Why Today’s Economic Data Will Change the Way You Approach Mortgage Rates in Florida and California

Economic landscapes shift rapidly, and today, June 4, 2026, marks a pivotal moment for anyone navigating the mortgage markets in Florida and California.

Recent headlines suggest that inflation and labor market data are converging to create a new baseline for interest rates.

You must understand these shifts to protect your home equity and maximize your real estate investment returns.

Whether you are a first-time homebuyer in Georgia or a seasoned investor in Michigan, these updates dictate your next financial move.

Understanding the Technical Landscape

To navigate this market effectively, you should familiarize yourself with the technical indicators driving today's headlines.

CPI (Consumer Price Index)

Dictionary Definition: A measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

Practical Application: High CPI readings typically force mortgage rates upward as the Federal Reserve fights inflation.

DSCR (Debt Service Coverage Ratio)

Dictionary Definition: A financial metric used to evaluate a property’s ability to cover its monthly debt payments using its own rental income.

Practical Application: Investors use DSCR loans to qualify for financing without needing to provide personal tax returns or W-2 income.

HELOC (Home Equity Line of Credit)

Dictionary Definition: A revolving line of credit that allows homeowners to borrow against the equity in their primary or secondary residence.

Practical Application: This tool provides flexible access to cash for renovations or down payments on subsequent properties.

LTV (Loan to Value)

Dictionary Definition: The ratio of a loan to the value of an asset purchased, expressed as a percentage.

Practical Application: Maintaining a lower LTV often helps you secure better interest rates and avoid private mortgage insurance.

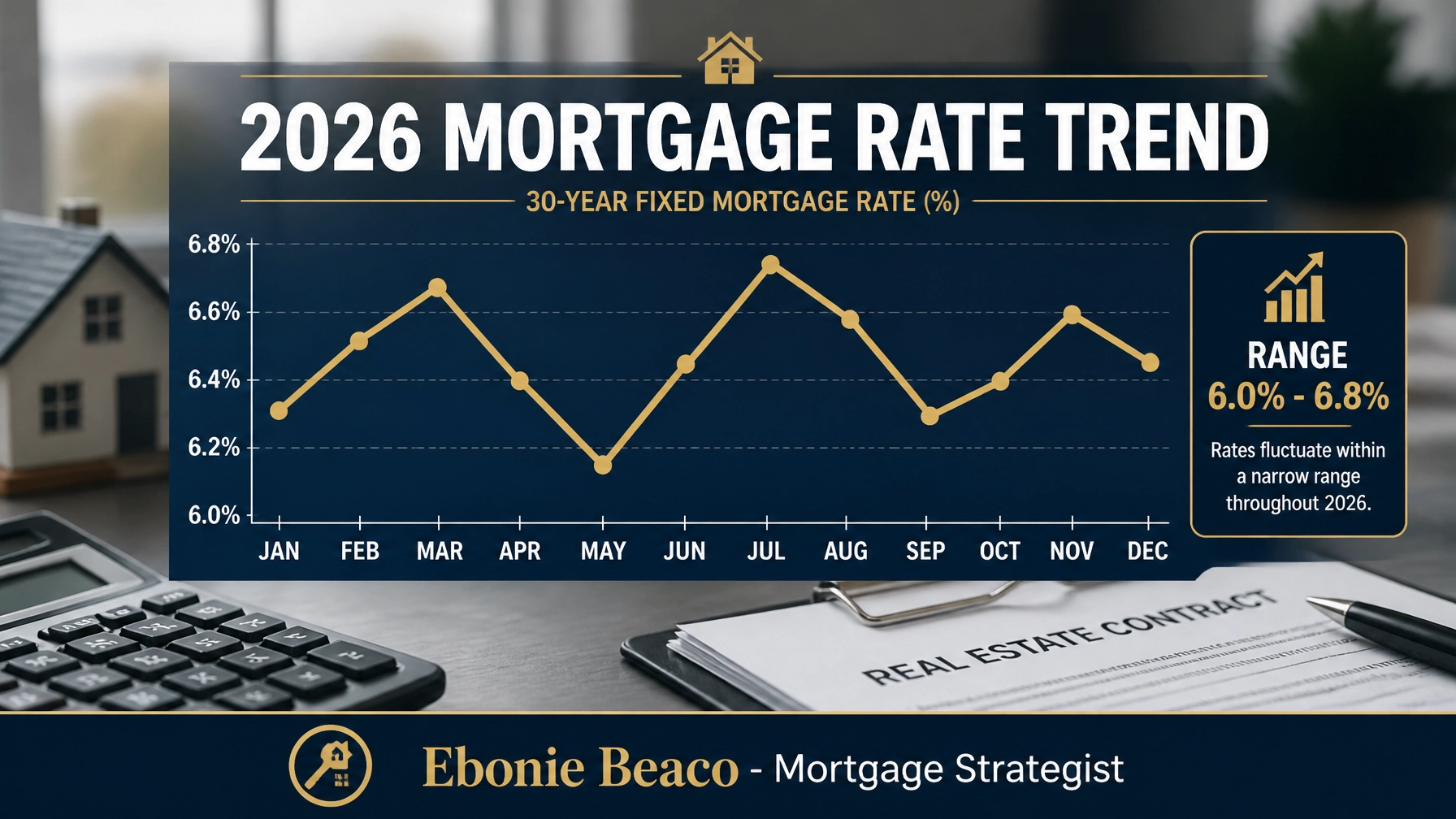

The Impact of Today's Economic Data

Today's economic reports highlight a labor market that is cooling but remains resilient enough to keep the Federal Reserve cautious.

Mortgage rates have recently hovered in the mid-6% range, following a period of volatility that saw five consecutive weekly increases in late May.

Current forecasts from major industry leaders suggest that rates may stay roughly flat or drift slightly lower throughout the month of June.

This stability is a welcome change for buyers in Alabama and Arkansas, where housing demand remains steady despite high financing costs.

Bond market sentiment has improved slightly due to expectations of lower energy prices, which often correlates with lower mortgage pricing.

If upcoming jobs reports show further weakening, you may see rates dip toward the lower 6% range by late June.

California and Florida: Markets Under Pressure

Florida and California represent two of the most sensitive real estate markets in the country due to their unique valuation profiles.

In California, high home prices mean that even a 0.25% change in mortgage rates significantly impacts your monthly payment and overall buying power.

Investors in California often look toward Non-QM loan solutions to manage the high entry costs of coastal properties.

Florida homeowners face different challenges, where rising insurance costs and flood risks often influence the total cost of homeownership more than the interest rate itself.

Regardless of these regional differences, the national bond market sets the base pricing for your loan, making today's data essential reading for everyone.

Residents in Indiana, Illinois, and Kentucky should also watch these trends closely, as local market activity often follows national rate shifts.

Strategic Financing for Real Estate Investors

Smart investors do not wait for the "perfect" rate; they use strategic financing to make deals work in any environment.

DSCR Investor Loans

For those looking to expand portfolios in Georgia or Missouri, DSCR loans remain the preferred choice for purchasing rental properties.

These loans focus on the cash flow of the property itself, allowing you to scale your portfolio without the limitations of your personal debt-to-income ratio.

Fix and Flip Financing

In competitive markets like Virginia and Michigan, bridge loans and fix-and-flip financing provide the speed necessary to secure distressed assets.

You can access short-term capital to renovate a property and then refinance into a long-term DSCR or conventional loan once the value has increased.

Practical Scenario: Calculating a DSCR Loan

Let's look at how an investor might analyze a potential rental property purchase in today's market.

Imagine you are purchasing a rental property in Florida valued at $450,000 with a strong history of rental income.

If the property generates $48,000 in annual gross rent and the annual debt service is $36,000, your DSCR is 1.33.

Lenders typically look for a DSCR of 1.20 or higher, meaning this property easily qualifies for competitive investor financing.

This strategy allows you to acquire the asset based on its performance, protecting your personal credit capacity for other opportunities.

Explore more about how these numbers work by visiting our mortgage basics guide.

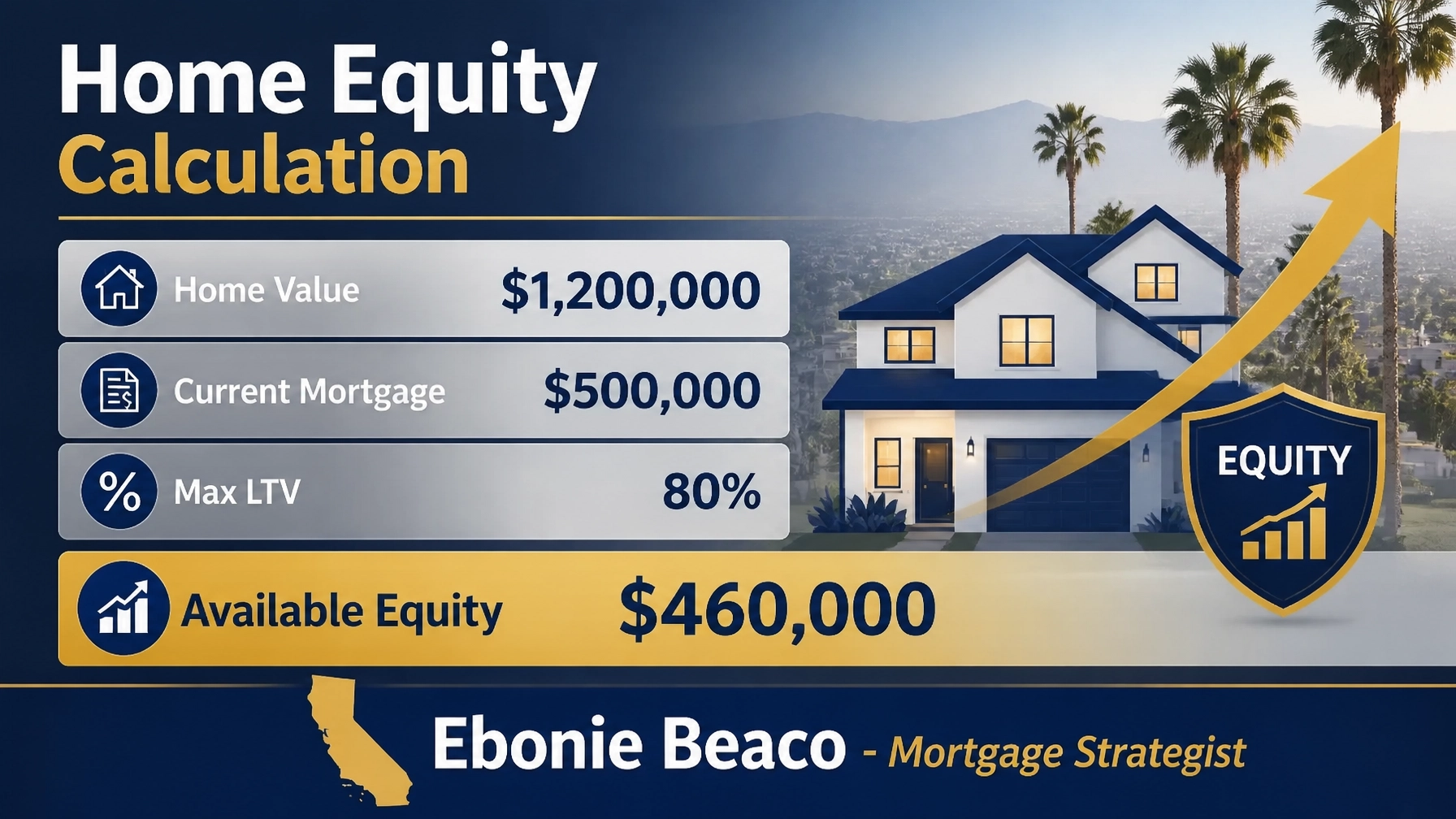

Accessing Equity Through a HELOC or Cash-Out Refinance

Homeowners in high-appreciation states like California often find themselves sitting on significant amounts of "lazy" equity.

You can put this equity to work through a HELOC or a cash-out refinance to fund home improvements or new investments.

Consider a California homeowner with a property valued at $1,200,000 and an existing mortgage balance of $500,000.

Under standard 80% LTV guidelines, the homeowner could potentially access up to $460,000 in available equity.

Using this capital for a down payment on a multi-unit property in Chicago or a short-term rental in Florida can accelerate your wealth-building journey.

Navigating the Loan Process

Understanding the loan process is the first step toward securing your financial future in this changing market.

You should start by requesting a soft-pull credit request to see where you stand without affecting your credit score.

This transparency allows you to compare different loan programs, from FHA and VA loans to specialized bank statement loans for the self-employed.

Today’s economic news might feel complex, but it essentially provides a roadmap for your timing and strategy.

Stay informed, watch the jobs reports, and look for opportunities where others see uncertainty.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664