Most Homeowners Don’t Realize Their House Could Be a $200,000 Credit Line. Here’s How a HELOC Works

For many homeowners, their house is more than a place to live. It is often their largest financial asset. As property values rise and mortgage balances decrease, homeowners build equity in their homes. What many people do not realize is that this equity can potentially be turned into a large credit line through a Home Equity Line of Credit, commonly known as a HELOC.

A HELOC allows homeowners to borrow against the equity they have built in their property while still maintaining ownership of the home. In many cases, homeowners could have access to $100,000, $150,000, or even $200,000 depending on the value of the property and the remaining mortgage balance.

What Is a HELOC

A Home Equity Line of Credit works similarly to a credit card, but it is secured by your home. Instead of receiving a lump sum loan, borrowers are approved for a maximum credit limit that they can access when needed.

Common HELOC features include:

• A revolving line of credit secured by your home

• A draw period that often lasts 10 years

• A repayment period that can last 15 to 20 years

• Interest charged only on the amount that is used

• Flexible access to funds for different financial needs

Because the loan is secured by real estate, HELOC interest rates are often lower than personal loans and credit cards.

How Lenders Calculate Your Available HELOC

The amount a homeowner can borrow depends on several factors. Lenders evaluate the property value, mortgage balance, credit score, and debt to income ratio. Most lenders allow homeowners to borrow up to 80 percent to 90 percent of the home's value when combining the first mortgage and the HELOC.

The available credit line is typically calculated using the following factors:

• Current market value of the home

• Remaining mortgage balance

• Maximum combined loan to value ratio allowed by the lender

• Borrower credit profile and financial stability

The difference between the lender's maximum allowed loan amount and the remaining mortgage balance determines the available HELOC credit line.

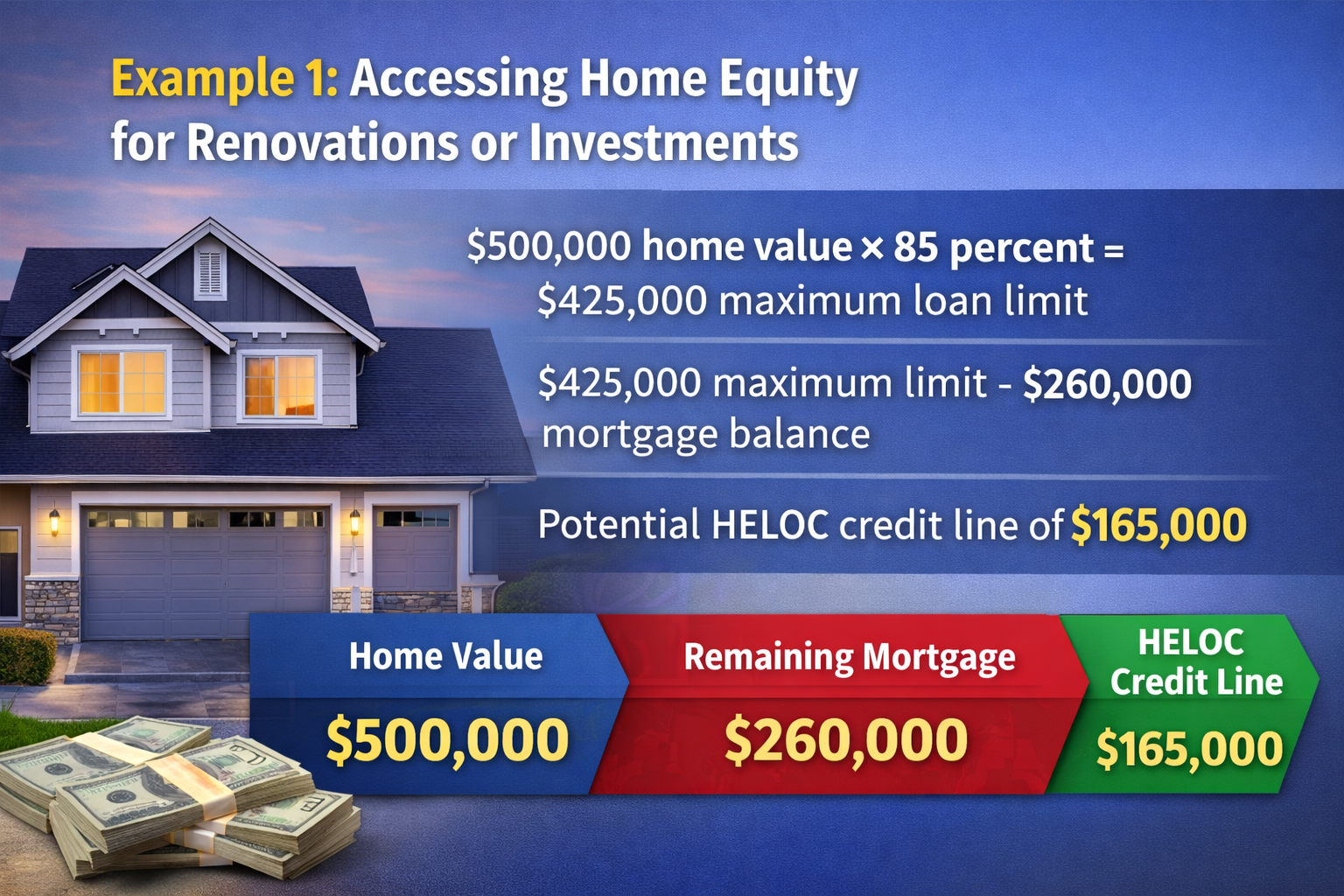

Example 1: Accessing Home Equity for Renovations or Investments

Consider a homeowner whose property is valued at $500,000. Their remaining mortgage balance is $260,000. If a lender allows an 85 percent combined loan to value ratio, the maximum total borrowing amount would be $425,000.

Calculation:

• $500,000 home value × 85 percent = $425,000 maximum loan limit

• $425,000 maximum limit − $260,000 mortgage balance

• Potential HELOC credit line of $165,000

This homeowner could potentially access up to $165,000 through a HELOC. Many homeowners use this type of credit line to finance renovations, consolidate debt, or invest in additional real estate.

Example 2: Using Home Equity as an Investment Tool

Now consider a homeowner with a property valued at $620,000 and a remaining mortgage balance of $340,000. If the lender allows an 85 percent combined loan to value ratio, the maximum borrowing amount would be $527,000.

Calculation:

• $620,000 home value × 85 percent = $527,000 maximum loan limit

• $527,000 maximum limit − $340,000 mortgage balance

• Potential HELOC credit line of approximately $187,000

This homeowner could potentially access close to $187,000 in available credit. Real estate investors often use HELOC funds to finance property renovations, fund down payments on rental properties, or create liquidity for investment opportunities.

Why Many Homeowners Use HELOCs

A HELOC can be a powerful financial strategy when used responsibly. It allows homeowners to leverage the value of their property while maintaining flexibility over when funds are used.

Some of the most common reasons homeowners open a HELOC include:

• Home renovations and property improvements

• Real estate investing and rental property purchases

• Debt consolidation with lower interest rates

• Emergency financial reserves

• Business or investment opportunities

For homeowners who have built significant equity, a HELOC can create financial flexibility and access to capital without selling their property.

If you are a homeowner or real estate investor and want to understand how much equity you may be able to access, you can schedule a complimentary one on one consultation to review your financing options.

Schedule here:

https://calendly.com/homeloansnetwork

You can also listen to more real estate financing insights on The Real Estate Deal Room Podcast by Ebonie Beaco, where mortgage strategies, investor financing, and market insights are discussed in depth.