Why Everyone Is Talking About Virginia HELOCs Right Now (And You Should Too)

Homeowners in Virginia and across the country are sitting on a goldmine. As of May 2026, U.S. homeowners hold a staggering $34.5 trillion in home equity. That averages out to roughly $302,000 per homeowner. Despite this massive wealth, only a tiny fraction of people are actually using it to their advantage.

If you own a home in Richmond, Virginia Beach, or Northern Virginia, you likely have more "tappable" equity today than you did just two years ago. The same holds true for homeowners in Michigan, Florida, and Georgia. But sitting on equity is like having a high-balance savings account that earns zero interest while you pay high interest on other debts.

Explore why the Virginia HELOC market is buzzing and how you can use this tool to build your real estate portfolio or clean up your finances.

The "Invisible ATM" Hiding in Your Walls

Many people think of their home solely as a place to live or a long-term nest egg. While that is true, your home is also a powerful financial engine. A Home Equity Line of Credit (HELOC) allows you to treat your property like a flexible, revolving credit line.

Think of a HELOC as a credit card secured by your home, but with much lower interest rates. You only pay interest on the amount you actually use. This flexibility is perfect for investors who need quick access to cash for a down payment or homeowners who want to tackle renovations in phases.

In states like Virginia and Michigan, home values have shown incredible resilience. This growth has created an "invisible ATM" for those who know how to access it. Whether you are looking for a Virginia HELOC lender or a Michigan HELOC lender, the strategy remains the same: leverage your equity to move your financial needle forward.

What Is a HELOC and Why Is 2026 the Year to Use It?

A HELOC is a second mortgage that sits behind your primary loan. You keep your low-interest first mortgage exactly where it is. This is a massive benefit for anyone who locked in a 3% or 4% rate years ago.

You get a draw period, usually ten years, where you can take money out and put it back in as needed. During this time, many programs offer interest-only payments, which keeps your monthly overhead low. After the draw period ends, you enter the repayment phase.

In 2026, the mortgage landscape has shifted. While interest rates have stabilized, equity growth hasn't stopped. Using a HELOC is a smart way to access capital without resetting the clock on your 30-year fixed primary mortgage. It’s a surgical tool for your finances rather than a sledgehammer.

The Virginia Surge: Why Richmond and NoVA Are Exploding

Virginia homeowners are currently in a very favorable position. Data from the Richmond MSA shows that homeowners have gained nearly $193,000 in equity over the last decade. In areas like Arlington and Alexandria, that number is even higher, with many owners seeing over $195,000 in growth in just five years.

The Virginia Beach and Norfolk markets are also seeing prices outpace the national average by significant margins. This means if you bought a home in these areas even a few years ago, you likely have a substantial cushion.

As a Virginia HELOC lender, we see clients using these funds to buy investment properties in other states, pay for private tuition, or consolidate high-interest credit card debt that has become unmanageable in the current economy.

Michigan Real Estate: A Hidden Gem for Equity Users

While the coasts often get the headlines, Michigan is quietly becoming a favorite for real estate investors. Markets like Grand Rapids and the Detroit suburbs have shown steady, reliable appreciation.

Many of our clients who work with a Michigan HELOC lender use their primary residence equity to fund rental acquisitions. Michigan's entry price point for rental properties is often more accessible than Northern Virginia or Florida. This allows an investor to take $50,000 from a HELOC and potentially purchase two rental doors in Michigan, creating an immediate new stream of passive income.

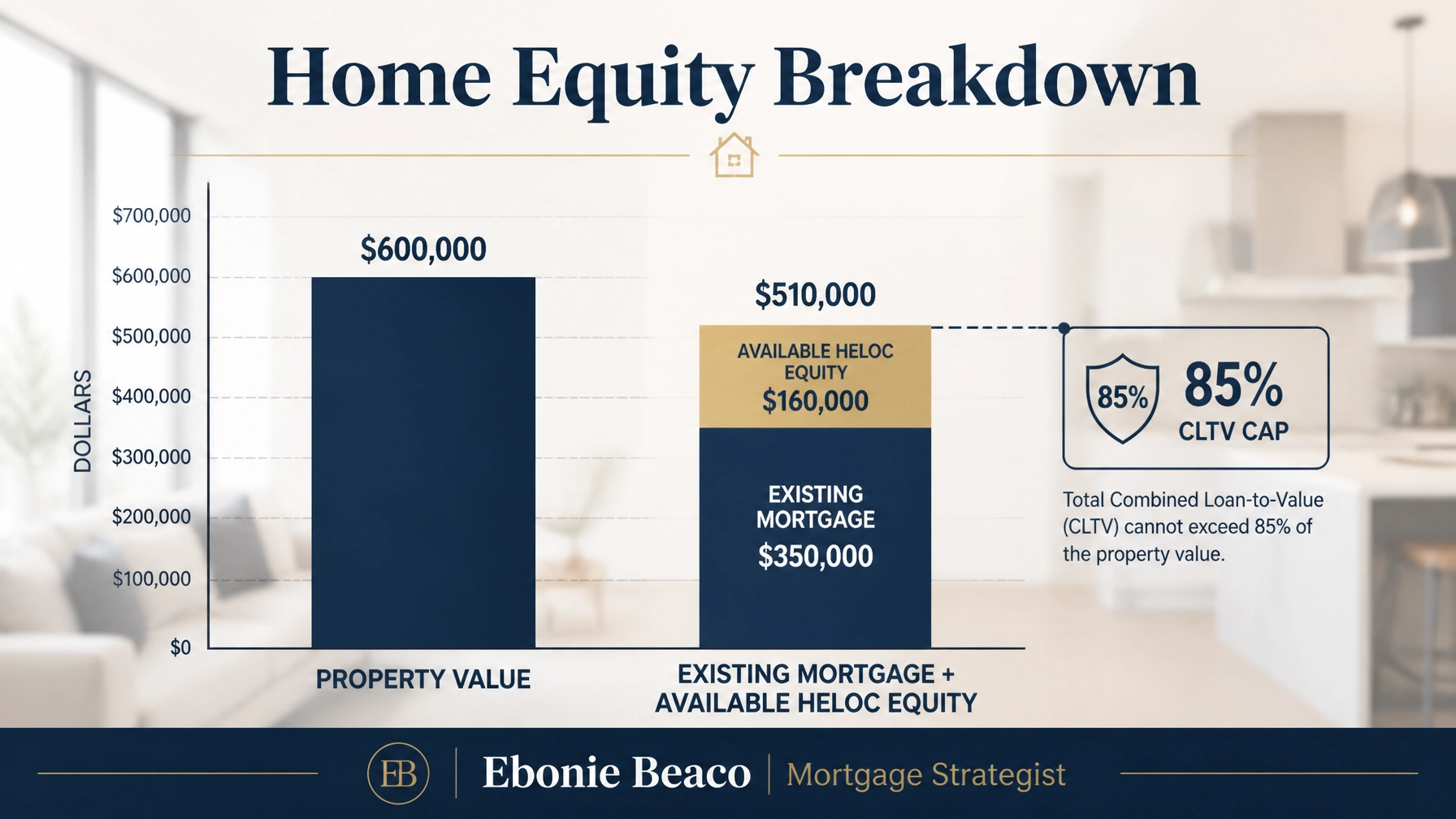

The Math Behind the Money: A Real Scenario

Let's look at how the numbers actually work in a real-world situation. Imagine a homeowner in Richmond, Virginia, who bought their home a few years back.

- Current Property Value: $600,000

- Existing Mortgage Balance: $350,000

- Max Combined Loan-to-Value (CLTV): 85%

To find the maximum debt allowed, we multiply the value by the CLTV cap:

$600,000 x 0.85 = $510,000 (Total Allowable Debt)

Now, we subtract the existing mortgage:

$510,000 - $350,000 = $160,000 (Available HELOC Amount)

In this scenario, the homeowner has $160,000 available to use. If they take out $50,000 of that to put a 25% down payment on a $200,000 rental property in Michigan, they have successfully moved equity from a "lazy" asset into a "productive" one.

Tapping Equity Across the Board: From Florida to Illinois

While Virginia and Michigan are in the spotlight today, we provide mortgage solutions across several states including Alabama, Arkansas, California, Florida, Georgia, Illinois, Indiana, Kentucky, Missouri, and Virginia.

In Florida, homeowners are dealing with rising insurance costs. Many are using HELOCs to install impact windows or upgrade roofing to lower their premiums. In Chicago, investors are using home equity to fund the "rehab" portion of a BRRRR (Buy, Rehab, Rent, Refinance, Repeat) strategy.

Every state has a different local economy, but the principle of home equity remains universal. If you have the equity, you have options. You can jump in and compare how a HELOC might serve your specific goals, whether you are in a beach house in Florida or a bungalow in Georgia.

How to Secure Your Line with a Local Expert

Getting a HELOC isn't as complicated as a full primary mortgage, but it does require professional guidance. Most lenders will look for a credit score in the high 600s or better and a Debt-to-Income (DTI) ratio that stays within a healthy range.

One secret that many big banks won't tell you is that wholesale mortgage channels often offer much more flexibility. While a retail bank might cap you at 75% LTV, a mortgage strategist can often find programs that go up to 85% or even 90% in some cases.

We also look at alternative documentation for self-employed borrowers. If your tax returns don't show the full picture of your success, we can explore bank statement options to qualify you for the equity you deserve.

The Final Verdict: Is It Time to Leverage?

The decision to tap your home equity should be based on your long-term goals. If you are using the money to buy an asset that appreciates or to eliminate debt that costs you 20% in interest, a HELOC is one of the smartest moves you can make.

Don't let your equity sit idle while life gets more expensive. Access the tools used by savvy investors and wealthy homeowners to stay ahead. We are here to guide you through every step of the process with transparency and clear communication.

Whether you are in Richmond, Detroit, Atlanta, or Chicago, your home is more than just a roof: it is your greatest financial lever.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664