Your Quick-Start Guide to Regional Equity Trends: Why Your Arkansas HELOC Lender is Seeing a Surge Tonight

Tonight, as the sun sets over the Ozarks and the lights flicker on in Chicago, a specific type of financial activity is humming beneath the surface. Homeowners across the country are waking up to a reality they didn't expect a few years ago: they are sitting on a gold mine of equity.

As of March 25, 2026, the landscape of home financing has shifted. While traditional 30-year fixed rates have seen their ups and downs, the Home Equity Line of Credit (HELOC) has emerged as the Swiss Army knife of real estate finance. Specifically, if you are looking for an Arkansas HELOC lender, you might notice that phone lines are busier than usual tonight.

There is a reason for this surge. It isn't just about spending money; it is about strategic positioning in a market that rewards liquidity.

The Arkansas Surge: Why the Natural State is Leading the Pack

Arkansas has long been a hidden gem for real estate, but the secret is officially out. Markets like Bentonville, Fayetteville, and Little Rock have seen consistent appreciation over the last 24 months. Homeowners who bought five years ago now find themselves with six figures of "accidental equity."

Tonight, your Arkansas HELOC lender is likely processing applications for homeowners looking to renovate before the spring selling season or investors eyeing distressed properties in rural counties. Because the cost of living remains lower than the national average, that equity goes much further here than it would in Los Angeles or Miami.

Explore your options early. When equity increases, your ability to leverage that value into a new investment or a home improvement project increases with it.

The Illinois Connection: Navigating the Prairie State Market

Moving North, the trend continues. An Illinois HELOC lender today is working with a different set of variables. In the Chicago metro area, property values have stabilized, but the demand for updated housing remains at an all-time high.

Illinois homeowners often use HELOCs to combat rising property taxes by increasing the home's functional value or consolidating high-interest debt that accumulated during the inflation spikes of previous years. If you own property in Illinois, your equity is a tool for stability.

Jump in and look at your current valuation. You might be surprised at the borrowing power you have built up while simply living your life.

Essential HELOC Vocabulary for the Modern Borrower

To navigate these waters, you need to speak the language. Here are the core concepts your mortgage strategist will discuss with you.

HELOC (Home Equity Line of Credit)

Definition: A revolving line of credit secured by the equity in your primary residence or investment property.

Application: Use it like a credit card for your house, where you only pay interest on what you actually spend.

LTV (Loan to Value)

Definition: The ratio of your current mortgage balance compared to the appraised value of the home.

Application: Lenders use this to determine how much "room" you have left to borrow.

CLTV (Combined Loan to Value)

Definition: The total of all loans on a property (first mortgage plus the new HELOC) divided by the home's value.

Application: This is the actual number that determines your HELOC limit.

Draw Period

Definition: The timeframe (usually 5 to 10 years) during which you can withdraw funds from your HELOC.

Application: During this phase, you typically make interest-only payments, allowing for maximum cash flow.

DSCR (Debt Service Coverage Ratio)

Definition: A calculation used for investment properties that compares rental income to the monthly mortgage debt.

Application: Investors use HELOCs as down payments for DSCR loans to grow their portfolios without using their own cash.

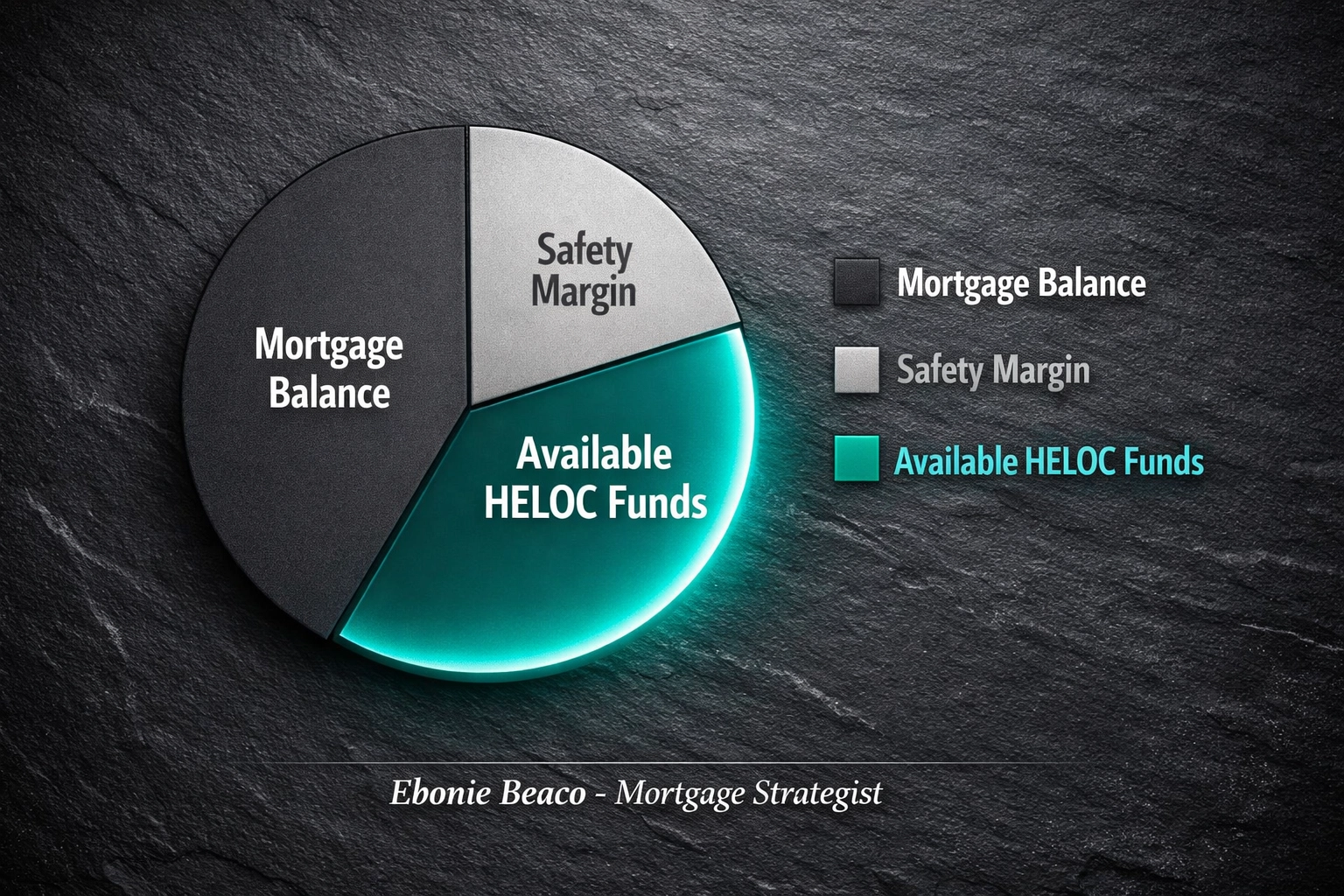

The Math Behind the Surge: A Real-World Example

Let’s look at how a homeowner in a state like Virginia or Georgia might actually use this. Numbers make the strategy clear.

Imagine you own a home valued at $500,000. Your current mortgage balance is $280,000.

Most lenders will allow you to go up to an 85% CLTV.

- Step 1: $500,000 (Value) x 0.85 = $425,000 (Maximum Total Debt Allowed).

- Step 2: $425,000 - $280,000 (Current Mortgage) = $145,000 (Available HELOC).

In this scenario, you have access to $145,000. You don’t have to take it all at once. You could draw $50,000 to fix a roof and update a kitchen, then leave the rest for an emergency fund or a down payment on a rental property.

Accessing this cash doesn't require you to give up your low-interest first mortgage. This is the primary reason why homeowners are choosing HELOCs over cash-out refinances in 2026.

Regional Equity Trends: A Multi-State Perspective

Home Loans Network monitors activity across several key states. Each region shows a unique reason for the current surge in equity interest.

Florida and Georgia: The Sunbelt Strategy

In cities like Atlanta, Savannah, and Tampa, the influx of new residents is driving up prices. Investors in these states are frequently using HELOCs to fund the "Buy" phase of a BRRRR (Buy, Rehab, Rent, Refinance, Repeat) strategy.

California: The Equity Heavyweight

California homeowners often have the largest equity positions in the country. A small percentage of equity in a San Diego or Sacramento home can equal the entire value of a home in the Midwest. Accessing this via a HELOC allows California residents to invest in out-of-state rental markets like Missouri or Kentucky.

Michigan and Indiana: The Renovation Wave

In Detroit and Indianapolis, we see a heavy focus on home improvement. Owners are using their equity to modernize older homes, significantly increasing their resale value in a competitive market.

Virginia and Kentucky: Stability and Growth

Virginia’s market remains robust due to government and tech sector stability. Homeowners here use equity lines as a safety net, ensuring they have access to capital regardless of broader economic shifts.

Strategic Moves for Real Estate Investors

If you are a landlord or a fix-and-flip investor, the HELOC is your best friend.

One of the most popular strategies right now involves using a HELOC on a primary residence to fund a down payment on a DSCR rental property. Because DSCR loans focus on the property's income rather than your personal income, the combination is powerful.

- Extract: Draw $60,000 from your HELOC in Arkansas.

- Invest: Use that $60,000 as a 20% down payment on a $300,000 rental property in Alabama.

- Flow: The rental income covers the new mortgage and the HELOC interest, while you gain the appreciation on a second asset.

This is how wealth is built in 2026. It isn't about working harder; it is about making your existing assets work for you.

Why Transparency is Our Only Policy

At Home Loans Network, we believe in showing you the full picture. A HELOC is a powerful tool, but it is still a loan. It requires a disciplined approach to repayment and a clear understanding of variable interest rates.

Tonight’s surge in interest from Arkansas to Illinois is a sign that people are becoming more financially literate. They understand that sitting on "dead equity" does nothing for their long-term net worth.

Compare your options. Look at the rates: which are currently hovering in the high 7% to low 8% range for well-qualified borrowers: and see if the math works for your specific goals.

Taking the Next Step

Whether you are looking for an Illinois HELOC lender to help consolidate debt or an Arkansas HELOC lender to help you start your investment journey, the process starts with a conversation.

The market moves fast. Regional trends show that those who wait often miss the peak of their borrowing power.

Access the tools you need to make an informed decision. You can start by exploring our mortgage calculators to see how a new line of credit fits into your monthly budget. If you are ready to see what your specific home is worth, you can book an appointment to speak with a strategist.

The equity is yours. How you use it will define your financial trajectory for the next decade.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664