Today is Wednesday, March 25, 2026. Just one week ago, the Federal Open Market Committee (FOMC) concluded its March meeting. As anticipated by many market observers, the Federal Reserve elected to maintain the federal funds rate at its current range of 3.50% to 3.75%.

On the surface, a "hold" suggests stability. Many homeowners in Missouri and throughout the Midwest have been conditioned to believe that if the Fed stops hiking rates, mortgage costs will eventually drift lower. However, the market reality of the past seven days has told a different story.

Mortgage rates have actually moved upward since the announcement.

As a mortgage strategist, I see this as a critical inflection point. If you are a homeowner in St. Louis, Kansas City, or Springfield, or an investor looking to scale a portfolio across Alabama, Florida, or Illinois, understanding why this decoupling is happening is essential to your financial health.

The Fed’s decision to stay the course is not a green light to wait for lower rates. It is a signal that the floor for borrowing costs has likely shifted higher than many anticipated.

The Great Decoupling: Fed Funds vs. Mortgage Rates

A common misconception among borrowers is that mortgage rates move in lockstep with the Federal Reserve. This is rarely the case. While the Fed controls the federal funds rate (the overnight lending rate between banks), mortgage lenders look to the 10-year Treasury yield as their primary benchmark.

The current disconnect is driven by inflation expectations and global uncertainty. Even though the Fed held rates steady, the 10-year Treasury yield spiked following the meeting. Why? Because the market is pricing in "sticky" inflation.

According to recent analysis from Bankrate regarding the March 18, 2026 meeting, the Fed raised its 2026 inflation projections to 2.7%. This tells the bond market that the central bank is not yet confident in its ability to bring prices down to its 2% target. When the bond market anticipates persistent inflation, yields rise. When yields rise, mortgage rates follow.

Visual Description: A realistic, wide-angle shot of a modern professional boardroom in a high-rise office. The lighting is natural and the atmosphere is one of serious financial strategy. Text Overlay at the bottom: Ebonie Beaco - Mortgage Strategist

Visual Description: A realistic, wide-angle shot of a modern professional boardroom in a high-rise office. The lighting is natural and the atmosphere is one of serious financial strategy. Text Overlay at the bottom: Ebonie Beaco - Mortgage Strategist

Why Missouri Homeowners Should Stop Waiting

If you have been sitting on the sidelines in Missouri, waiting for a "rate cut" before you refinance or pull equity for an investment, you may be falling into a psychological trap. The "wait and see" approach often leads to missed opportunities.

Rate Timing Risk

The risk that an individual waits for a specific economic event (like a Fed cut) only to find that the market has already priced in that event or moved in the opposite direction.

Wait-and-see behavior assumes that future rates will be lower than they are today. However, with crude oil prices fluctuating and Middle East tensions adding a layer of uncertainty, the cost of debt could remain elevated for years.

Homeowners in Missouri who are waiting for 5% or 4% rates may find themselves still waiting in 2027, while the equity they could have utilized today remains trapped and unproductive.

Strategic Equity Access: The Power of the HELOC and Cash-Out Refi

For homeowners in Missouri and our neighboring states like Arkansas, Kentucky, and Indiana, the focus should shift from "rate chasing" to "equity utilization." Your home is not just a place to live; it is a financial tool.

HELOC (Home Equity Line of Credit)

A revolving line of credit that allows you to borrow against the equity in your home as needed, typically featuring a variable interest rate.

Application: Access funds for a down payment on a Missouri rental property without disturbing your current low-rate first mortgage.

Cash-Out Refinance

A new mortgage for more than you owe on your current home, where the difference is paid to you in cash.

Application: Consolidate high-interest credit card debt or fund a major renovation project to increase property value.

Explore your options for accessing equity safely by visiting our home refinance page.

Investment Strategies for the 2026 Market

Real estate investors in markets like Chicago, Illinois, or the coastal regions of Virginia and Florida are moving away from traditional financing and toward more sophisticated structures. If the Fed is holding rates, the "smart money" is looking at yield rather than just the interest rate.

One such strategy is the DSCR (Debt Service Coverage Ratio) Loan.

DSCR Loan

A mortgage program for real estate investors that qualifies the borrower based on the rental income generated by the property rather than personal income or employment history.

Application: Scale a portfolio of rental properties in Indiana or Michigan without the debt-to-income (DTI) constraints of traditional lending.

This is particularly relevant for Missouri investors. If you find a multi-unit property in a high-demand area, the ability to qualify based on the property's performance allows you to act quickly, even in a higher-rate environment.

Visual Description: A realistic exterior of a classic, established bank building with limestone columns and large glass windows. The setting is clean and professional. Text Overlay at the bottom: Ebonie Beaco - Mortgage Strategist

Visual Description: A realistic exterior of a classic, established bank building with limestone columns and large glass windows. The setting is clean and professional. Text Overlay at the bottom: Ebonie Beaco - Mortgage Strategist

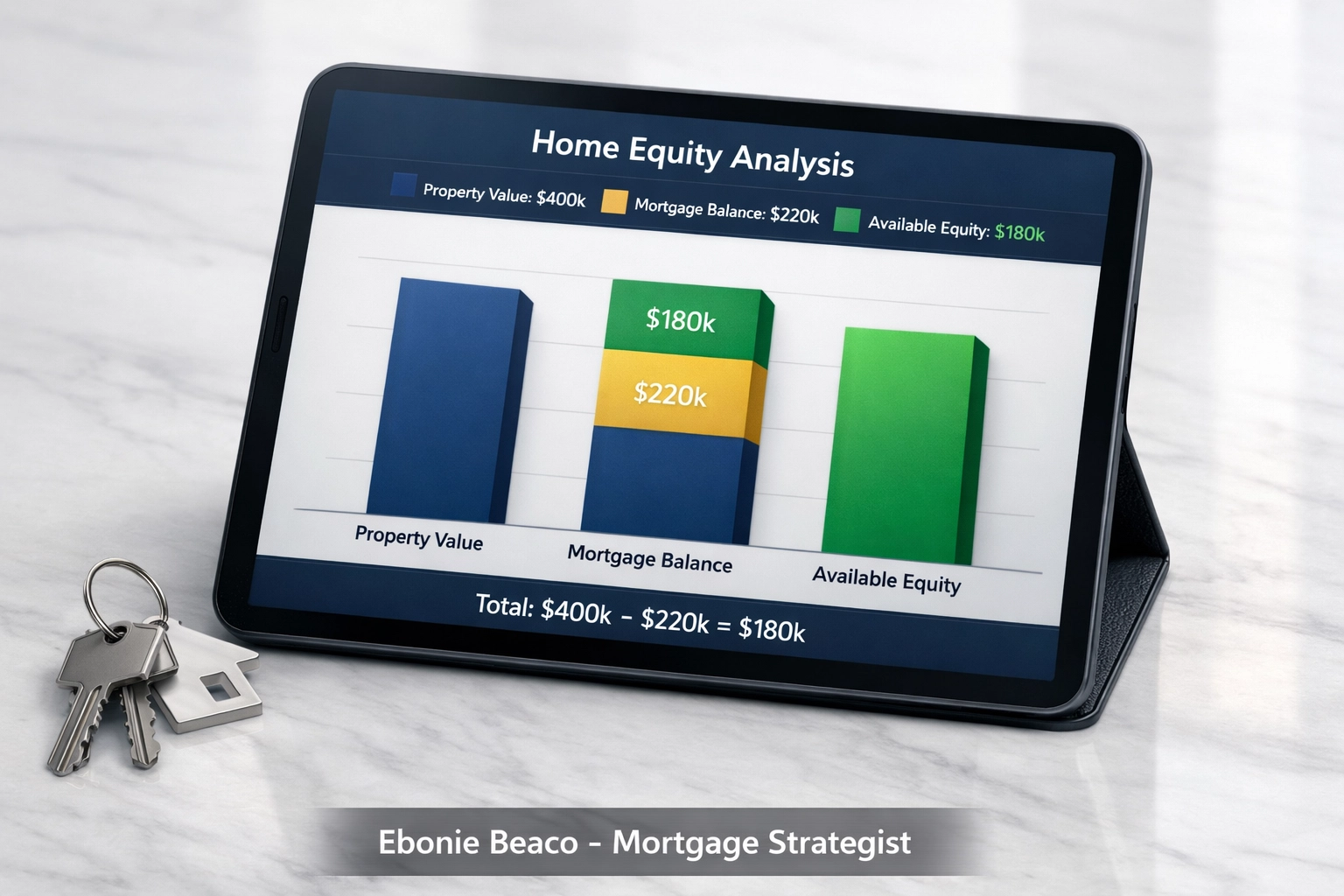

Analyzing the Numbers: A Missouri Equity Case Study

To understand the practical impact of these strategies, let’s look at a typical scenario for a homeowner in the St. Louis suburbs.

The Scenario:

- Current Property Value: $400,000

- Existing Mortgage Balance: $220,000

- Total Available Equity: $180,000

If this homeowner wants to use a Cash-Out Refinance to fund a new investment property while maintaining a 75% Loan-to-Value (LTV) ratio, the math looks like this:

- New Loan Amount (75% of $400k): $300,000

- Payoff Existing Mortgage: $220,000

- Cash to Homeowner: $80,000 (minus closing costs)

With that $80,000, the homeowner could potentially put a 20% down payment on a $350,000 rental property in a growing market like Huntsville, Alabama or Savannah, Georgia. Even if the interest rate on the new loan is higher than the original, the Total Return on Investment (ROI) from the new rental property and the tax advantages of the mortgage interest often outweigh the cost of the higher rate.

Visual Description: A professional financial chart illustrating a deal breakdown. It shows: Property Value $400,000, Current Loan $220,000, New Loan $300,000, and Cash to Borrower $80,000. Text Overlay at the bottom: Ebonie Beaco - Mortgage Strategist

Visual Description: A professional financial chart illustrating a deal breakdown. It shows: Property Value $400,000, Current Loan $220,000, New Loan $300,000, and Cash to Borrower $80,000. Text Overlay at the bottom: Ebonie Beaco - Mortgage Strategist

The Path Forward: Education Over Speculation

The Federal Reserve’s "hold" is a reminder that we are in a "higher for longer" environment. This doesn't mean the real estate market is stalled; it means the strategies for winning have changed.

For Realtors and Wholesalers in Florida, Georgia, and Missouri, your clients need guidance on how to structure deals that make sense today. Waiting for a rate drop that may not come for 12 or 18 months is a strategy based on hope, not data.

Non-QM Mortgage Loans

Mortgage products designed for borrowers who do not meet the strict criteria of major government-backed agencies, often used by self-employed individuals or those with complex financial situations.

Application: Bridge the gap for a buyer in Michigan who has the assets but doesn't fit the standard "W-2" mold.

Compare different loan programs and their requirements on our loan programs page.

Conclusion: Taking Control of Your Financial Timeline

The signals from the Federal Reserve in March 2026 are clear: they are in no rush to lower rates. If you are a homeowner in Missouri or any of the states we serve: from the Midwest to the Southeast: your focus should be on how to maximize your current position.

Whether you are looking for Fix and Flip Financing in Indiana, Airbnb and Short-Term Rental Financing in Florida, or a simple HELOC in Virginia, the key is to act based on the numbers available today.

The decoupling of the Fed and mortgage rates means you cannot rely on headlines to tell you when to move. You need a strategy tailored to your specific goals and your specific market.

Explore your options today. Do not let the "hold" hold you back.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664