7 Mistakes You're Making with Your Florida HELOC (and How to Fix Them Before Breakfast)

You just poured your first cup of coffee, the Florida sun is hitting the patio, and you’re thinking about that equity sitting in your home. Whether you are in Miami, Tampa, or even looking at properties across the country in California or Georgia, your home equity is likely your largest untapped asset.

A Home Equity Line of Credit (HELOC) is a powerful tool, but it is also one of the most misunderstood financial products in the mortgage industry. If you are not careful, a Florida HELOC can turn from a wealth-building tool into a financial anchor.

Here are the seven mistakes homeowners and investors are making right now and how you can course-correct before your second cup of coffee is cold.

1. The Secret Home Equity Drain: The Velocity Banking Trap

Velocity Banking: A strategy where a homeowner uses a HELOC as their primary checking account to pay off their main mortgage quickly. Practical Application: While it sounds efficient, it often shifts low-interest fixed debt to higher-interest variable debt.

The mistake here is thinking you are "beating the system." Many homeowners in high-growth areas like Virginia or Michigan attempt to funnel their entire paycheck into a HELOC to lower the daily average balance. While this reduces interest on paper, you are effectively trading a 3% or 4% fixed-rate primary mortgage for a variable rate that could be significantly higher.

The Fix: Compare the total interest cost over the life of both loans. If your primary mortgage has a record-low rate, keep it. Use the HELOC for targeted investments, such as fix and flip financing or property improvements, rather than trying to outsmart your primary amortization schedule. You can compare options using our mortgage calculators to see the real numbers.

2. The 10-Year Payment Shock: The Interest-Only Fake Out

Draw Period: The initial phase of a HELOC (usually 10 years) during which you can borrow funds and typically only pay interest. Practical Application: This allows for lower monthly payments early on, but requires a plan for when the principal repayment kicks in.

Many California HELOC holders or investors in Illinois get comfortable making interest-only payments. It feels like "free money" because the monthly obligation is so low. However, once that draw period ends, the loan enters the repayment period. Suddenly, your payment could triple as you begin paying down the principal over a shorter 15 or 20-year window.

The Fix: Treat your HELOC like a standard loan from day one. Calculate what the principal and interest payment would be and pay that amount voluntarily. This builds equity faster and prevents the "payment shock" that leads many to a foreclosure situation.

Visual: A chart showing the difference between Interest-Only payments vs. Principal + Interest payments over 10 years.

Visual: A chart showing the difference between Interest-Only payments vs. Principal + Interest payments over 10 years.

3. The Vanishing Payment: Misapplied Principal Payments

This is a technical glitch that happens more often than you think. When you send extra money to a traditional mortgage, it is usually easy to tag it as "Principal Only." With a HELOC, lenders often apply overages to the next month's interest rather than the current principal balance.

The Fix: Review your statements monthly. If you are in Alabama or Missouri and notice your balance isn't dropping as fast as your extra payments suggest, call your servicer. Explicitly request that all overages be applied to the principal. Access your online portal and look for a specific toggle or checkbox for "Principal Reduction."

4. The Revolving Door: Consolidating Debt Without Strategy

Debt Consolidation: Using a lower-interest loan to pay off multiple high-interest debts. Practical Application: This reduces monthly outflows but only works if the source of the debt is addressed.

Homeowners from Indiana to Kentucky often use a HELOC to wipe out high-interest credit card debt. This is a smart move for your credit score, but it is dangerous for your home. If you clear the cards and then run the balances back up, you have doubled your debt and secured it against your roof.

The Fix: Before you draw funds for consolidation, close the high-interest accounts or cut up the cards. Your HELOC should be a bridge to financial freedom, not a safety net for overspending. Review our mortgage basics on credit to understand how this impacts your long-term borrowing power.

5. The Illusion of Wealth: Treating Equity Like Income

In a hot market like Florida or Georgia, equity grows fast. It is tempting to look at a $100,000 credit line as a $100,000 bonus. But equity is not income; it is a secured loan. Every dollar you draw is a dollar plus interest that must be repaid.

The Fix: Only draw from your HELOC for "appreciating" or "income-producing" purposes. Using it for a vacation is a mistake. Using it for a DSCR investor loan down payment on a rental property in Arkansas or Michigan is a strategy.

Visual: Infographic showing "Good Debt" (Home improvements, education, real estate investment) vs. "Bad Debt" (Luxury items, vacations, depreciating assets).

Visual: Infographic showing "Good Debt" (Home improvements, education, real estate investment) vs. "Bad Debt" (Luxury items, vacations, depreciating assets).

6. The High-Stakes Gamble: Funding Speculative Investments

DSCR Loan (Debt Service Coverage Ratio): A loan for real estate investors that qualifies based on the property’s income rather than the borrower’s personal income. Practical Application: Using a HELOC for a down payment on a DSCR property can help scale a portfolio quickly.

Some investors use a California HELOC to fund high-risk, speculative crypto ventures or unproven startups. If those investments fail, you have no way to pay back the HELOC, and the lender can take your primary residence.

The Fix: If you are an investor, use your HELOC as "gap funding" or for bridge loans. For example, use your equity to purchase a distressed property in Virginia, renovate it, and then refinance into a long-term loan to pay back the HELOC. This keeps your home safe while your investment grows.

7. The Regional Blindspot: Ignoring Local Market Dynamics

A Florida HELOC is different from a Georgia HELOC lender's requirements. LTV (Loan-to-Value) limits vary by state and by lender. Some lenders may only go up to 80% LTV in certain Florida counties due to insurance risks, while they might allow 90% in Illinois.

LTV (Loan-to-Value): The percentage of the property's value that is borrowed. Practical Application: Lower LTVs often result in better interest rates and easier approvals.

The Fix: Work with a Mortgage Strategist who understands the specific geographic nuances. Whether you are looking at Airbnb and short-term rental financing in coastal Florida or a suburban rental in Michigan, your strategy must match the local appraisal environment. You can learn more about appraisals here.

Calculating Your Real Borrowing Power

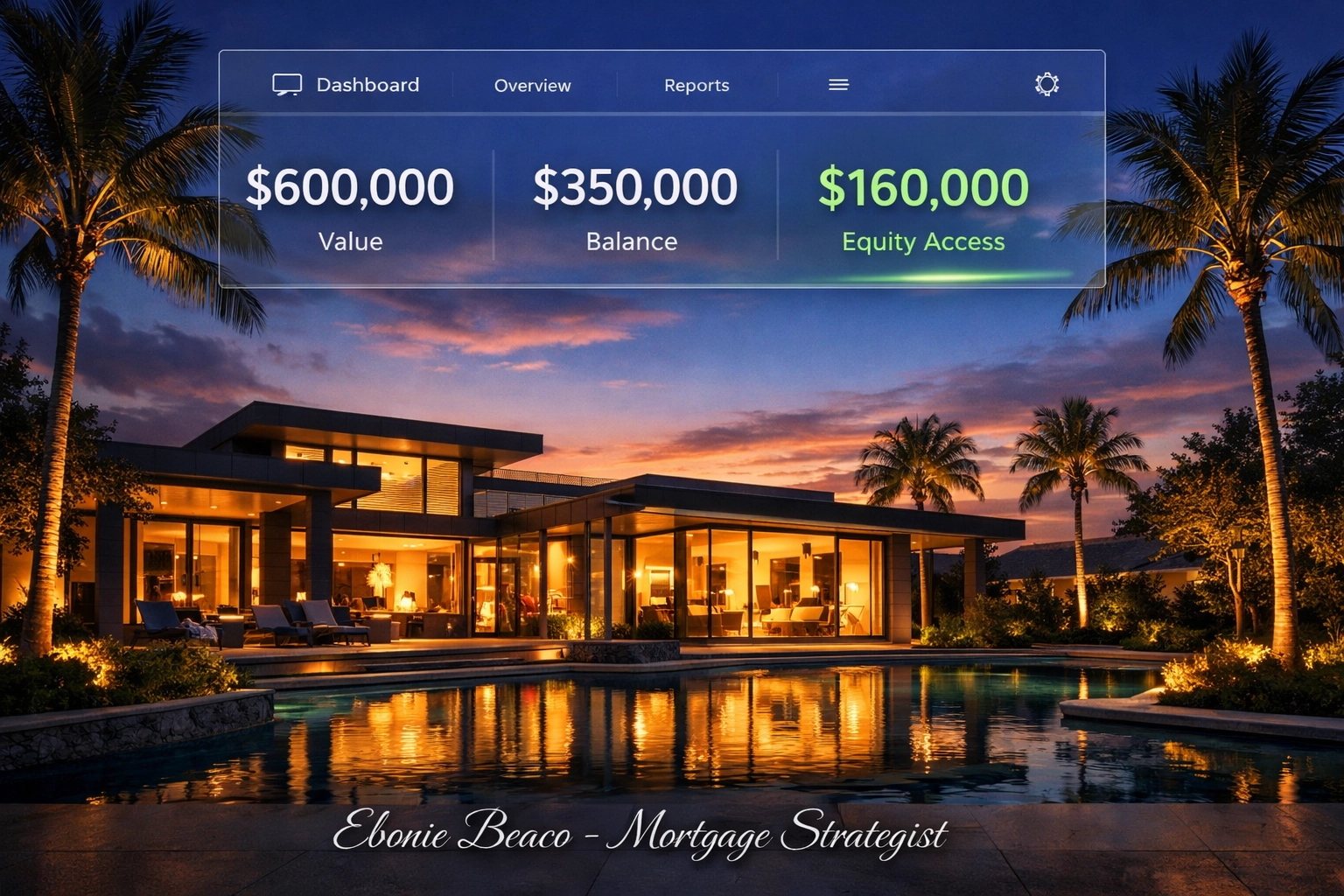

Let’s look at a real-world scenario. Suppose you own a home in Florida valued at $600,000. Your current mortgage balance is $350,000. Most lenders will allow a combined loan-to-value (CLTV) of 85%.

The Calculation:

- Home Value: $600,000

- Max CLTV (85%): $600,000 x 0.85 = $510,000

- Subtract Existing Mortgage: $510,000 - $350,000 = $160,000

- Available HELOC: $160,000

In this case, you have $160,000 in available credit. An investor could use this to fund the down payments for two DSCR rental property loans in Alabama, effectively turning one home into three income-producing assets.

Visual: A breakdown of the $600,000 home example showing the $160,000 HELOC availability and how it can be split into two $80,000 down payments.

Visual: A breakdown of the $600,000 home example showing the $160,000 HELOC availability and how it can be split into two $80,000 down payments.

Ready to Build a Smarter Strategy?

Managing a HELOC requires more than just a signature at closing. It requires a transparent understanding of how interest rates, draw periods, and market values intersect. If you are ready to stop making these common mistakes and start using your equity to build a lasting legacy, we are here to help you navigate the process.

Explore your options, Compare different loan structures, and Access the capital you have worked so hard to build.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664

But there is one more thing most lenders won't tell you about HELOCs during a shifting interest rate environment. If the Federal Reserve makes a sudden move tomorrow, your monthly payment could change before your next statement even arrives. Do you know the "Cap" on your specific loan? Most homeowners don't( until it's too late...)