Why Today’s Economic Data Will Change the Way You Invest in Chicago and Florida Real Estate

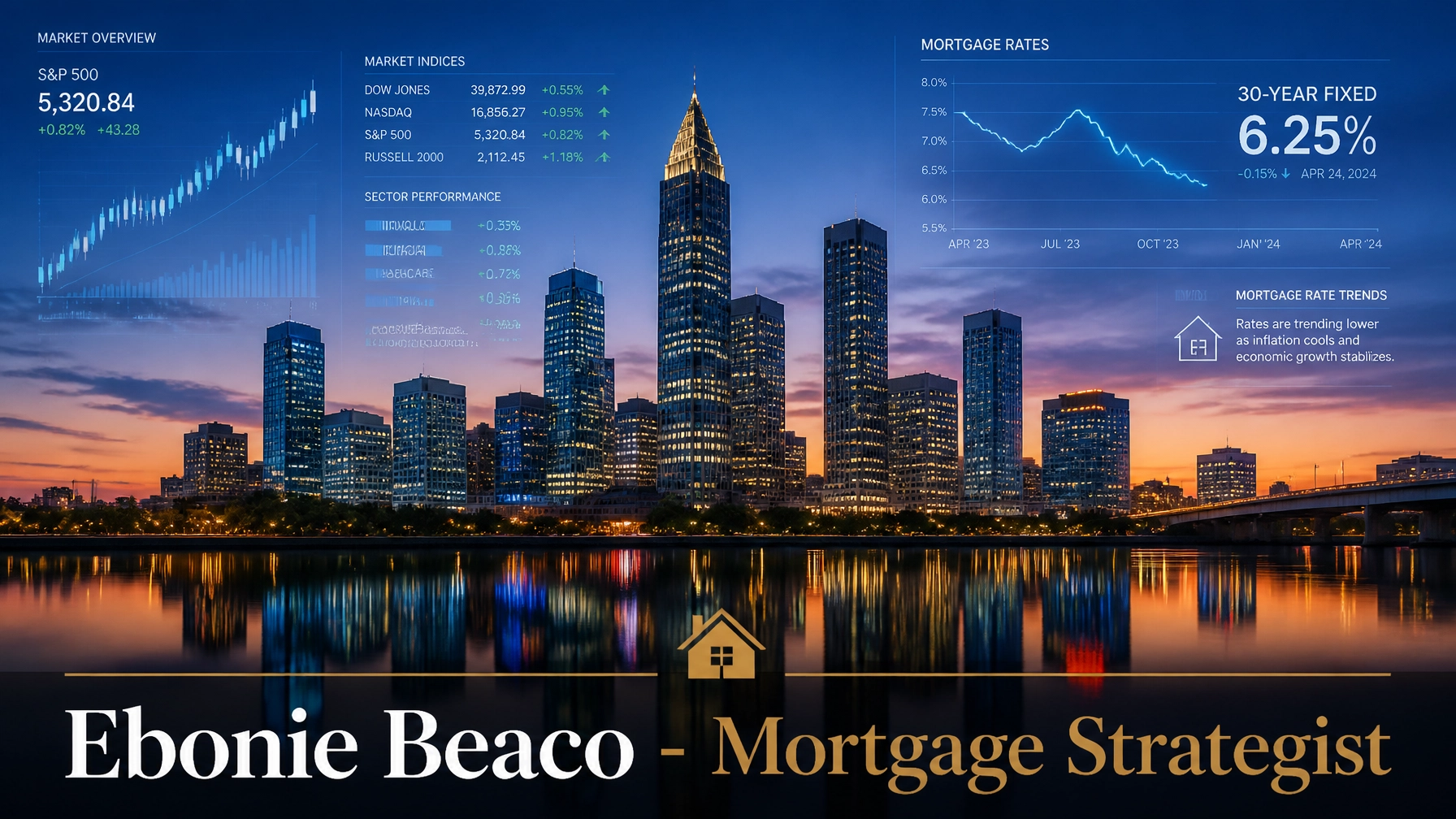

Today marks a significant shift in the financial landscape as the latest economic indicators reveal a complex interplay between inflation, employment, and housing demand. For real estate investors and homeowners in markets like Chicago and Florida, these numbers are far more than just abstract figures on a screen; they are the signals that dictate when to hold, when to flip, and when to tap into equity. As the Federal Reserve continues to navigate the path toward economic stability, the ripple effects are being felt across the mortgage industry, influencing everything from conventional loan rates to specialized investor products. Understanding these shifts is the first step in positioning your portfolio for long-term growth and resilience against market volatility. You can explore our current loan programs to see how these economic changes align with your specific investment goals.

Decoding Today's Economic Indicators

The current economic report highlights a stabilizing Consumer Price Index (CPI), which suggests that the aggressive inflationary pressures of the past few years are beginning to subside. This cooling trend often leads to a more predictable interest rate environment, providing a window of opportunity for those who have been waiting on the sidelines for mortgage rates to soften. However, the labor market remains surprisingly tight, which keeps upward pressure on wages and, consequently, housing demand in major metropolitan areas. For the savvy investor, this data provides the clarity needed to transition from a defensive posture to an offensive strategy. By analyzing these trends today, you can anticipate where capital will flow tomorrow, allowing you to secure properties before the next wave of competition enters the market.

Essential Financial Definitions

CPI (Consumer Price Index): A measure that examines the weighted average of prices of a basket of consumer goods and services.

- Application: You use this to gauge the general direction of inflation and predict how the Federal Reserve might adjust interest rates.

DSCR (Debt Service Coverage Ratio): A metric used by lenders to determine if a property’s rental income can cover its debt obligations.

- Application: You apply for DSCR loans to qualify for financing based on the property's performance rather than your personal income.

LTV (Loan-to-Value): The ratio of a loan to the value of an asset purchased, expressed as a percentage.

- Application: You monitor your LTV to determine how much equity you can access through a cash-out refinance or a HELOC.

DTI (Debt-to-Income): A personal finance measure that compares your monthly debt payments to your gross monthly income.

- Application: You keep your DTI low to ensure you qualify for the most competitive rates on conventional mortgage products.

The Chicago Investment Landscape: Yield and Stability

Chicago remains a cornerstone for investors who prioritize cash flow and historical stability over speculative price appreciation. Unlike many coastal markets that experienced extreme volatility, the Chicago metro area has maintained a steady trajectory, supported by a diverse economy and a robust rental market. Today’s data suggests that while inventory remains tight, the demand for workforce housing and small multifamily properties continues to outpace supply. This environment creates a unique opportunity for house hacking or traditional landlord strategies, particularly in neighborhoods with strong transit access and stable employment hubs. You can use our mortgage calculators to run your own scenarios on Chicago properties and see how the numbers align with your budget.

Investors in Illinois are increasingly looking toward 2-unit and 4-unit buildings as a way to maximize their returns in a high-interest-rate environment. These properties often allow for creative financing solutions, such as using a DSCR loan to scale a portfolio without the limitations of traditional DTI requirements. Because Chicago's rent-to-price ratios are often more favorable than those in the Sunbelt, these assets frequently pencil out even when mortgage rates are elevated. Success in this market requires a deep understanding of local property tax structures and tenant regulations, but the reward is a durable income stream that can weather economic downturns. Jump in and compare the benefits of conventional loans versus non-QM options to find the best fit for your next Chicago acquisition.

Financial Breakdown: DSCR Analysis for a Chicago 4-Unit

When you are evaluating a multi-unit property in Chicago, the Debt Service Coverage Ratio is often the most critical factor for loan approval. Lenders typically look for a ratio of 1.20 or higher, meaning the property generates 20% more income than the cost of the mortgage, taxes, and insurance. In the example below, a classic Chicago brick 4-unit building shows a strong DSCR, demonstrating why these assets are highly prized by experienced landlords. By focusing on the property's ability to generate cash flow, you can secure financing even if you are self-employed or have a complex personal tax return.

The Florida Investment Market: Resilience and Risk Management

The Florida real estate market continues to attract a massive amount of capital, driven by strong inbound migration and a pro-business environment. However, today’s economic data highlights the necessity of a sophisticated approach to risk management, particularly regarding insurance costs and property valuations. While cities like Miami, Orlando, and Tampa offer significant appreciation potential, they also require a more nuanced understanding of short-term rental regulations and climate-related expenses. Investors who succeed in Florida are those who look beyond the surface-level growth and focus on the underlying fundamentals of each submarket. Accessing the right financing strategy is essential for navigating this fast-paced environment and ensuring your capital is deployed efficiently.

One of the most effective strategies for Florida investors right now is the use of cash-out refinancing to unlock equity from existing assets. As property values have surged over the last several years, many owners are sitting on significant amounts of "lazy capital" that could be used to fund new acquisitions or property improvements. Despite the current rate environment, the ability to pull out six figures of tax-free cash can provide the liquidity needed to pounce on distressed deals or fix-and-flip opportunities. By leveraging your existing equity, you can maintain your momentum and continue to scale your Florida portfolio even when traditional lending criteria tighten. Explore how our home refinance options can help you put your equity to work.

Strategy Spotlight: Unlocking Florida Equity with Cash-Out Refinance

In a market like Florida, where appreciation has been rapid, a cash-out refinance can be a game-changer for your investment strategy. If you purchased a property several years ago, your current LTV is likely very low, giving you a substantial cushion to draw from. The calculation below illustrates how an investor can extract over $180,000 in cash from a coastal property while still maintaining a healthy equity position. This strategy allows you to diversify your holdings and capitalize on new opportunities without needing to bring additional outside capital to the table.

National Trends: How Financing Strategies Align with Your Goals

Across the states where we operate: from Alabama and Arkansas to Georgia, Virginia, and Michigan: the theme for this year is adaptability. The "one-size-fits-all" approach to mortgage financing is no longer effective in a market characterized by high rates and varying regional dynamics. Homeowners and investors must look toward a broader suite of products, including Non-QM loans, bank statement programs, and ITIN loans, to find the flexibility they need. These products are specifically designed for the modern borrower, including entrepreneurs and investors who may not fit the rigid mold of traditional banking. Understanding the nuances of each program is how you gain a competitive edge in today's housing market.

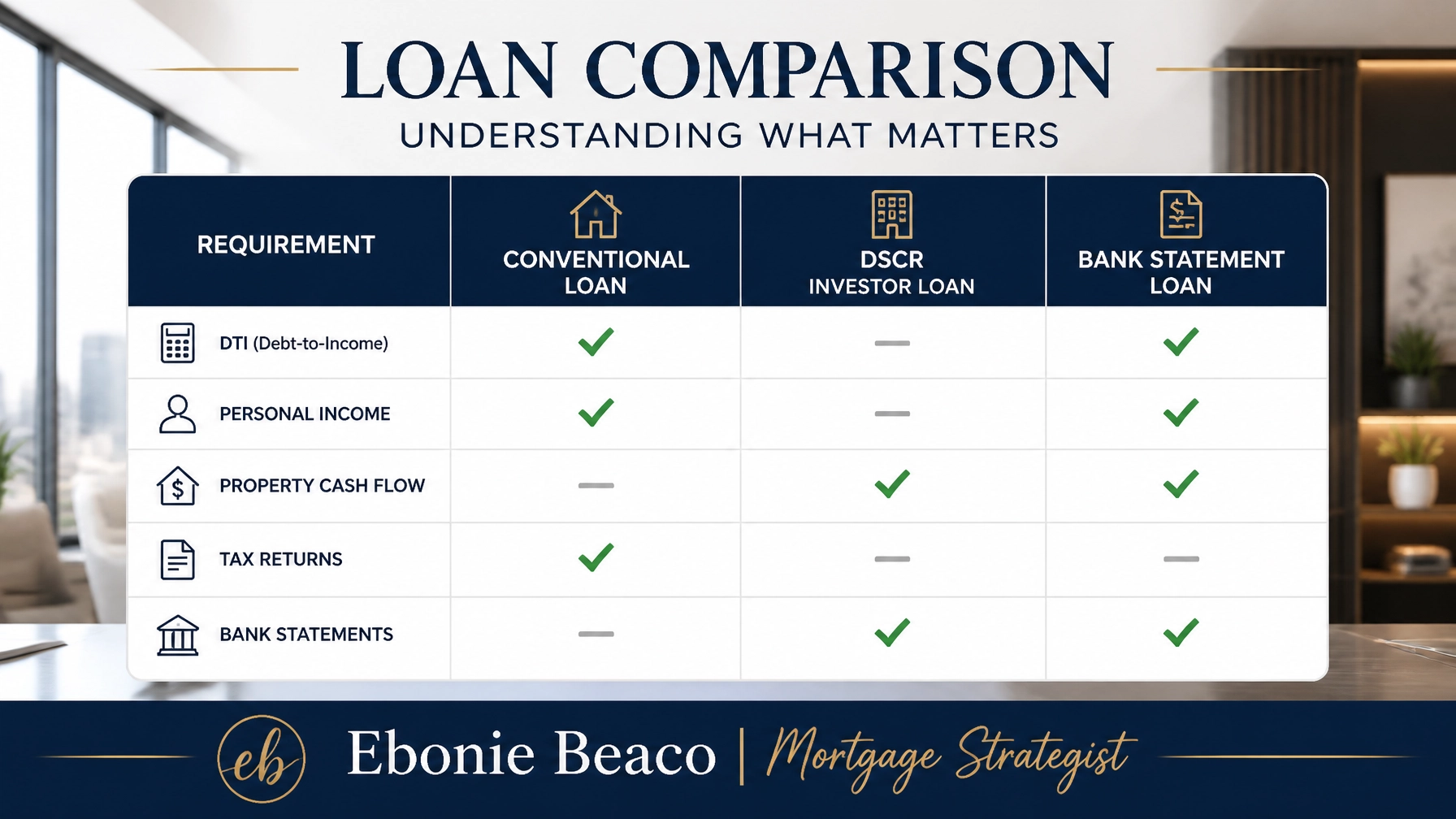

Comparing Non-QM and Traditional Mortgage Options

Choosing the right loan product is a balance between rate, flexibility, and speed. While traditional conventional loans often offer the lowest interest rates, they come with strict documentation requirements and DTI limits that can hinder an active investor's growth. Non-QM products, such as DSCR and bank statement loans, offer a streamlined path to approval by focusing on the asset or the borrower's actual cash flow. The chart below provides a quick comparison to help you determine which path aligns with your current financial profile and long-term objectives.

Future Outlook and Market Predictions

As we look toward the remainder of the year, the consensus among economists is one of cautious optimism. While we may not see a return to the historic low rates of the early 2020s, the current stabilization suggests that the worst of the volatility is behind us. For investors in Chicago and Florida, this means that the focus will shift back to property fundamentals: location, condition, and management. Those who have a clear understanding of today's economic data will be the ones best positioned to capture market share and build lasting wealth. The key is to remain informed, stay flexible, and work with a mortgage strategist who understands the intricacies of complex real estate transactions.

According to recent forecasts from Fannie Mae, we expect home price growth to remain positive but moderate, which is a healthy sign for long-term investors. Similarly, the National Association of Realtors (NAR) continues to highlight the strength of the luxury and cash-buyer segments, which provides a floor for valuations in premium markets. By keeping a pulse on these national trends while executing at the local level, you can build a real estate portfolio that is both profitable and resilient. The information you act on today will determine your financial trajectory for years to come.

If you are looking for clarity on your next mortgage move, let’s talk. Whether you are buying your first home in Indiana, refinancing an Airbnb in Florida, or scaling a multifamily portfolio in Chicago, I can help you navigate the process with ease and confidence.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664