Michigan Real Estate: How DSCR Loans Simplify the Closing Process

Speed defines success in the Michigan real estate market. Whether you are eyeing a multi-unit in Grand Rapids or a single-family rental in the Detroit suburbs, the ability to move quickly determines whether you secure the deed or lose out to a cash buyer.

Traditional mortgage lending often feels like a marathon through a swamp of paperwork. Between tax returns, debt-to-income (DTI) ratios, and employment verification, the clock often runs out before the bank even issues an approval.

This is where the Debt Service Coverage Ratio (DSCR) loan changes the game for Michigan investors. By shifting the focus from your personal finances to the property’s income potential, the closing process becomes a streamlined, predictable path to ownership.

Understanding the DSCR Advantage

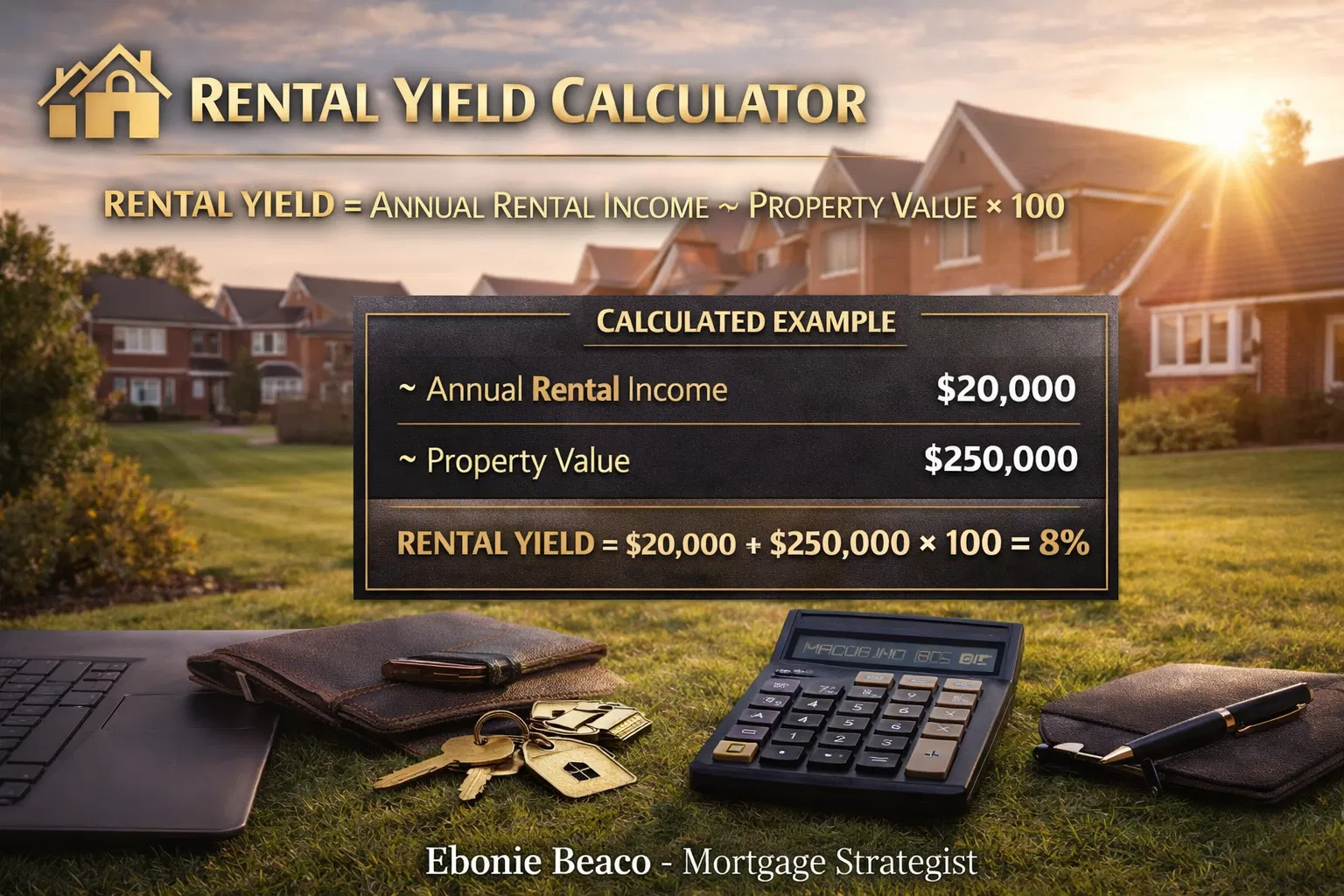

Debt Service Coverage Ratio (DSCR): A financial metric used by lenders to evaluate an investment property's ability to cover its mortgage payments through its own rental income.

This calculation allows a Michigan DSCR loan lender to bypass the typical scrutiny applied to a borrower's personal income. If the property pays for itself, the loan is viable.

A Michigan brick home with seasonal landscaping, representing a prime investment opportunity in a competitive neighborhood.

A Michigan brick home with seasonal landscaping, representing a prime investment opportunity in a competitive neighborhood.

Case Study: Beating a Cash Offer in Grand Rapids

Consider the case of an investor named Marcus. Marcus found a high-potential duplex in the East Hills neighborhood of Grand Rapids. The seller was motivated but had a strict requirement: the deal had to close in 14 days, or they would accept a lower, all-cash offer from a local hedge fund.

Marcus knew a traditional bank would take at least 45 to 60 days to verify his business tax returns and personal income. He turned to a DSCR strategy instead.

Because the property was already tenanted and generating $3,500 in monthly rent, and the projected mortgage payment was $2,800, the DSCR was 1.25. This exceeded the typical 1.20 requirement, allowing the underwriting team to focus solely on the property’s value and the title work.

Marcus closed in exactly 14 days. He secured the property without needing to liquidate his own cash reserves, effectively out-positioning a "cash is king" competitor through financing speed.

Why Traditional Banks Struggle with Investor Timelines

Traditional lenders are built for homeowners, not investors. They use a "Full Doc" approach that requires a deep dive into your financial history.

For a self-employed investor or someone with a complex portfolio, this process is grueling. The underwriter must calculate every source of income, subtract every liability, and verify every tax deduction.

In contrast, the DSCR process eliminates these hurdles. You can explore how this differs from other programs by viewing our complete mortgage service area map.

The No-Income-Verification Process Explained

The most significant time-saver in a DSCR loan is the removal of personal income verification. Here is what you generally do not need to provide:

- Tax Returns: No two-year history of IRS filings is required.

- W2s or Pay Stubs: Your employment status is irrelevant to the property's performance.

- DTI Ratios: Your personal debt (car loans, student loans) does not impact the loan's eligibility.

By removing these variables, the underwriting team can move from "Application" to "Clear to Close" in a fraction of the time.

Essential Documentation for a Fast Michigan Close

To hit a 14-to-21-day closing window, you must have your "investor kit" ready. A Michigan DSCR loan lender will typically request:

- Entity Documents: Most DSCR loans in Michigan require you to close in an LLC. Have your Articles of Organization and Operating Agreement ready.

- Lease Agreements: If the property is occupied, the current lease dictates the income.

- Appraisal with Rent Schedule: The appraiser must complete Form 1007 to verify market rents in the area.

- Proof of Down Payment: You still need to show you have the funds to close and required reserves.

Managing these documents effectively is the secret to choosing the ideal lender who understands the pace of investment real estate.

Navigating the Michigan LLC Requirement

In the state of Michigan, many DSCR programs require the borrower to be a legal entity rather than an individual. This provides a layer of liability protection for the investor and allows the lender to treat the transaction as a business-to-business loan.

If you haven't formed your LLC yet, do so before signing your purchase agreement. Closing in an LLC also makes it easier to manage capital gains taxes when it comes time to sell or trade the property.

Calculating Your Potential Speed: The Timeline

What does a 14-day close actually look like?

- Day 1-2: Application and initial document upload. Credit is pulled and the LLC is verified.

- Day 3-7: The appraisal is ordered and completed. This is the most critical step, as the appraiser must confirm both the value and the market rent.

- Day 8-10: Underwriting review. Since there is no income to verify, the underwriter focuses on the appraisal and title report.

- Day 11-12: Conditions are cleared. These are usually minor items like insurance binders or updated bank statements.

- Day 13: Clear to Close (CTC) issued. Closing disclosures are sent.

- Day 14: Signing and funding.

Compare this to the 50-year mortgage or other conventional products, and the efficiency of DSCR becomes undeniable.

Why Real Estate Investors Prefer DSCR

Investors use DSCR because it allows for scalability. When you aren't limited by your personal DTI, you can theoretically own an unlimited number of properties, provided each one "covers" its own debt.

This is especially useful for those following the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) method. Once a property is renovated and a tenant is placed, you can use a DSCR loan to cash-out refinance your initial capital and move to the next deal.

Common Hurdles to a Fast Close (and How to Avoid Them)

Even with a streamlined process, delays can happen. Awareness is your best defense.

- Appraisal Delays: In high-demand areas like Ann Arbor or Grand Rapids, appraisers are busy. Work with a lender who has a deep bench of local Michigan appraisers.

- Title Issues: Ensure the title company is experienced in investor transactions and LLC closings.

- Incomplete Insurance: Have your insurance agent ready to provide a quote for a landlord policy the moment you are under contract.

For more tips on avoiding common pitfalls, see our guide on expensive kitchen mistakes when preparing a property for the rental market.

Leveraging DSCR for Short-Term Rentals (Airbnb)

Michigan is a powerhouse for short-term rentals, particularly in coastal towns along Lake Michigan and near major universities. DSCR loans are often the only way to finance these properties effectively.

Standard lenders struggle to value the fluctuating income of an Airbnb. A specialized DSCR program can use "AirDNA" data or historical short-term rental income to qualify the loan, allowing you to close on a vacation rental with the same speed as a long-term lease property.

If you are looking to enter the short-term market, you may want to pre-qualify to see how your target property measures up.

Strategic Planning for Michigan Investors

The Michigan real estate landscape is shifting. As interest rates fluctuate, the ability to lock in a deal quickly becomes a massive financial advantage.

Waiting for a traditional bank to "bless" your personal income is no longer necessary. By utilizing the DSCR model, you treat your real estate portfolio like the business it is.

Jump in and analyze your next deal with the mindset of a professional. When you remove the personal paperwork, you gain the clarity needed to scale.

Take the Next Step in Your Investment Journey

Navigating the nuances of the Michigan market requires a partner who understands that time is your most valuable asset. Whether you are looking for a Michigan DSCR loan lender to help you beat a cash offer or you want to explore cash-out options for your current portfolio, expert guidance is just a call away.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664