Yes, You Can Buy a Home with an ITIN: Here’s How

Achieving the dream of homeownership is a major milestone, but for many individuals living and working in the United States without a Social Security Number, the process can feel out of reach. If you are an immigrant, a foreign investor, or someone who pays taxes using an ITIN (Individual Taxpayer Identification Number), you might have heard that buying a home is impossible.

I am here to tell you that is simply not true.

At Home Loans Network, we prioritize transparency and education. Whether you are looking for a primary residence in Chicago, an investment property in Florida, or a family home in California, your tax identification status does not have to be a barrier. Exploring your options is the first step toward building wealth through real estate.

Understanding the ITIN

Before we jump into the mortgage details, let's clarify what we are talking about.

ITIN (Individual Taxpayer Identification Number): A tax processing number issued by the Internal Revenue Service (IRS) to individuals who are required to have a U.S. taxpayer identification number but who do not have, and are not eligible to obtain, a Social Security Number (SSN). Practical Application: This number allows you to comply with U.S. tax laws and, more importantly for our purposes, provides a way for lenders to track your financial reliability.

An ITIN is not a work permit, nor does it change your immigration status. However, for the purpose of real estate finance, it serves as a critical tool that allows you to open bank accounts and apply for specific types of mortgage loans.

Does Citizenship Status Affect Property Ownership?

A common misconception is that you must be a U.S. citizen to own land or a home in the United States. In reality, the U.S. does not place restrictions on non-citizens purchasing property.

From the high-rises of Virginia to the suburban neighborhoods of Michigan and Indiana, anyone with the financial means can acquire real estate. The hurdle isn't the ownership itself; it is the financing. Traditional government-backed loans, like FHA or VA loans, typically require a Social Security Number. To get around this, you will look toward Non-QM Mortgage Loans or specialized ITIN lending programs.

How to Obtain Your ITIN

If you do not already have one, obtaining an ITIN is a straightforward process, though it requires patience.

- Complete Form W-7: This is the official IRS application for an ITIN.

- Provide Identification: You will need to submit original documents or certified copies from the issuing agency to prove your identity and foreign status. A valid passport is often the easiest document to use.

- File Your Taxes: Usually, you submit the W-7 along with your federal income tax return.

- Wait for Processing: It generally takes about 7 to 11 weeks to receive your ITIN letter in the mail.

Once you have this number, you are no longer just a renter; you are a potential buyer. You can explore more about these initial steps at our FAQ page.

Title: ITIN Mortgage Solutions. Calculation: Home Value: $350,000 | Down Payment (20%): $70,000 | Loan Amount: $280,000 | Estimated Closing Costs (3%): $10,500 | Total Cash for Closing: $80,500. Ebonie Beaco - Mortgage Loan Officer

Title: ITIN Mortgage Solutions. Calculation: Home Value: $350,000 | Down Payment (20%): $70,000 | Loan Amount: $280,000 | Estimated Closing Costs (3%): $10,500 | Total Cash for Closing: $80,500. Ebonie Beaco - Mortgage Loan Officer

The Requirements for an ITIN Mortgage

Lenders who offer ITIN loans are taking on a different type of risk profile compared to standard borrowers. Because of this, the documentation requirements are often more thorough. Here is what you will generally need to provide to start the loan process:

- Tax Returns: You typically need at least two years of tax returns filed using your ITIN.

- Proof of Income: This includes two years of consistent employment history. If you are self-employed, you might use Bank Statement Loans to prove your cash flow.

- Identification: A valid passport or a government-issued photo ID.

- Residency: Proof that you have lived in the U.S. for a certain period, often shown through utility bills or rental agreements.

- Credit History: While you may not have a traditional FICO score, some lenders allow "alternative credit," such as proof of timely rent and utility payments.

DTI (Debt-to-Income Ratio): A personal financial measure that compares an individual's monthly debt payments to their monthly gross income. Practical Application: Lenders use this to ensure you aren't taking on a mortgage payment that will overwhelm your monthly budget.

Down Payments and Interest Rates

It is important to be transparent about the costs. ITIN loans usually require a larger down payment than conventional loans. While a standard buyer might put down 3% or 5%, an ITIN borrower should prepare for a down payment ranging from 10% to 20%.

Interest rates for ITIN loans are also typically higher than those for borrowers with Social Security Numbers. This is because these loans are held by private lenders rather than being insured by the government. However, as you build equity and establish a stronger credit profile, you may eventually look into a home refinance to secure better terms.

Let’s Look at a Scenario

Imagine you are looking at a property in Arkansas or Alabama for $250,000.

- Purchase Price: $250,000

- Down Payment (15%): $37,500

- Loan Amount: $212,500

By saving for that 15% to 20% down payment, you demonstrate financial stability to the lender, which can sometimes help in negotiating the interest rate.

ITIN Loans for Real Estate Investors

If you are a landlord or an aspiring investor in Georgia or Kentucky, the ITIN program is not just for primary residences. You can use these loans to purchase rental properties.

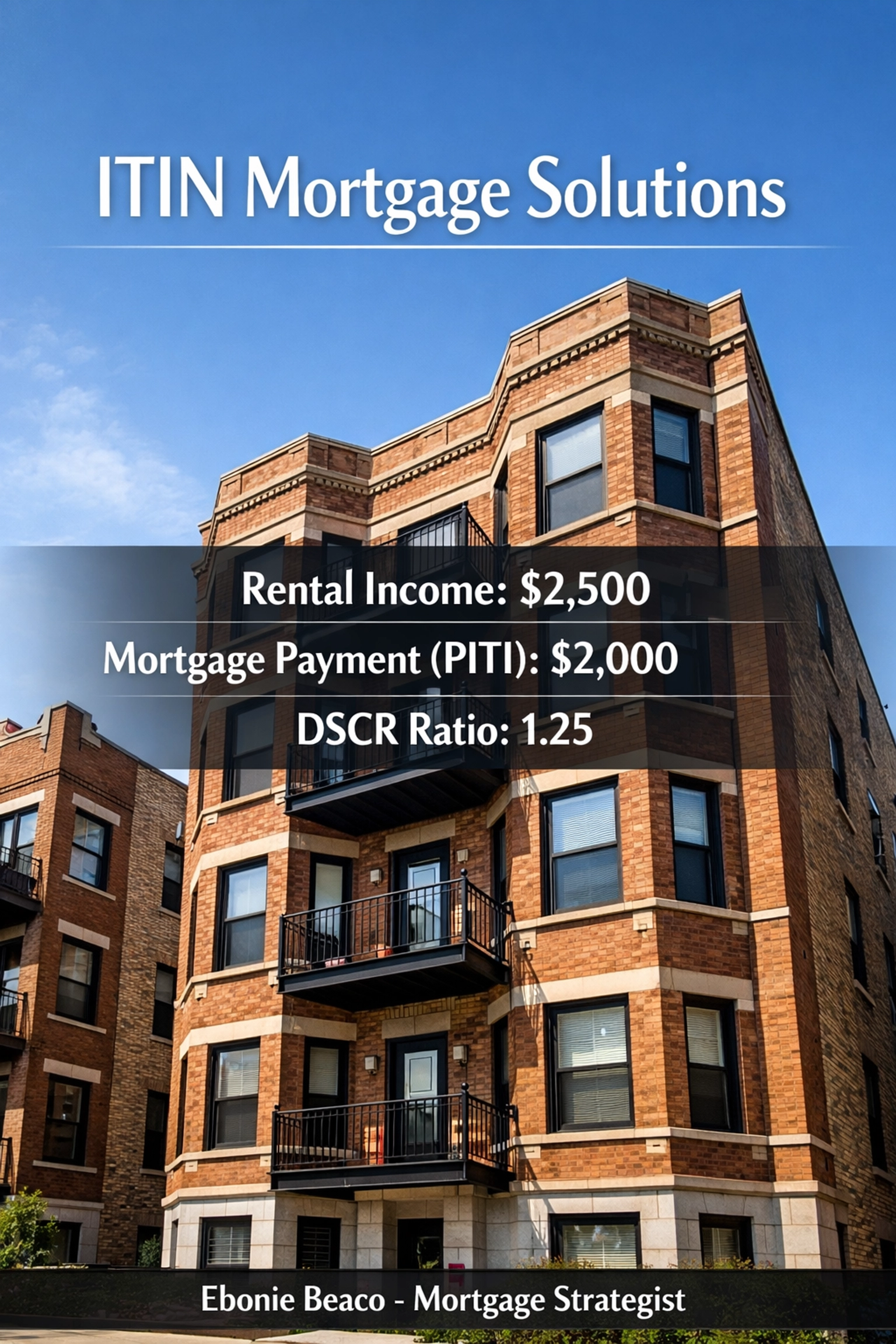

Many investors choose to use DSCR Investor Loans.

DSCR (Debt Service Coverage Ratio): A measurement of a property's ability to cover its own mortgage debt through the rental income it generates. Practical Application: This allows you to qualify for a loan based on the property's projected rent rather than your personal income tax returns.

For ITIN holders, DSCR loans are an incredible way to scale a portfolio without the restrictions of traditional personal income verification. Whether you are targeting short-term rentals in Florida or multi-unit buildings in Illinois, this strategy opens doors that many assume are closed.

The Importance of Professional Guidance

The path to buying a home with an ITIN has more steps than a traditional mortgage, but it is a path that many have successfully walked. Navigating the nuances of non-QM lending requires a strategist who understands the specific programs available in your state.

In states like California and Virginia, where home prices can be higher, knowing exactly how much you need for a down payment and how your DTI is calculated is vital. We want to ensure you feel confident when you submit your online forms and begin the journey.

Title: ITIN Mortgage Solutions. Calculation: Rental Income: $2,500 | Mortgage Payment (PITI): $2,000 | DSCR Ratio: 1.25. Ebonie Beaco - Mortgage Loan Officer

Title: ITIN Mortgage Solutions. Calculation: Rental Income: $2,500 | Mortgage Payment (PITI): $2,000 | DSCR Ratio: 1.25. Ebonie Beaco - Mortgage Loan Officer

Regional Insights

Real estate activity remains vibrant across our service areas.

- In Chicago, ITIN borrowers are revitalizing neighborhoods by purchasing and renovating two-flats.

- In Florida, many international investors use ITINs to fund vacation rentals and Airbnb properties.

- In Missouri and Arkansas, affordable entry-level homes make the 15% down payment requirement more manageable for first-time buyers.

No matter where you are located, the goal remains the same: stop paying a landlord and start building your own equity. If you want to see how the numbers work for your specific situation, you can use our mortgage calculators to run different scenarios.

Take the Next Step

Homeownership is a powerful tool for financial stability and legacy building. If you have been waiting to buy because you only have an ITIN, the wait is over. Access the information you need, compare your options, and jump into the market with a clear plan.

Your status should not limit your potential. We are here to guide you through every document, every calculation, and every milestone.

Are you ready to stop wondering and start owning?

Homeownership is possible with an ITIN. Contact Ebonie Beaco for financing or mentoring.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664