Why Today’s Inflation Data Will Change the Way You Shop for a Home in Florida and Georgia

The release of today’s Consumer Price Index (CPI) report has sent a clear signal through the financial markets, and the impact is already being felt by home shoppers and real estate investors across the Southeast.

In Florida and Georgia, where the housing market remains a primary driver of the local economy, understanding the nuance of this data is essential for anyone looking to secure a mortgage or expand a rental portfolio.

Inflation data serves as the compass for the Federal Reserve, and by extension, the primary catalyst for movement in mortgage interest rates.

When the cost of goods and services cools, the pressure on bond yields often eases, creating a window of opportunity for borrowers who have been waiting on the sidelines.

Explore how these shifting numbers translate into real purchasing power for homeowners and investors in Alabama, Arkansas, California, Florida, Georgia, Illinois, Indiana, Kentucky, Michigan, Missouri, and Virginia.

Defining Inflation and the CPI

Consumer Price Index (CPI): A measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care.

The CPI is the most widely used indicator of inflation and serves as a benchmark for how quickly the purchasing power of the dollar is eroding.

When inflation is high, the Federal Reserve typically raises interest rates to slow down spending; conversely, a cooling CPI suggests that the economy is stabilizing, which can lead to lower borrowing costs.

Jump in and review the latest official updates from the Bureau of Labor Statistics to see the granular breakdown of today's figures.

The Direct Link to Mortgage Rates

Mortgage rates do not move in a vacuum; they are closely tied to the 10-year Treasury yield, which reacts almost instantly to inflation reports.

As today's data suggests a move toward the Fed's target of 2.0%, we are seeing a stabilizing effect on fixed-rate mortgage products.

For a homeowner in a high-growth city like Atlanta or Miami, a half-percentage point drop in interest rates can significantly increase the range of properties they can afford.

Investors tracking DSCR rental property loans also benefit from this cooling, as lower interest rates improve the debt-service coverage ratio, making it easier to qualify for financing on new acquisitions.

Access the Home Loans Network Mortgage Calculators to see how today's rates affect your specific budget.

Why Florida and Georgia Markets Respond Differently

While national inflation data provides the broad strokes, the local markets in Florida and Georgia have unique characteristics that influence how this data applies to you.

Florida continues to see massive domestic migration, which keeps housing demand elevated regardless of slight fluctuations in the national CPI.

Georgia, particularly the metro Atlanta area, serves as a hub for both corporate relocations and first-time homebuyers, making it highly sensitive to changes in monthly payment affordability.

In these states, cooling inflation doesn't just mean lower rates; it often sparks a surge in buyer competition as those who were previously priced out return to the market.

Compare your options for a new home purchase to stay ahead of the competitive curve in these high-demand regions.

Financial Impact: A Real-World Calculation

To understand the practical weight of today's news, we must look at the numbers.

When inflation fears subside, lenders can offer more competitive pricing on conventional and Non-QM mortgage loans.

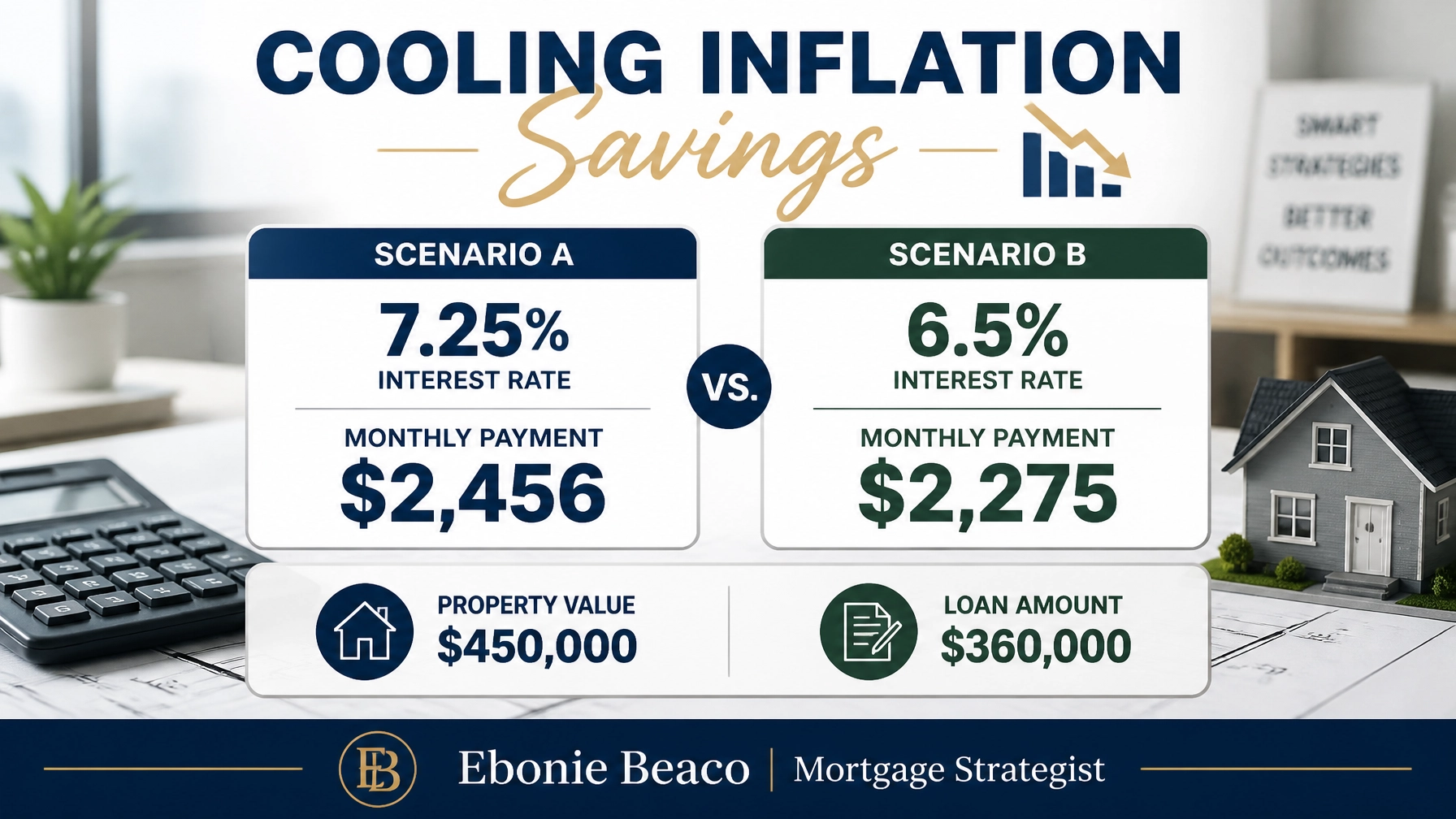

Consider a homebuyer in Savannah or Tampa looking at a property valued at $450,000.

With a 20% down payment, the loan amount is $360,000.

If the interest rate is 7.25% due to high inflation concerns, the monthly principal and interest payment is approximately $2,456.

If today’s cooling inflation data allows that same buyer to lock in a rate of 6.5%, the payment drops to $2,275.

This represents a monthly savings of $181, or more than $2,100 per year, which can be used for property taxes, insurance, or further real estate investments.

Strategies for Investors: DSCR and Fix-and-Flip

DSCR (Debt Service Coverage Ratio) Loan: A mortgage for investment properties that qualifies the borrower based on the property’s cash flow rather than personal income.

Real estate investors in Florida and Georgia frequently use DSCR investor loans to scale their portfolios quickly without the hurdles of traditional W-2 verification.

When inflation numbers come in lower than expected, it often signals a peak in interest rates, which provides a safer entry point for fix and flip financing.

Investors in the "BRRRR" (Buy, Rehab, Rent, Refinance, Repeat) space can use today’s data to plan their exit strategy with more confidence.

Refinancing a renovated property in Birmingham or Indianapolis becomes much more attractive when the long-term rate outlook is trending downward.

Explore our diverse range of loan programs tailored for professional landlords and developers.

Home Equity Solutions: HELOC and Cash-Out Refinancing

For current homeowners who have seen their property values skyrocket over the last few years, today’s inflation data is equally important.

If you are considering a HELOC (Home Equity Line of Credit) to fund a home renovation or consolidate debt, the interest rate you receive is directly influenced by the Fed’s reaction to these CPI reports.

Cash-Out Refinance: A mortgage refinancing option where the new loan is larger than the existing one, allowing the homeowner to take the difference in cash.

Many homeowners in Virginia and Michigan are using cash-out strategies to access the equity they've built to purchase additional short-term rentals or Airbnb properties.

As inflation stabilizes, the cost of these equity-based loans becomes more predictable, allowing for better long-term financial planning.

Check your eligibility for a home refinance to see how much equity you can put to work today.

Your Roadmap in a Changing Market

Success in the Florida and Georgia real estate markets requires more than just finding the right house; it requires a sophisticated financing strategy.

The shift in inflation data today should be seen as an invitation to re-evaluate your current mortgage or investment goals.

Whether you are a first-time buyer in Orlando or a seasoned commercial investor in Chicago, the landscape of "what is possible" has just changed.

Step-by-Step Guidance:

- Review your current credit profile and debt-to-income ratio.

- Analyze the cash flow potential of your target properties using a DSCR calculator.

- Compare fixed-rate options versus adjustable-rate mortgages (ARMs) if you plan a short-term hold.

- Consult with a mortgage strategist to lock in rates when the market shows these dips.

Analyze your next deal with precision to ensure your ROI remains high in any economic climate.

Conclusion

Today’s inflation data confirms that the economic headwinds of the past year are beginning to shift.

For the savvy borrower, this is the time to be proactive rather than reactive.

Lower inflation leads to lower rates, which ultimately leads to more equity and more wealth-building opportunities.

If you are navigating the markets in AL, AR, CA, FL, GA, IL, IN, KY, MI, MO, or VA, having a clear understanding of these financial indicators is your greatest advantage.

Do not wait for the headlines to become common knowledge.

The best deals are often made in the moments immediately following these critical data releases.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664