Arkansas Investment Properties: Breaking Down DSCR Loan Requirements

Arkansas has quickly become a standout destination for real estate investors. With its blend of affordable entry prices and a steady demand for rental housing in cities like Little Rock, Fayetteville, and Bentonville, the "Natural State" offers a unique landscape for building wealth. However, if you are a 1099 worker, a freelancer, or an entrepreneur, traditional financing can often feel like a brick wall.

The traditional mortgage world relies heavily on tax returns and debt-to-income (DTI) ratios. For many successful investors, those tax returns show heavy deductions that, while great for the IRS, make it difficult to qualify for a standard loan. This is where the Debt Service Coverage Ratio (DSCR) loan steps in.

As an Arkansas DSCR loan lender, we focus on the property’s ability to generate income rather than your personal pay stubs. If the rent covers the mortgage, you are halfway to the finish line.

Understanding the Core of DSCR Financing

A DSCR Loan is a non-QM (Non-Qualified Mortgage) loan designed specifically for investment properties. Instead of looking at your personal income, lenders look at the cash flow of the property you are buying or refinancing.

Debt Service Coverage Ratio (DSCR): A financial metric used to evaluate a property's ability to cover its debt obligations. Practical Application: It allows you to scale a portfolio without hitting the personal income limits that stop most traditional borrowers.

Arkansas investment property nestled in natural woods landscaping, representing the serene yet profitable opportunities in the local market.

Arkansas investment property nestled in natural woods landscaping, representing the serene yet profitable opportunities in the local market.

How the Calculation Works in the Real World

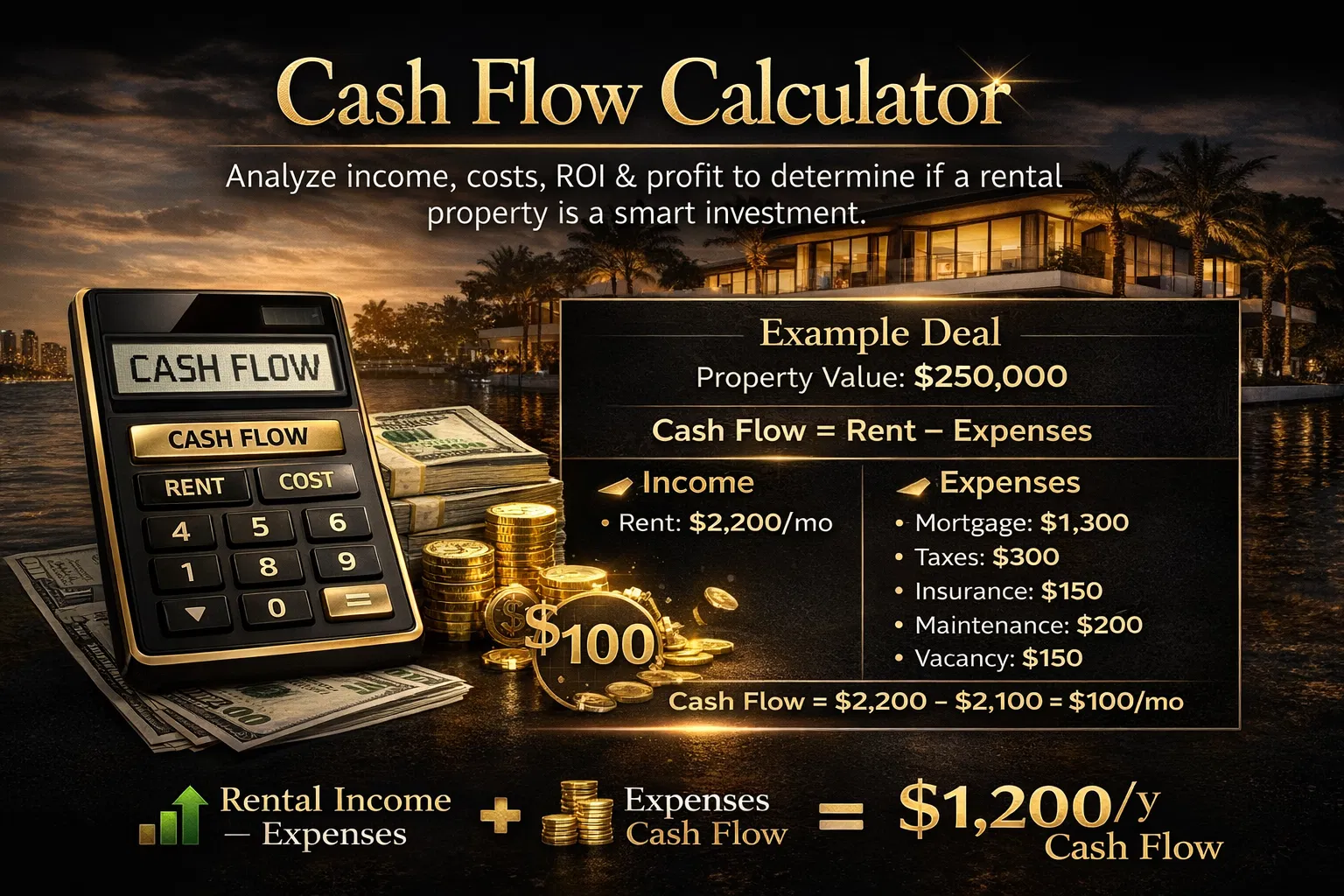

To understand if a deal works, you have to know the math. The DSCR is calculated by taking the Gross Monthly Rent and dividing it by the PITI (Principal, Interest, Taxes, and Insurance), plus any HOA fees.

For example, if a duplex in Little Rock brings in $2,000 in total rent and the total mortgage payment is $1,600, your ratio is 1.25.

Most lenders look for a ratio of 1.0 or higher. A 1.0 means the property "breaks even." Anything above 1.0 is considered positive cash flow. Some programs even allow for "no-ratio" or "low-ratio" loans (under 1.0) if you have a strong credit profile or significant cash reserves, though these typically come with higher interest rates.

Case Study: Marcus, the 1099 Investor in Little Rock

Marcus is a freelance consultant in Little Rock. He earns $120,000 a year, but after his business expenses and tax write-offs, his "taxable income" looks much lower to a traditional bank. Marcus found a charming craftsman-style home near the downtown area that he wanted to turn into a long-term rental.

When Marcus approached a traditional lender, they denied him. His DTI was too high because they couldn't count his full gross income.

The DSCR Strategy: Marcus shifted his focus to a DSCR loan.

- Property Price: $225,000

- Expected Rent: $1,900

- Estimated PITI: $1,550

- DSCR Ratio: 1.22

Because the property generated more than enough rent to cover the debt, Marcus qualified easily. He didn't have to provide a single tax return or W-2. He used his 20% down payment and closed the deal in three weeks.

Credit Score vs. DSCR Ratio: Which Holds More Weight?

In the world of Arkansas investment properties, your credit score and the property's DSCR ratio work together like a scale. Neither one is the sole factor, but they both influence your terms.

1. The Credit Score Requirement

While we don't look at your income, we do look at how you handle debt. Most DSCR programs require a minimum credit score of 620 to 640.

- Higher Scores (720+): Typically unlock the lowest interest rates and the highest Loan-to-Value (LTV) options (up to 80%).

- Lower Scores (620-660): May require a larger down payment (25-30%) to offset the risk.

2. The DSCR Ratio Requirement

The ratio determines the "strength" of the deal.

- 1.25 or Higher: This is the "sweet spot." It shows the property is highly profitable.

- 1.0 to 1.24: Very standard and easily fundable for most investors.

- Less than 1.0: This indicates the property is "short" on cash flow. You can still get funded, but expect to bring more cash to the table as a down payment.

Compare: If you have a 760 credit score but the property has a 0.9 DSCR, you might still get a great rate but have to put 30% down. Conversely, if you have a 640 credit score but the property has a 1.5 DSCR, the strength of the property helps balance your lower credit profile.

Why Arkansas Investors Are Choosing DSCR Loans

Arkansas offers a diverse mix of investment opportunities, from the bustling corporate hubs in the Northwest to the steady, reliable rental markets in central Arkansas. Here is why the DSCR model fits this state so well:

- Speed of Execution: In a competitive market like Fayetteville, being able to close quickly is vital. DSCR loans typically close faster than conventional loans because there is no income verification.

- LLC Ownership: Most DSCR lenders actually prefer that you close in the name of an LLC. This provides a layer of asset protection that traditional residential loans often discourage.

- No Limit on Properties: Conventional financing often caps you at 10 properties. With DSCR, you can theoretically own 50 or 100 properties, provided each one meets the ratio requirements.

- Short-Term Rental Friendly: Arkansas is a tourist destination. From the Ozarks to Hot Springs, Airbnb and VRBO properties are booming. We can often use "AirDNA" data or short-term rental projections to qualify the loan.

The Down Payment and Reserve Requirements

Because these are considered higher-risk than a primary residence, you should plan for the following:

- Down Payment: Usually 20% to 25%. Some specialized programs might allow 15% for highly experienced investors, but 20% is the standard.

- Cash Reserves: Lenders want to see that you have enough cash in the bank to cover 3 to 6 months of mortgage payments (PITI). This ensures that if the property sits vacant for a month or needs a repair, you won't default.

Navigating the Appraisal Process

The appraisal for a DSCR loan is slightly different than a standard home appraisal. The appraiser will complete a Form 1007 (Single-Family Rent Schedule). This document tells the lender what the fair market rent is for that specific property based on comparable rentals in the area.

If the appraiser says the market rent is $1,500, but you were hoping for $1,800, the loan will be based on the $1,500 figure unless you have a signed lease in place that proves otherwise.

Getting Started in the Arkansas Market

If you are looking to expand your portfolio, the first step is a pre-qualification. This isn't the scary, document-heavy process you might be used to. We will look at your credit score, the estimated value of the property you are targeting, and the projected rent.

Explore your options by looking at different property types. Whether it is a single-family home in the suburbs of Little Rock or a small multi-family unit in Jonesboro, the DSCR program is versatile enough to handle it.

Access the equity you already have. If you own properties with significant equity, you can use a cash-out refinance to pull funds out and use them as a down payment for your next Arkansas investment.

Final Thoughts for Realtors and Investors

For realtors, understanding DSCR is a game-changer for your 1099 and investor clients. When a client tells you they can't get a loan because of their tax returns, you can steer them toward a strategy that focuses on the deal itself.

The Arkansas market continues to grow, and the natural beauty of the state keeps demand high. From the woods of the Ozarks to the metro centers, the opportunities are there if you have the right financing partner.

Jump in and evaluate your next deal today. If the numbers work, the loan works.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

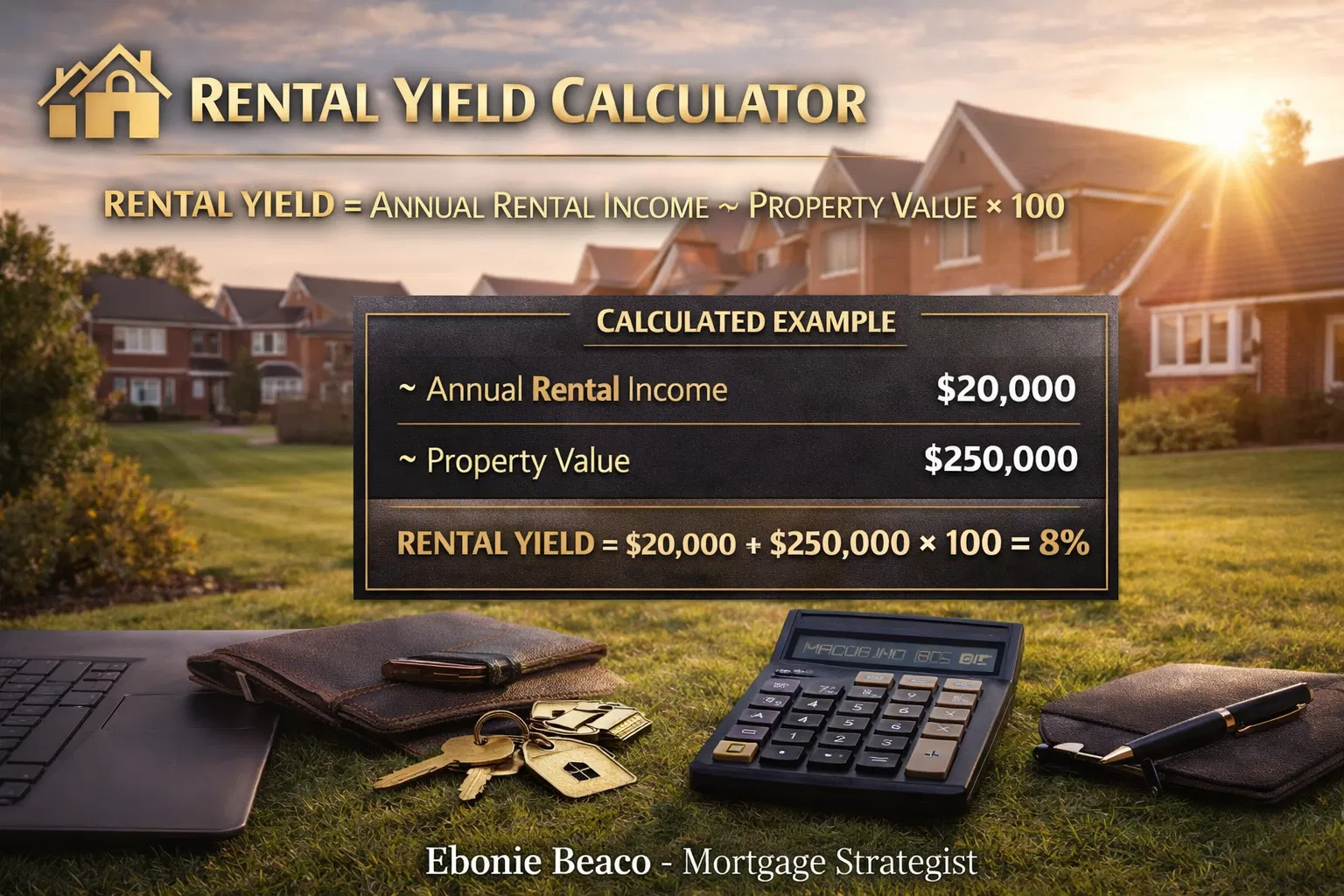

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664