Alabama Real Estate Investing: Cash Flow Calculations for DSCR Success

Alabama has emerged as a powerhouse for real estate investors seeking high yields and steady growth. While markets like Florida and California often grab the headlines, savvy investors are looking toward the "Magic City" of Birmingham and surrounding areas for consistent cash flow. To succeed in this market, you need to understand the primary tool used by professional landlords: the DSCR loan.

As an Alabama DSCR loan lender, I focus on the performance of the property rather than your personal debt to income ratio. This shift in perspective allows you to scale your portfolio much faster than traditional financing would ever permit. But to make this strategy work, you must master the art of the cash flow calculation.

What is a DSCR Loan?

Debt Service Coverage Ratio (DSCR): A financial metric used by lenders to measure a property's ability to cover its debt obligations using only its rental income.

In plain English, a DSCR loan evaluates whether the rent coming in is enough to pay the mortgage going out. If the property pays for itself, the lender is satisfied. This is a game changer for investors who may have high personal expenses or multiple existing mortgages that make qualifying for a standard bank loan difficult.

Explore how these loans work by looking at the property's potential rather than your tax returns. You can pre-qualify for these programs based on the asset's performance.

Why Birmingham is a DSCR Hotspot

Birmingham offers a unique combination of affordable entry points and strong rental demand. With a diverse economy rooted in healthcare, finance, and education, the rental market stays robust even when the national economy fluctuates.

When you analyze a deal in Birmingham, you often find properties where the rental income significantly exceeds the monthly debt service. This "buffer" is exactly what a DSCR loan looks for. Alabama also benefits from some of the lowest property taxes in the United States, which directly improves your cash flow and your DSCR ratio.

(A beautiful Alabama southern-style home with a lush garden and wrap-around porch, representing the high-quality rental stock found in the Birmingham suburbs.)

(A beautiful Alabama southern-style home with a lush garden and wrap-around porch, representing the high-quality rental stock found in the Birmingham suburbs.)

The DSCR Calculation Formula

To calculate your ratio, you use a simple formula:

Gross Monthly Rent / PITIA = DSCR

PITIA stands for:

- Principal

- Interest

- Taxes

- Insurance

- Association Dues (HOA)

If your gross rent is $1,500 and your total PITIA is $1,200, your DSCR is 1.25.

Most lenders look for a ratio of 1.0 or higher. A 1.0 means the property "breaks even." A ratio of 1.25 or higher is considered a "strong" cash flow and often unlocks the best interest rates and terms.

Case Study: The Birmingham High-Yield Market

Let's look at a real-world scenario for a single-family home in a growing Birmingham neighborhood.

The Scenario:

- Purchase Price: $200,000

- Down Payment: $40,000 (20%)

- Loan Amount: $160,000

- Interest Rate: 7.0%

- Monthly Rent: $1,850

The Expenses (Monthly):

- Principal & Interest: $1,064

- Property Taxes (Alabama average): $100

- Homeowners Insurance: $110

- HOA Dues: $0

- Total PITIA: $1,274

The Calculation: $1,850 (Rent) / $1,274 (PITIA) = 1.45 DSCR

In this case, the property generates 45% more income than the debt service requires. This is an excellent result for an investor. An Alabama DSCR loan lender would see this as a low-risk, high-reward investment, likely offering competitive terms because the "coverage" is so high.

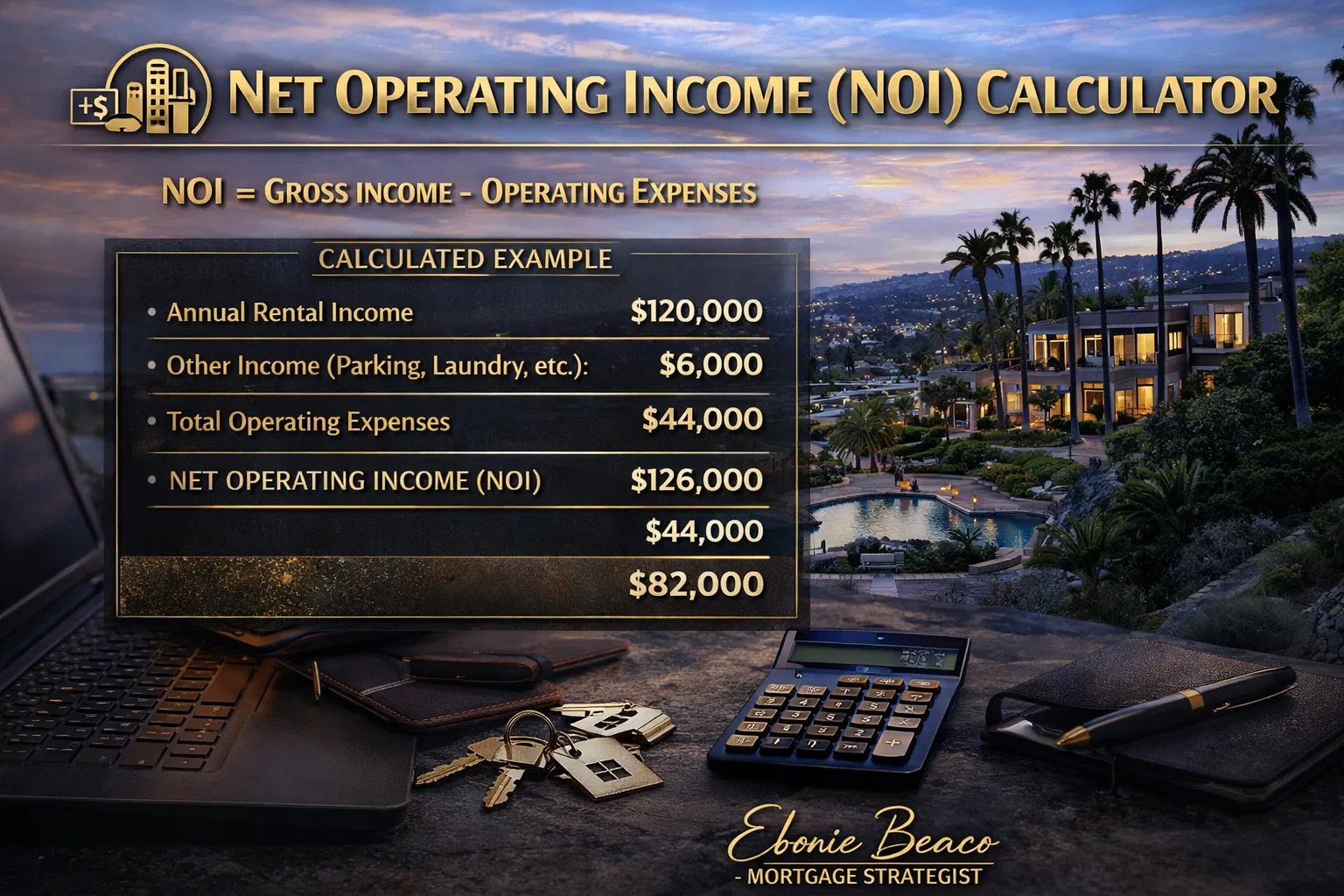

Net Operating Income (NOI) vs. Mortgage Payment

While lenders focus on PITIA, as an investor, you need to look at the Net Operating Income (NOI).

Net Operating Income (NOI): The total income generated by a property after all operating expenses have been paid, but before mortgage payments or taxes are deducted.

Operating expenses include repairs, property management fees, and vacancies. While the lender doesn't always subtract these from the DSCR calculation, you must account for them to ensure you are actually making a profit.

If your Birmingham rental has an NOI of $1,600 and your mortgage payment (Principal and Interest) is $1,064, your actual "cash-in-hand" is $536 per month. Understanding this difference helps you avoid "paper profits" that disappear when a water heater breaks or a tenant moves out.

The Impact of Property Taxes on Your DSCR

One reason Alabama is so attractive for DSCR loans is the tax environment. Compare a $300,000 home in Birmingham to a $300,000 home in Chicago or New Jersey. The property taxes in Alabama might be $1,500 per year, while in other states, they could easily be $6,000 or more.

Since taxes are part of the "PITIA" denominator in the DSCR formula, lower taxes mean a lower denominator and a much higher ratio. This allows you to qualify for larger loans on Alabama properties than you might elsewhere.

Jump in and compare how interest rates impact your loans to see how small shifts in the market can change your monthly cash flow.

Strategies to Improve Your DSCR

If you find a property in Alabama that you love but the DSCR is coming in too low (below 1.0), you have several options to fix the deal:

- Increase the Down Payment: By lowering the loan amount, you lower the monthly interest and principal payments, which increases your ratio.

- Buy Down the Interest Rate: Paying points upfront can lower your monthly payment for the life of the loan.

- Validate Market Rents: Lenders use an appraisal (Form 1007) to determine market rent. If you can provide evidence that the home can rent for more (perhaps as a short-term rental), the lender may use that higher figure.

- Shop Insurance: Don't settle for the first insurance quote. In Alabama, wind and hail coverage can vary significantly. A lower insurance premium improves your DSCR.

For investors looking at more complex deals, such as those involving renovations, you might consider fix and flip loans before transitioning into a long-term DSCR loan once the property is stabilized and rented.

Scaling Your Alabama Portfolio

The beauty of working with a dedicated Alabama DSCR loan lender is the ability to repeat this process. Because these loans do not appear on your personal debt-to-income (DTI) profile in the same way a traditional mortgage does, you aren't capped by your salary.

As long as the property's income supports the debt, you can continue to acquire assets. Many investors use a cash-out refinance strategy on their existing properties to fund the down payment on the next Alabama rental.

Working with Realtors and Investors

Realtors in Alabama can use DSCR knowledge to help their clients close more deals. When a client is frustrated by strict traditional banking rules, introducing them to a DSCR specialist can save the transaction.

By focusing on properties with high rental yields in areas like Birmingham, Huntsville, or Mobile, realtors can present "ready-made" investment opportunities where the math already works for a DSCR loan. This makes the property much more attractive to out-of-state investors who are looking for turnkey cash flow.

Final Thoughts on Alabama Cash Flow

Success in Alabama real estate isn't about luck; it is about the math. By focusing on the DSCR and understanding how NOI interacts with your debt service, you can build a resilient portfolio that withstands market cycles.

Whether you are looking at a single-family home in Birmingham or a multi-unit property in Montgomery, the principles remain the same. Keep your expenses low, your rents competitive, and your financing strategic.

Access the tools you need to analyze your next deal and see how the numbers stack up. If you're ready to explore how a DSCR loan can fit into your investment strategy, let's look at your specific scenario.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664