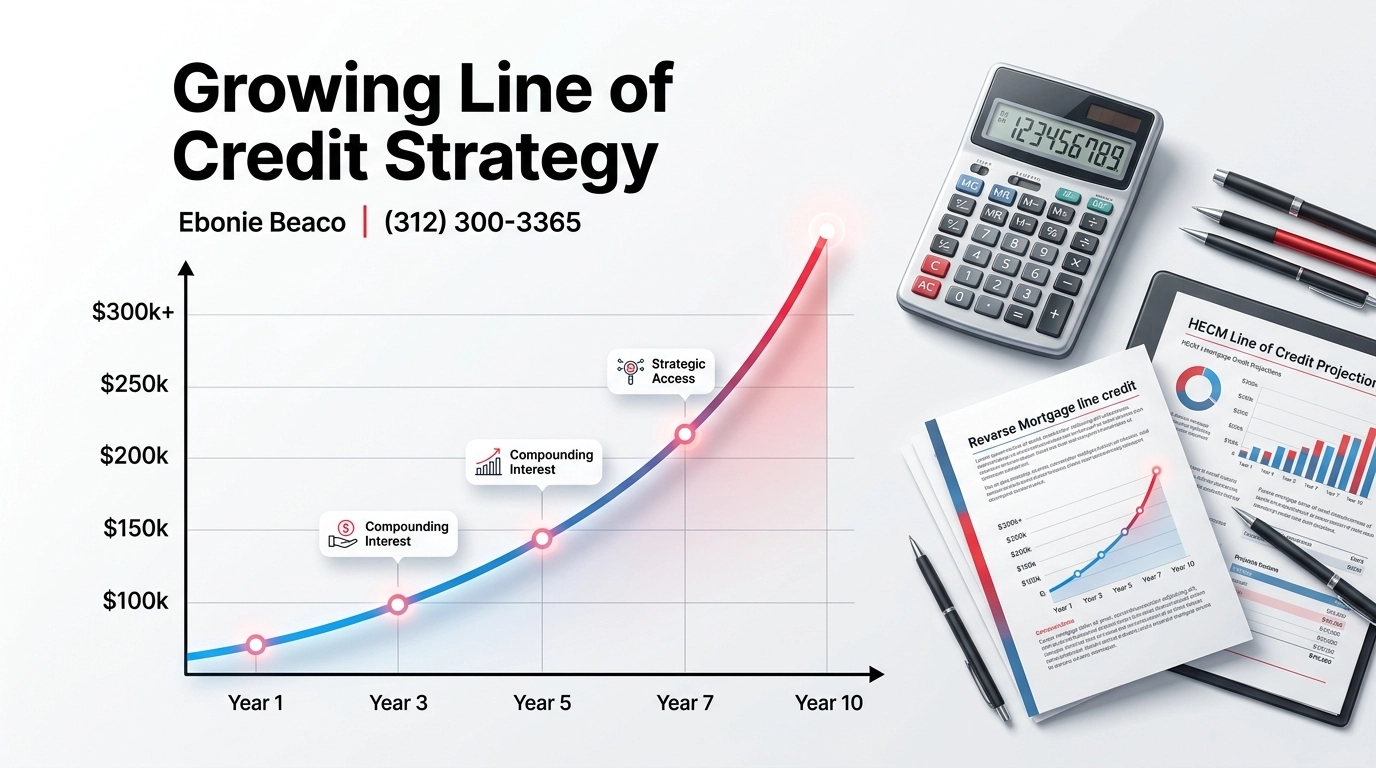

2. The Power of the Growing Line of Credit

The HECM Line of Credit is unique because the available credit grows regardless of the home's value.

If you secure a $150,000 LOC at age 62 and the growth rate (Interest + MIP) is 5%, your available "investment pool" grows to nearly $245,000 in ten years, even if you never put another penny into the home. This is the definition of "deferred gratification."

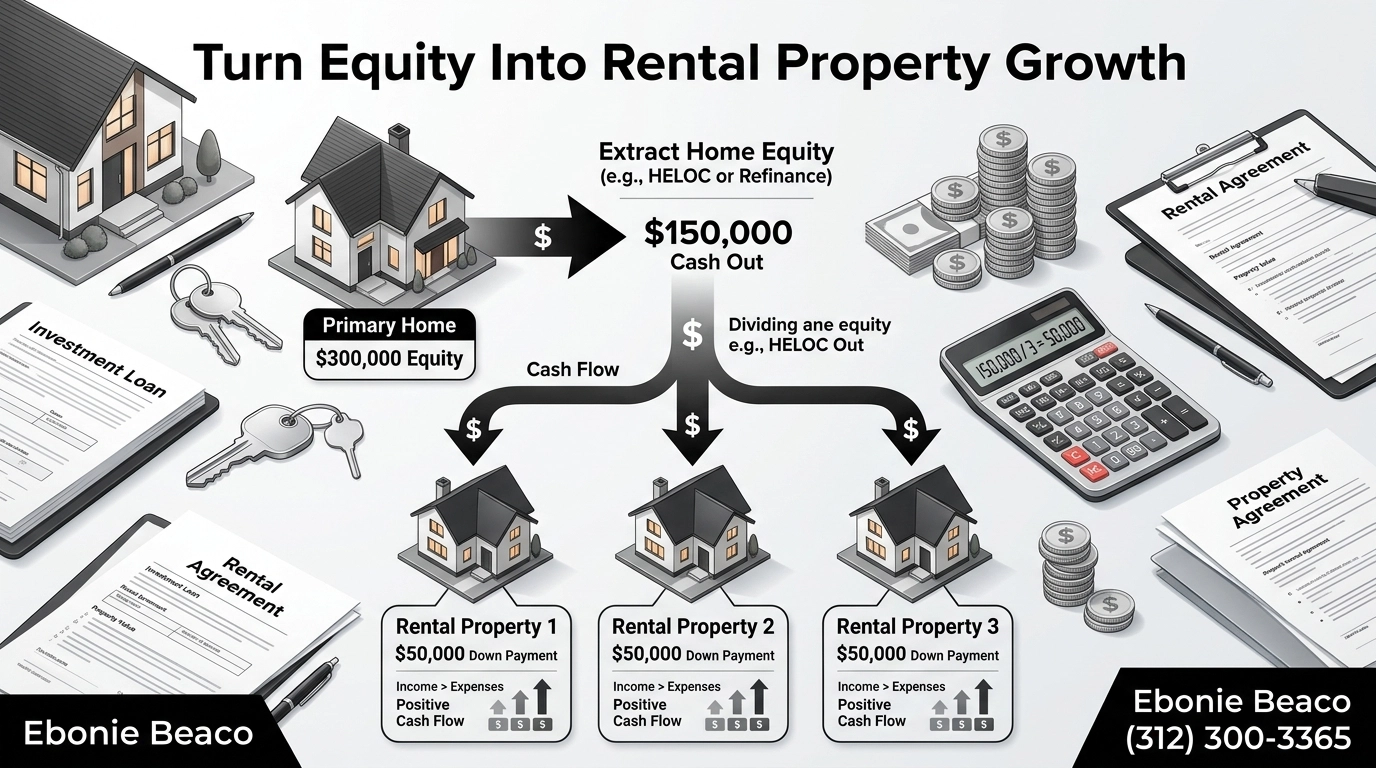

3. Portfolio Expansion via Equity Extraction

The most aggressive strategy involves using the HECM to fund the acquisition of multiple rental units.

In this Fayetteville-based calculation, the investor transforms one primary residence into a four-property portfolio. By using the HECM to buy the new primary home, they free up $320,000 in cash. That cash then serves as the 25% down payment for three rental units, drastically increasing the net monthly cash flow.

How to Use a Reverse Mortgage to Invest in Real Estate

The process is structured and requires careful mortgage basics knowledge. To use a HECM for investment, follow these steps:

- Eliminate Existing Debt: Use the HECM to pay off your current traditional mortgage. This immediately improves your debt-to-income ratio, making it easier to qualify for traditional investment property loans.

- Establish a Line of Credit: This becomes your "Emergency Fund" or "Acquisition Fund."

- Buy a Rental Property: Use the proceeds from the HECM as a cash down payment on a non-owner occupied property. Since the HECM doesn't require a monthly payment, your "Borrowing Power" remains high.

- The Buy-and-Hold: Use the rental income to pay down the HECM balance if you wish to preserve equity for heirs, or reinvest that income into a third property.

Growing Your Portfolio: The Different Paths

There is no "one-size-fits-all" in real estate. Depending on your goals in Arkansas, you might choose:

- The Consolidation Path: Selling several smaller, high-maintenance properties and using a HECM for Purchase to buy one high-end "forever home" while keeping the remaining cash in a high-yield savings or brokerage account.

- The Family Legacy Path: Using a HECM to pay for the closing costs and down payments for your children or grandchildren to buy their first homes, effectively "gifting" them their inheritance early so they can start building their own equity.

- The Passive Income Path: Using a HECM to purchase a low-maintenance condo and using the leftover cash to buy into a Real Estate Investment Trust (REIT) or a private equity real estate fund.

FAQ: Frequently Asked Questions

Does the bank own my home? No. You remain the owner of the home and the title remains in your name. The bank simply holds a lien, just like a traditional mortgage.

Can I still leave the home to my children? Yes. When you pass away, your heirs can choose to pay off the loan balance and keep the home, or sell the home and keep the remaining equity.

What if the loan balance becomes higher than the home value? Arkansas is a non-recourse state for HECMs. You or your heirs will never be held personally liable for a deficit. The FHA insurance fund covers the difference.

Is the money from a reverse mortgage taxable? Generally, no. The IRS considers the funds to be a loan advance, not income. This makes it a highly tax-efficient way to fund your retirement or new investments.

Conclusion: Thinking Like an Owner

The "Rigid Bank Terms" of traditional lending often fail to meet the needs of experienced homeowners who want to maximize their retirement years. By choosing the "Flexible Funding" of a reverse mortgage, you are choosing to put your equity to work. Whether you are in Little Rock, Fayetteville, or anywhere in the Natural State, the opportunity to turn your home into a cash-generating machine is available now.

Ready to Build Your Strategy?

Ebonie Beaco - Mortgage Strategist | NMLS #2389954 📞 312-392-0664 🌐 www.HomeLoansNetwork.com

Call or text today to get started on your customized Arkansas wealth strategy.

#ArkansasRealEstate #ReverseMortgage #WealthStrategy #RealEstateInvestment