Why This Morning’s Rate Movement Will Change the Way You Hunt for Homes in Georgia

This morning, the financial markets signaled a shift that carries significant implications for anyone navigating the real estate landscape in Georgia. As of May 27, 2026, mortgage rates have shown a new level of persistence, moving slightly in response to the latest inflation data and Treasury yield adjustments. For prospective homebuyers in Atlanta, Savannah, and across the state, these micro-movements dictate your purchasing power and the monthly commitment of your next Home Purchase. Understanding the underlying mechanics of these daily shifts is the first step toward securing a deal that aligns with your long-term wealth goals. While some may wait for a dramatic drop, savvy market participants are learning to navigate the current environment with precision.

Decoding the Morning Headlines: What the New Yield Means for You

The 10-year Treasury yield, a primary benchmark for fixed-rate mortgages, saw a notable uptick in early trading today, reflecting a cautious but steady economic outlook. When yields rise, mortgage lenders typically adjust their pricing upward to maintain profitability, which directly impacts the interest rates offered to consumers. This morning's movement suggests that we are entering a period of prolonged stability where rates fluctuate within a narrow, albeit elevated, band. According to recent market reports from NerdWallet, the expectation for a rapid return to 5% has largely faded, replaced by a focus on steady management. For you, this means that the cost of borrowing is unlikely to change drastically in the next few weeks.

Many observers are closely watching the Federal Reserve's stance on inflation, which remains the primary driver behind these rate decisions. When inflation cools slower than anticipated, the "higher for longer" narrative gains traction, keeping conventional loan rates in the high 6% to low 7% range. This environment requires a shift in strategy, moving away from timing the bottom and toward identifying properties that generate value even at today's costs. Those who understand that rates are a tool rather than an obstacle can find opportunities that others overlook during periods of uncertainty. Explore your options early so you can act when a property fits your specific financial profile and lifestyle needs.

The Georgia Housing Market: A Snapshot of Inventory and Demand

Georgia continues to be a focal point for real estate activity, driven by a growing population and a robust job market in sectors like technology and logistics. However, the inventory of available homes remains tight, particularly in high-demand areas like the Atlanta metro region and North Georgia. This scarcity often creates a competitive floor for prices, ensuring that well-located homes retain their value despite higher borrowing costs. Real estate investors and homeowners alike are finding that the "wait and see" approach often leads to higher entry prices later as demand continues to outpace supply. Jump in by reviewing the latest conventional loan guidelines to see how you can position yourself as a strong buyer.

In cities like Savannah and Augusta, the market reflects a similar trend of resilience, with buyers competing for a limited pool of updated properties. The recent rate movement makes it essential to work with a strategist who can help you compare different financing structures to offset higher interest expenses. Many sellers are now open to creative concessions, such as temporary rate buydowns, which can significantly lower your initial monthly payments. This proactive approach allows you to secure a home now while preserving the option to refinance if rates eventually trend lower in the coming years. Accessing the market with a clear understanding of your local inventory is the best way to ensure your search remains productive.

Essential Mortgage Terms Every Georgia Buyer Should Know

Navigating the mortgage process requires a firm grasp of the terminology that lenders and strategists use to define your loan. Below are several key concepts explained simply to help you interpret the documents and disclosures you will encounter during your home search.

Basis Points (BPS): A unit of measure used in finance to describe the percentage change in the value of financial instruments or the rate of change in interest rates.

Practical Application: If a lender says rates moved up 25 basis points, it means the interest rate increased by 0.25%.

Debt-to-Income Ratio (DTI): A personal financial measure that compares your monthly debt payments to your monthly gross income.

Practical Application: Lenders use this to determine how much you can comfortably afford to borrow each month without overextending your budget.

Loan-to-Value (LTV): The ratio of a loan to the value of an asset purchased, expressed as a percentage.

Practical Application: If you put down 20% on a $400,000 home, your LTV is 80%, which often allows you to avoid paying private mortgage insurance.

Debt Service Coverage Ratio (DSCR): A measure of the cash flow available to pay current debt obligations, used primarily in investment property financing.

Practical Application: Investors use DSCR loans to qualify based on the property’s rental income rather than their personal tax returns.

Strategic Financing for Investors: DSCR and Non-QM Options

For real estate investors in Georgia, this morning's rate movement highlights the importance of choosing the right loan product for your specific portfolio goals. Conventional financing may not always be the best fit, especially for those who are self-employed or looking to scale their rental holdings quickly. Non-QM (Non-Qualified Mortgage) loans offer a flexible alternative, allowing borrowers to qualify using bank statements or the projected income of the property itself. These programs are particularly popular for Airbnb and short-term rental operators who need to account for fluctuating seasonal income. By focusing on the property’s performance rather than personal W-2 income, you can often secure funding for multiple deals simultaneously.

The DSCR loan is currently a dominant tool for landlords seeking to acquire or refinance residential properties in Georgia. Because the qualification is tied to the rental revenue of the home, investors do not have to worry about the impact of their personal debt-to-income ratios. This strategy is ideal for those looking to implement the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) method in growing markets like Columbus or Macon. Even with rates in the 7% range, if the property's cash flow covers the debt at a 1.20 ratio or higher, the deal remains viable. Accessing these specialized products requires working with a strategist who understands the nuances of investor-focused lending.

Unlocking Equity: How Homeowners Are Winning in a High-Rate Environment

While current rates may seem high for new purchases, many existing homeowners in Georgia are sitting on record amounts of home equity. This equity can be accessed through a HELOC (Home Equity Line of Credit) or a cash-out refinance to fund home improvements, consolidate high-interest debt, or even purchase a new investment property. Instead of selling a home with a low legacy rate, many owners are choosing to keep their current mortgage and use a second lien to tap into their wealth. This allows you to maintain your low-cost primary debt while still putting your home’s value to work for your future financial stability.

Strategic use of home equity is a hallmark of successful wealth building in the modern economy. For example, a homeowner in Gwinnett County with $200,000 in untapped equity could potentially access $150,000 to use as a down payment for a duplex. This move creates a second stream of income and adds another asset to their portfolio without requiring them to sacrifice their original 3% or 4% interest rate. Comparing the cost of a HELOC versus a full refinance is a critical step in this process to ensure the numbers align with your budget. Explore how your home can serve as a funding machine for your next big financial move by looking at your current equity position.

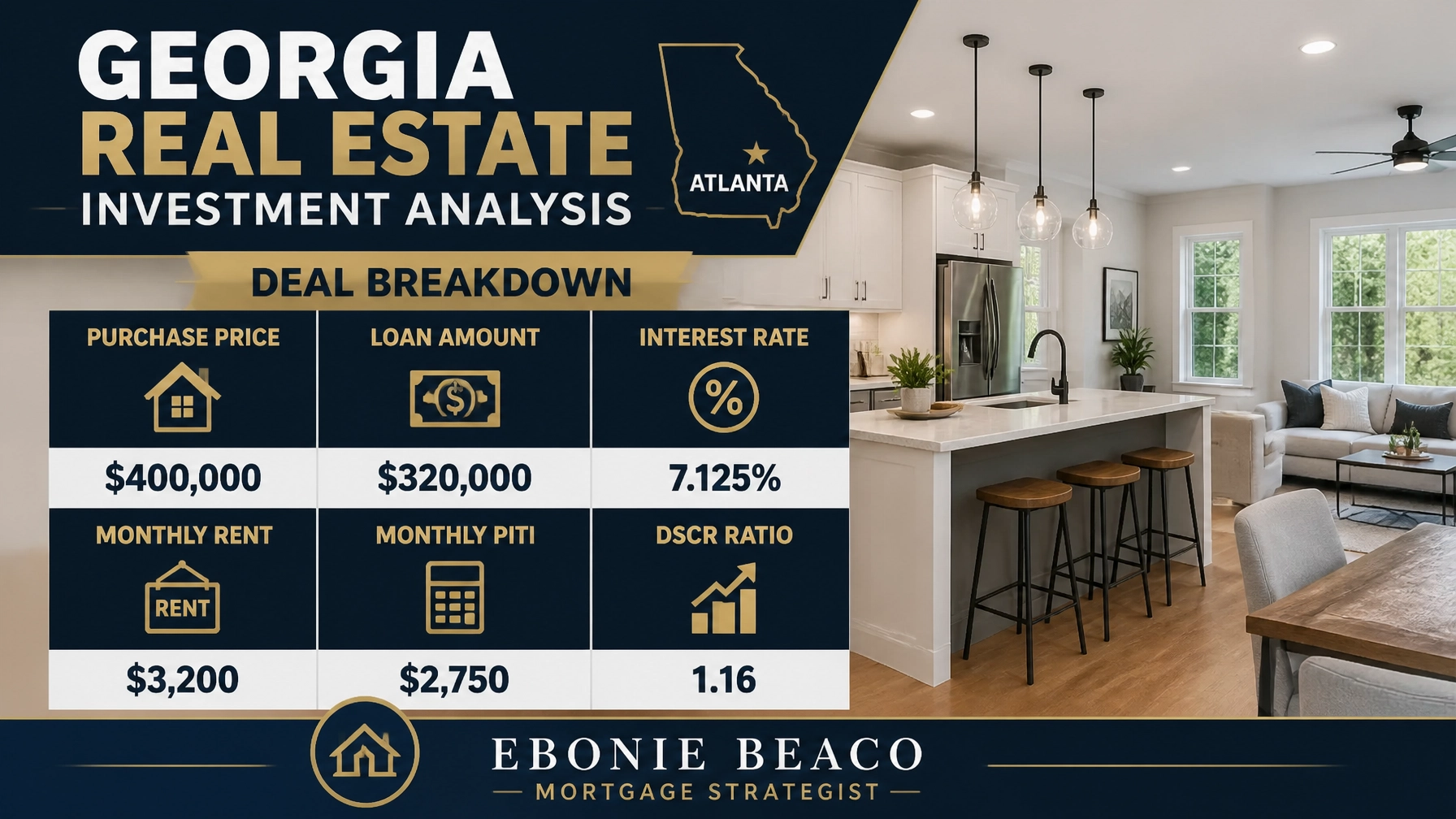

A Closer Look: The Financial Breakdown of a Georgia Rental Property

To illustrate how these concepts translate into a real-world scenario, let's examine a typical investment property deal in the Atlanta suburbs. This example assumes a 30-year fixed-rate DSCR loan, which is common for investors looking for long-term stability and ease of qualification.

In this scenario, an investor identifies a single-family home priced at $400,000 with a projected monthly rent of $3,200. With a 20% down payment ($80,000), the loan amount is $320,000. At a current rate of 7.125%, the monthly PITI (Principal, Interest, Taxes, and Insurance) is approximately $2,750. This results in a DSCR of 1.16, meaning the property generates 16% more income than is required to cover the mortgage payment. While the cash flow may be tighter than it was three years ago, the investor is acquiring a hard asset in a high-demand market where rents and property values are expected to rise over time.

This strategy focuses on the long-term appreciation and tax benefits associated with real estate ownership rather than just immediate monthly cash flow. By securing the property now, the investor benefits from future rent increases while the mortgage payment remains fixed for the life of the loan. If rates move lower in the future, a refinance can further increase the monthly profit margin. Understanding these calculations helps you move forward with confidence, knowing that your investment is grounded in sound financial principles. Compare your own scenarios and ask questions to see how today's rates can still work in your favor when the deal is structured correctly.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664