Scaling Your Florida Airbnb Portfolio with DSCR Financing

Florida continues to stand as the primary destination for short-term rental investors.

Between the theme parks of Orlando and the coastal appeal of the Panhandle, the opportunity to generate high rental yields is immense.

However, many investors hit a wall when they try to scale their portfolios using traditional financing.

Conventional banks often focus on your personal debt-to-income (DTI) ratio, which can limit how many properties you can own before you appear "too risky" on paper.

This is where the DSCR loan changes the game for Florida real estate professionals and investors.

Understanding the DSCR Loan Model

Debt Service Coverage Ratio (DSCR): A financial metric used by mortgage lenders to measure the ability of an investment property to cover its own monthly debt payments through its generated income.

Lenders use this ratio to determine if a property is a viable investment on its own merits, rather than looking at your personal W-2 income or tax returns.

For the active Florida Airbnb investor, this means your ability to acquire a vacation home in Kissimmee or Miami is based on what that specific house earns on the short-term rental market.

Jump in and explore how this specific loan type allows you to scale without the red tape of traditional mortgage underwriting.

Why Florida is the Epicenter for Airbnb Financing

Florida is a unique market because it offers year-round demand.

While other states might see a massive dip in tourism during the winter, Florida’s "snowbird" season and spring break crowds keep occupancy rates high.

When you work with a Florida DSCR loan lender, you are tapping into a program designed for this specific high-velocity market.

These loans are considered Non-QM (Non-Qualified Mortgage) products.

Non-QM Mortgage: A category of loans that do not follow the strict federal guidelines of conventional mortgages, allowing for more flexible qualification criteria like bank statements or property cash flow.

Because these loans don’t need to meet Fannie Mae or Freddie Mac standards, they are perfect for the self-employed investor or the entrepreneur looking to grow a fleet of short-term rentals quickly.

The Power of the "Projected Income" Strategy

One of the biggest hurdles for new Airbnb investors is financing a property that doesn't have a history of rental income yet.

Most traditional lenders want to see two years of tax returns showing rental profit.

In a fast-moving market like Orlando, you cannot wait two years to prove a property works.

Modern DSCR programs allow lenders to use projected income data from sources like AirDNA or Rabbu.

This data provides a reliable estimate of what a property will earn based on comparable Airbnbs in the immediate area.

Case Study: Scaling in Orlando with AirDNA Data

Let’s look at a real-world scenario involving an investor named Sarah who wanted to purchase a vacation rental near the Disney theme parks.

The Scenario: Sarah found a modern 4-bedroom townhome in a resort community priced at $550,000. She had the 25% down payment ready but was already carrying three other mortgages, making her DTI ratio too high for a conventional loan.

The Solution: She applied for a Florida Airbnb financing loan using a DSCR program. Instead of asking for her tax returns, the lender looked at the projected gross income for that specific zip code in Orlando.

The Financials:

- Purchase Price: $550,000

- Loan Amount (75% LTV): $412,500

- Estimated Monthly Payment (PITI): $3,200

- AirDNA Projected Monthly Revenue: $5,100

- DSCR Calculation: $5,100 / $3,200 = 1.59

Because the ratio was well above 1.0, the loan was approved quickly. Sarah didn't have to provide a single paycheck stub. She closed the deal under her LLC, protecting her personal assets and keeping the debt off her personal credit report.

Access more insights on how market shifts influence these types of deals by checking out this update on mortgage rates and buyer activity.

Key Benefits of Florida DSCR Loans for Investors

If you are a realtor or an investor, you need to know why this product is the preferred choice for scaling.

- No Limit on Properties: You can own 5, 10, or even 20 properties using DSCR financing. There is no "cap" like there is with conventional financing.

- LLC Financing: You can close the loan in the name of your business. This is a massive benefit for tax planning and liability protection.

- Faster Closings: Because the underwriting is focused on the property and the appraisal, these loans often close faster than traditional mortgages.

- No DTI Requirements: Your personal car payments, student loans, or existing home mortgages do not impact your ability to qualify for the next investment.

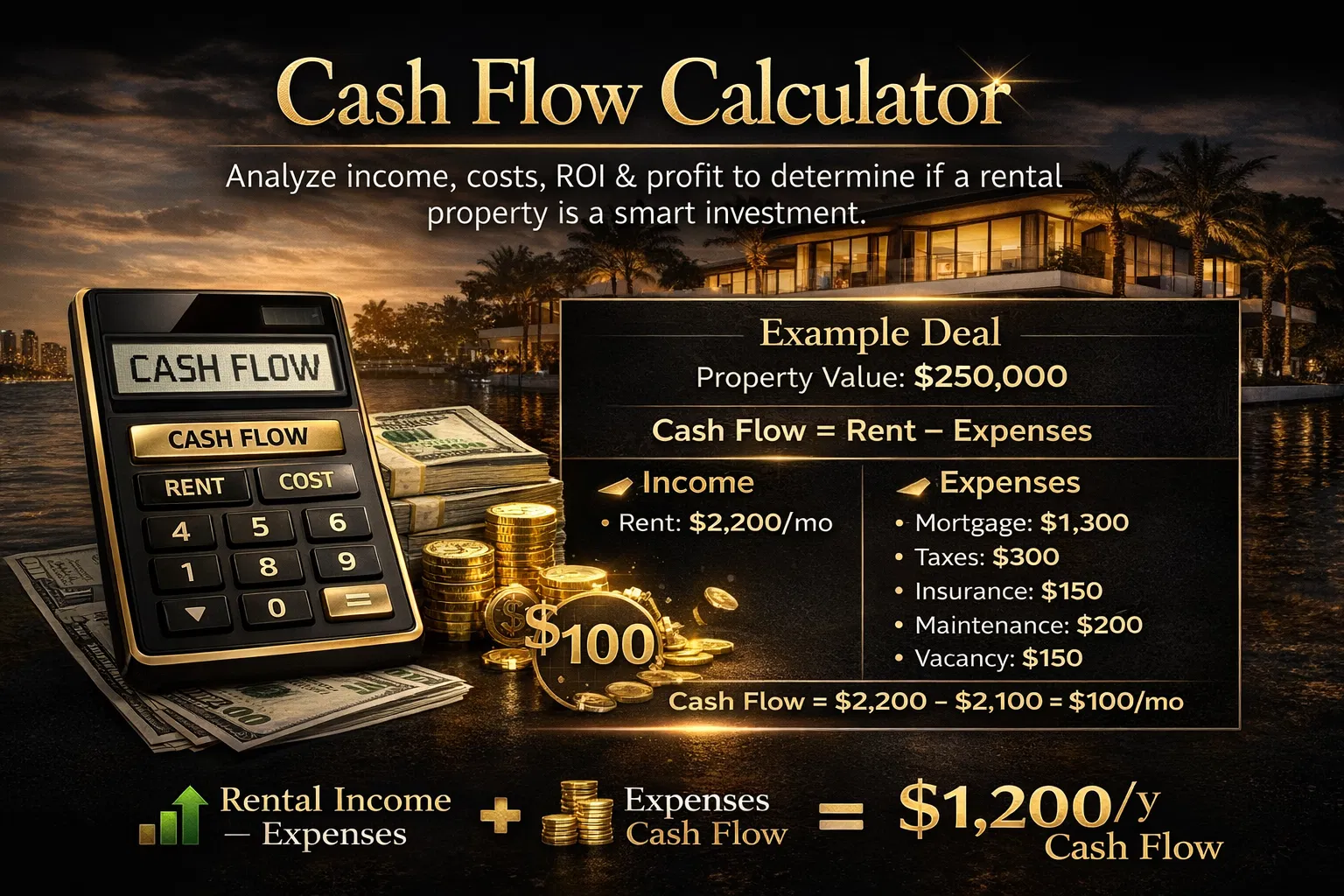

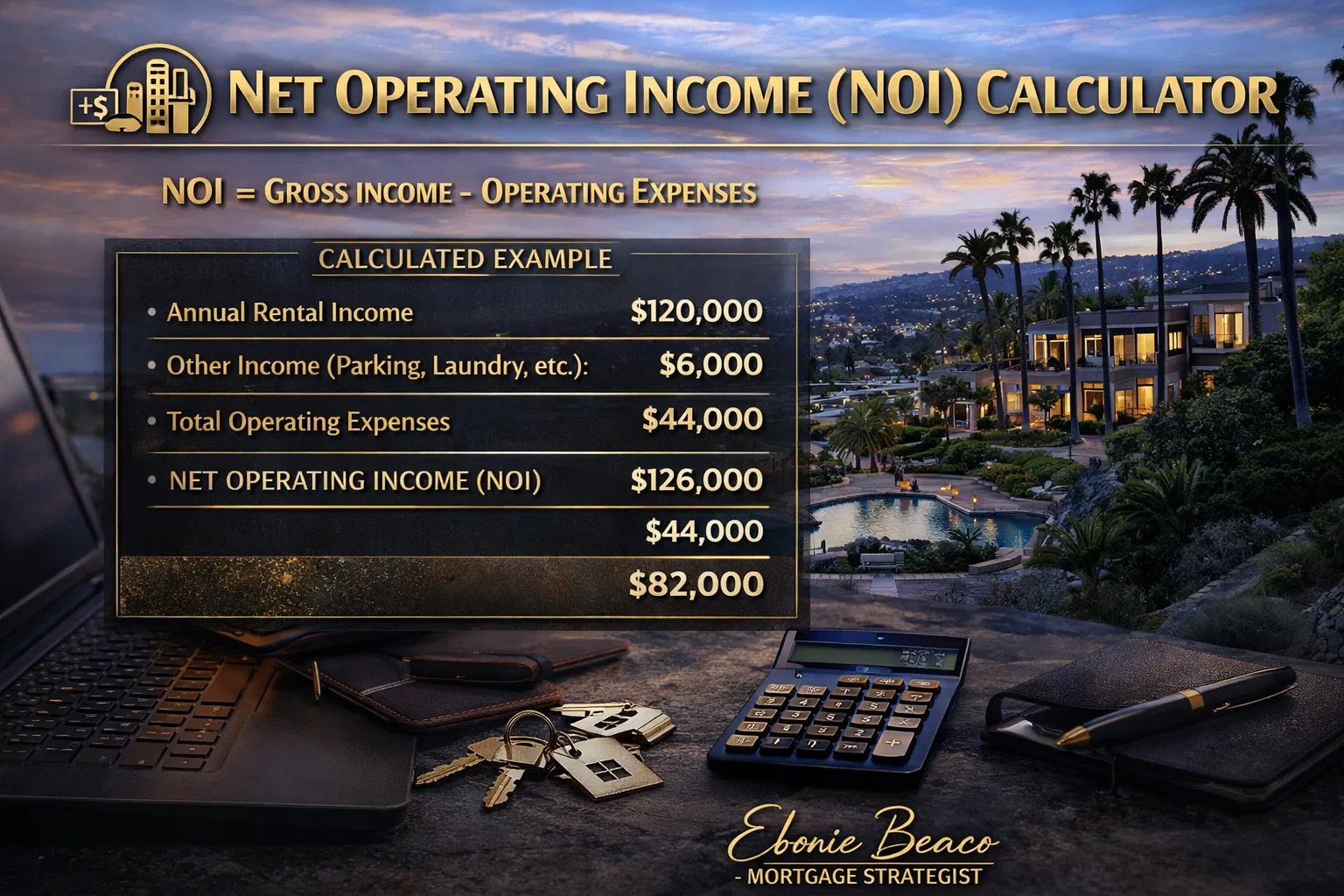

How to Calculate the DSCR for Your Next Deal

Before you reach out to a lender, you should run the numbers yourself.

The formula is simple: Gross Rental Income / Debt Service = DSCR.

Debt Service: The total monthly mortgage payment, including principal, interest, taxes, insurance, and any association fees (HOA).

If your property generates $4,000 a month and your total mortgage payment is $3,000, your ratio is 1.33.

Most lenders look for a ratio of 1.20 or higher, though some "no-ratio" programs exist for investors with high credit scores and significant down payments.

Compare this to other strategies, such as how interest rate changes affect your borrowing power, to see when the best time to lock in a rate might be.

Navigating the Florida Market as a Realtor

For realtors in markets like Tampa, Orlando, or the Panhandle, understanding DSCR loans is a competitive advantage.

When you have a client who is a "high-earning" professional but has a "messy" tax return due to business write-offs, a DSCR loan is their path to a "yes."

You can help your clients see the long-term value of the property by providing them with the income projections needed for these loans.

By positioning yourself as an expert in Florida Airbnb financing loans, you become more than just a real estate agent; you become a strategic partner in their wealth-building journey.

Explore how choosing the right lender can significantly improve your client's experience and your closing rate.

Essential Requirements for a DSCR Loan

While these loans are easier to qualify for in terms of income, they do have specific requirements you should keep in mind:

- Credit Score: Most programs require a minimum score of 640, though higher scores (720+) will unlock the most competitive interest rates.

- Down Payment: Expect to put down at least 20% to 25%. The more equity you have, the better your rate will be.

- Appraisal and Rent Schedule: The lender will order an appraisal that includes a "1007 Rent Schedule" to verify the long-term rental value, even if you plan to use it for short-term rental.

- Cash Reserves: Lenders usually want to see that you have 3 to 6 months of mortgage payments tucked away in a bank account as a safety net.

The Strategy of the Cash-Out Refinance

Once you have a few properties in your Florida portfolio, you can use a Cash-Out Refinance to continue your growth.

Cash-Out Refinance: A mortgage refinancing option where the new mortgage is for a larger amount than the existing one, allowing the borrower to take the difference in cash.

If your Orlando Airbnb has increased in value over the last two years, you can pull that equity out using a DSCR loan and use it as a down payment for your next property.

This "recycling" of capital is how professional investors build massive portfolios without constantly needing new infusions of personal cash.

Final Thoughts for Florida Investors

The Florida real estate market is fast, competitive, and highly rewarding for those who know how to use the right financial tools.

Whether you are looking at a beachfront condo in Destin or a single-family home near the attractions in Orlando, the DSCR loan is designed to help you succeed.

It removes the barriers of traditional lending and focuses on what truly counts: the performance of your investment property.

If you are ready to stop letting DTI limits hold you back and start scaling your Airbnb business, it is time to look at a financing strategy that matches your ambition.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664

Are you ready to see if your property qualifies? Pre-qualify today and get the data you need to make your next move.