How Atlanta Real Estate Investors Are Winning with Low-DSCR Loans

The Atlanta real estate market is currently moving at a pace that demands agility and a different kind of financial playbook. If you are an investor looking at properties along the BeltLine or in rapidly gentrifying pockets of the city, you have likely noticed that traditional financing can sometimes feel like a bottleneck. This is where the Debt Service Coverage Ratio (DSCR) loan becomes a vital tool in your belt.

While many investors aim for high cash flow from day one, a growing number of savvy Atlanta professionals are winning by leveraging "Low-DSCR" loans. These are loans where the property’s rental income essentially breaks even with the mortgage payment: a 1.0 ratio. You might wonder why anyone would settle for a breakeven property. In a city like Atlanta, the answer is often tied to appreciation and long-term portfolio scaling.

Defining the DSCR Loan

A DSCR loan is a type of non-QM (Non-Qualified Mortgage) loan that allows you to qualify based on the income generated by the property rather than your personal income or tax returns.

DSCR (Debt Service Coverage Ratio): A financial metric used to measure a property's ability to cover its debt obligations. Practical Application: Lenders divide the monthly gross rent by the monthly debt service (principal, interest, taxes, insurance, and HOA) to determine the ratio.

For example, if a property in West End rents for $2,500 and the total mortgage payment is $2,500, your DSCR is 1.0. If the rent is $3,000 and the payment is $2,400, your DSCR is 1.25.

The Strategy Behind the 1.0 Ratio

In many traditional lending circles, a 1.25 ratio is the gold standard. However, an Atlanta DSCR loan lender understands that the city's market dynamics often favor future value over immediate monthly profit.

Explore the idea of the "Breakeven Winner." When you acquire a property with a 1.0 DSCR, you are essentially asking the tenant to pay off your mortgage while you wait for the neighborhood to appreciate. In Atlanta’s high-growth corridors, the equity gain can far outpace the value of a few hundred dollars in monthly cash flow.

Jump in and look at the market activity. If you are feeling like the housing market is confusing, you aren't alone. But for investors, the focus remains on the asset's performance rather than the noise.

Why Atlanta Investors Choose Low-DSCR Loans

Atlanta is a unique beast. We have a massive tech presence, a thriving film industry, and a constant influx of new residents. This leads to several reasons why a low-DSCR loan makes sense:

- Neighborhood Transformation: Areas that were overlooked five years ago are now the most sought-after zip codes. Getting into these areas early often means accepting lower initial rents compared to high mortgage costs.

- Ease of Qualification: Since these loans do not look at your personal Debt-to-Income (DTI) ratio, you can scale your portfolio quickly. You aren't limited by how many conventional loans you can carry.

- LLC Friendly: You can close the loan in the name of your LLC, providing a layer of asset protection that traditional residential loans often lack.

- No Tax Returns Needed: This is a major benefit for self-employed investors or those who have significant write-offs on their tax returns.

Case Study: The Long-Term Play in a Gentrifying Neighborhood

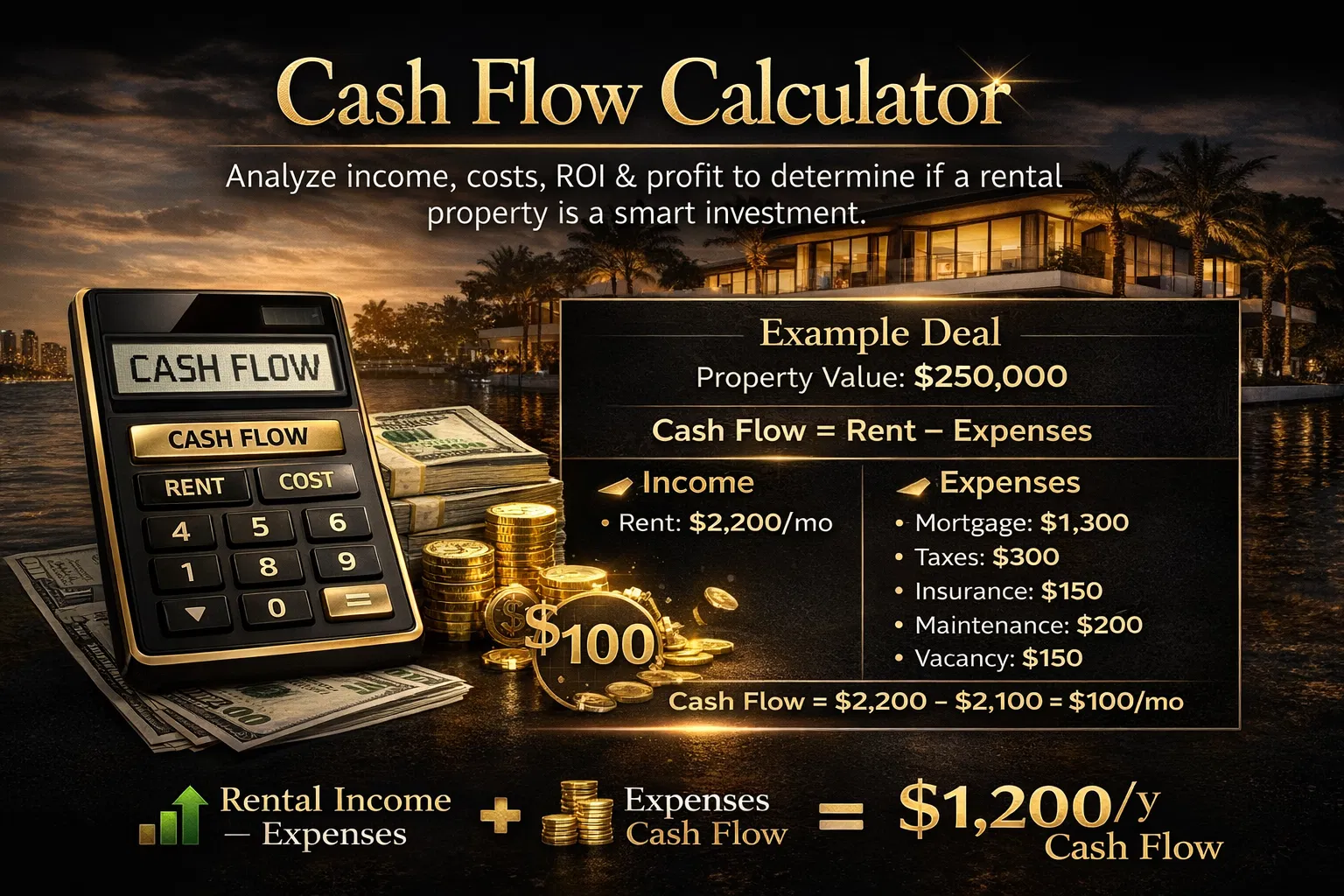

Let’s look at a real-world scenario involving an investor named Marcus. Marcus found a charming bungalow in an area of Atlanta undergoing significant revitalization. The property was priced at $400,000.

The Financial Breakdown:

- Purchase Price: $400,000

- Down Payment (20%): $80,000

- Loan Amount: $320,000

- Total Monthly Payment (PITI): $2,600

- Projected Monthly Rent: $2,600

- DSCR Ratio: 1.0

At first glance, some might say Marcus is "breaking even." However, Marcus is an experienced investor who recognizes that this specific pocket of Atlanta has seen a 7% annual appreciation rate over the last three years.

By using a low-DSCR loan, Marcus secured the property without needing to show his personal income. Within 12 months, the property value rose to $428,000. While his cash flow was $0, his wealth increased by $28,000 in equity, plus the principal paydown contributed by the tenant.

Marcus also kept an eye on interest rates. He knew that if interest rates are dropping, he could potentially refinance later to improve his ratio and start seeing positive cash flow.

How to Qualify with an Atlanta DSCR Loan Lender

Qualifying for a low-DSCR loan is a different experience than applying for a standard home loan. The focus shifts from "How much do you make?" to "How much does the house make?"

Access the basic requirements typically expected by lenders:

- Credit Score: Most programs prefer a score of 620 or higher, though higher scores often unlock better rates.

- Appraisal with Rent Schedule: The lender will order an appraisal that includes a Form 1007, which confirms the market rent for the property.

- Liquidity Reserves: Lenders usually want to see that you have 3 to 6 months of mortgage payments set aside in a bank account.

- Property Type: These loans are designed for non-owner-occupied investment properties, including single-family homes, townhomes, and 2-4 unit small multifamily buildings.

Scaling Your Portfolio with Zero DTI Stress

One of the biggest hurdles for real estate investors is the "DTI ceiling." Once you own three or four properties under conventional financing, your personal debt-to-income ratio often becomes too high to qualify for more.

Compare this to the DSCR model. Because the lender ignores your personal income, you could theoretically own 10, 20, or 50 properties as long as each one meets the minimum DSCR requirements. This is how professional investors in Georgia and Florida are building massive portfolios in record time.

If you are ready to see what your numbers look like, you can pre-qualify to get a clear picture of your purchasing power.

Common Misconceptions About Low-DSCR Loans

"The Interest Rates are Too High" While it is true that DSCR loans carry slightly higher interest rates than conventional owner-occupied loans, you must weigh the cost against the benefit. The "cost" is the interest rate; the "benefit" is the ability to acquire an asset that you otherwise couldn't finance.

"I Can't Get a Loan if the Property Doesn't Cash Flow" This is a common myth. While some lenders require a 1.2 ratio, many specialized programs allow for a 1.0 ratio or even a "No Ratio" option if your credit score and down payment are strong enough. This is specifically useful for properties in high-appreciation areas where rents haven't quite caught up to property values yet.

"The Process Takes Too Long" Actually, DSCR loans often close faster than conventional loans. Because there is no need to verify employment, income history, or tax transcripts, the underwriting process is streamlined.

Structuring Your Next Atlanta Deal

When you are looking at your next investment in the Atlanta metro area, don't just look at the monthly check you'll receive. Look at the total return on investment.

Consider the "Wealth Trifecta":

- Appreciation: The increase in the property's market value over time.

- Amortization: The tenant paying down your loan balance every month.

- Tax Benefits: Depreciation and interest deductions that can offset your other income.

Even at a 1.0 DSCR, you are hitting all three of these wealth-building pillars. If you find a property in a "path of progress" neighborhood, the low-DSCR loan is your ticket to entry.

Next Steps for Investors and Realtors

For realtors, understanding these programs is a game-changer for your clients. When a buyer says, "I don't think I can qualify because I'm self-employed," you can point them toward a DSCR solution. It keeps the deal alive and helps your clients build long-term wealth.

For investors, the key is to stop waiting for the "perfect" 1.5 DSCR deal that might never come in a competitive market. Instead, look for the solid 1.0 deal in a location that is poised for growth.

Explore your options. Compare the numbers. And most importantly, have a strategist in your corner who knows the Atlanta landscape.

Ready to see how a DSCR loan can fit into your investment strategy?

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664