Why Everyone Is Talking About Tonight’s Mortgage Rate Trends (And You Should Too)

As the sun sets on Thursday, May 21, 2026, the real estate community is buzzing with the latest shifts in the credit markets. Keeping a steady pulse on mortgage movements is a primary requirement for any homeowner or investor looking to secure a financial advantage. Today’s data suggests a market that is navigating a complex web of geopolitical headlines, inflation reports, and central bank policy. For those holding property in states like Illinois, Florida, or California, understanding these daily fluctuations provides the clarity needed to make move-time decisions.

The current environment demands a higher level of strategic thinking than we have seen in previous years. We are witnessing a unique intersection where high property values meet persistent borrowing costs, creating a landscape that rewards the well-informed. Whether you are managing a single-family home in Virginia or a multi-unit portfolio in Michigan, the numbers released tonight tell a story of resilience and careful calculation. Explore the details below to see how these trends influence your specific real estate goals.

The Current State of Mortgage Rates in May 2026

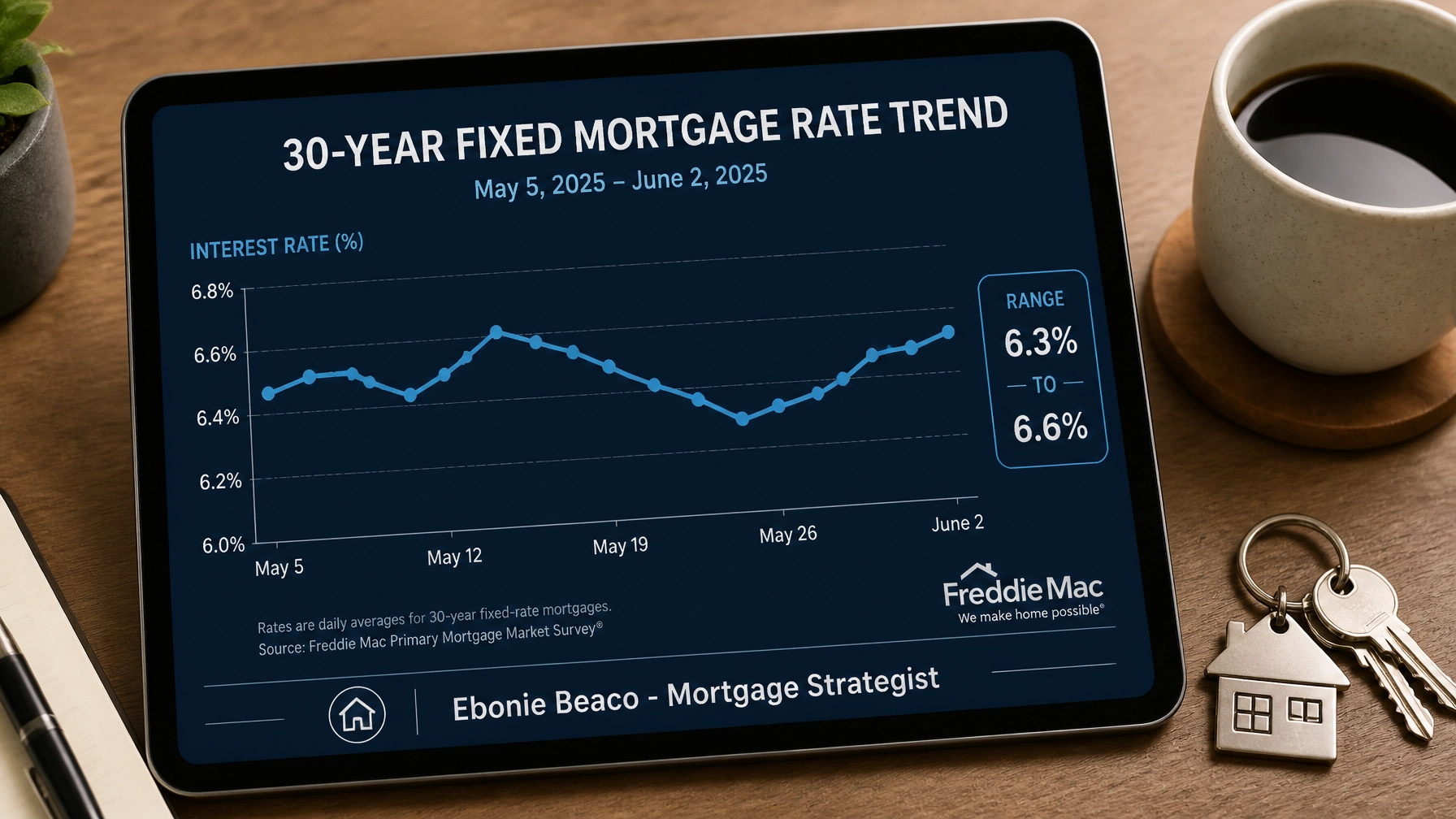

Tonight’s market reports show that 30-year fixed-rate mortgages are currently hovering within the 6.37% to 6.60% range. This placement follows a slight upward bias throughout the week as investors react to the latest economic indicators. While some experts anticipated a more aggressive dip, the reality remains a range-bound environment that requires patience. Homebuyers and investors should note that even small fractional changes can significantly alter the long-term cost of a loan.

National Average Breakdowns

Tonight's averages across various loan programs provide a clear benchmark for your next transaction.

- 30-Year Fixed Conforming: Currently averaging approximately 6.45%.

- 15-Year Fixed Conforming: Sitting lower at roughly 5.74%.

- 30-Year FHA Loans: Averaging 6.14% for qualified borrowers.

- 30-Year VA Loans: Holding steady at 5.95% for those with military eligibility.

Defining Key Financial Concepts for Today's Market

To navigate the lending landscape successfully, you must understand the technical definitions that lenders use to evaluate your files. These terms represent the foundation of your borrowing power and your ability to scale a real estate portfolio.

DSCR: Debt Service Coverage Ratio

Definition: A financial metric used by lenders to measure a property's ability to cover its own debt payments based on its gross rental income.

Application: Investors use DSCR loans to qualify for financing without needing to provide personal income tax returns, as the property’s cash flow serves as the primary qualifier.

HELOC: Home Equity Line of Credit

Definition: A revolving line of credit that allows homeowners to borrow against the equity in their primary or investment properties.

Application: You can use a HELOC to fund a renovation, pay for a down payment on a new property, or maintain a liquid cash reserve for investment opportunities.

Non-QM: Non-Qualified Mortgage

Definition: A category of loan programs designed for borrowers who do not meet the strict documentation standards of traditional conforming loans.

Application: Self-employed individuals and entrepreneurs often jump in to use Non-QM solutions to qualify using bank statements rather than tax returns.

What Is Driving the Interest Rate Volatility?

Understanding the "why" behind the numbers is just as significant as the numbers themselves. Several macro-economic factors are currently tugging at the bond market, which in turn influences what you see on your mortgage quote.

The Federal Reserve and Inflation

The Federal Reserve held the federal funds rate steady at its most recent meeting, keeping it in the 3.50% to 3.75% range. While the central bank is not raising rates further, it has not yet signaled a pivot toward significant cuts. This is because inflation data remains slightly above the preferred 2% target, causing the 10-year Treasury yield to stay elevated. As the 10-year yield moves, mortgage rates typically follow in tandem.

Geopolitical Influence and Global Sentiment

External events, such as the ongoing developments in the Middle East and fluctuating energy prices, play a massive role in market sentiment. Recent ceasefire talks have provided some moments of relief for the bond market, but any breakdown in these negotiations typically leads to a "flight to safety" in bonds, which can cause rates to fluctuate. For real estate professionals in markets like Georgia and Alabama, these global headlines are now part of the daily checklist for timing a lock.

Regional Market Activity and Strategy

The impact of these rate trends varies significantly depending on your location and your specific investment strategy. We are seeing distinct patterns emerge in the states we serve.

Illinois and the Midwest Focus

In Chicago and surrounding suburbs, the demand for affordable housing remains high despite the mid-6% interest rates. Investors are increasingly looking toward landlord loans for multi-unit buildings where the rental income can offset the higher borrowing costs. Conventional purchase activity in Indiana and Michigan has actually shown a modest increase, suggesting that buyers are adjusting their expectations and moving forward with their lives.

Florida and the Southeast Corridor

The Florida market continues to see robust activity, particularly in the short-term rental and Airbnb space. Investors in cities like Orlando and Tampa are utilizing cash-out refinance strategies to tap into the massive equity growth seen over the last few years. If you own property in Florida with significant equity, extracting that capital now to fund your next acquisition could be a powerful move.

California and Virginia Suburban Growth

Higher-priced markets in California and Virginia are seeing a rise in the use of Adjustable-Rate Mortgages (ARMs). Currently, ARMs represent about 8.3% of all applications. This strategy allows borrowers to secure a lower initial rate for the first 5 to 10 years, with the plan to refinance if rates drop toward the end of 2026 or into 2027.

Practical Financial Examples for Homeowners and Investors

Let’s look at how these strategies function in the real world with concrete numbers. These examples reflect the types of scenarios we analyze daily for our clients.

Example 1: The Cash-Out Refinance Strategy

Imagine a homeowner in Atlanta, Georgia, who owns a home valued at $600,000 with an existing mortgage balance of $300,000.

- Property Value: $600,000

- Max Loan-to-Value (80%): $480,000

- Existing Balance: $300,000

- Available Cash: $180,000 (minus closing costs)

By executing a cash-out refinance, this homeowner can access $180,000 to purchase a rental property in Arkansas or fund a major renovation that increases the primary home's value even further.

Example 2: The DSCR Rental Property Calculation

An investor is looking at a four-unit building in St. Louis, Missouri, priced at $500,000.

- Purchase Price: $500,000

- Down Payment (20%): $100,000

- Loan Amount: $400,000

- Monthly PITI (Principal, Interest, Taxes, Insurance): $2,950

- Total Monthly Rental Income: $3,600

- DSCR Calculation: $3,600 / $2,950 = 1.22

Because the DSCR is above 1.0, many lenders would approve this loan based on the property’s performance alone, regardless of the investor's personal income.

Looking Ahead: The Forecast for Late 2026

Many industry analysts, including those from Fannie Mae, expect a gradual cooling of rates as we move deeper into the year. Some projections suggest that we could see averages move below the 6% threshold by the end of 2026 if inflation continues its orderly retreat. However, for most of the summer, the consensus is that we will stay in the "mid-6s" range.

Waiting for the perfect rate is often a losing strategy in a rising-price environment. If you find a property that fits your investment criteria today, the financing is simply a tool to acquire the asset. You can always refinance later when the market shifts. Compare your options and look at the total cost of ownership rather than focusing solely on the interest rate.

Quick Tips for Navigating Rates Tonight

- Check your credit score: Even a 20-point difference can move you into a different pricing tier.

- Look at the 15-year option: If you can afford the higher monthly payment, you will save thousands in interest.

- Consider a rate lock: If you are within 30 days of closing, locking today protects you from sudden volatility.

- Explore different lenders: Different institutions have different appetites for risk, which affects their daily pricing.

Final Thoughts on Today's Market

The mortgage world does not stand still, and neither should your strategy. The information released tonight provides a snapshot of a market in transition. By staying educated on mortgage basics and keeping an eye on the bigger picture, you position yourself to win in any environment.

Whether you are a first-time homebuyer in Kentucky, a seasoned landlord in Missouri, or a realtor structuring deals in Virginia, the financing you choose is the engine that drives your real estate success. Jump in, ask the tough questions, and ensure your financing is aligned with your long-term wealth-building goals.

For more detailed market updates, you can refer to the latest analysis from Fortune and Norada Real Estate.

Resolve your uncertainty by exploring your options today.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664