Why Everyone Is Talking About Today’s Rate Volatility (And You Should Too)

Navigating the mortgage market in May 2026 requires a firm grasp of how global economic shifts translate into local housing trends. Current headlines are dominated by a persistent choppiness in the 30-year fixed mortgage rate, which has settled into a high 6% range following several months of unpredictable swings.

Volatility: A financial term describing the frequency and magnitude of price movements for a specific security or market index over a set period. In the mortgage world, high volatility often means that the interest rate you see in the morning could shift significantly by the time you are ready to lock your loan in the afternoon.

Investors and homeowners across Alabama, Florida, and Virginia are watching these numbers closely as they plan their next move. Understanding the drivers behind these shifts allows you to position your portfolio or your primary residence for long-term financial health regardless of daily market noise.

Explore the current landscape of mortgage loan programs to see how modern financing adapts to these rapid market changes.

The Economic Drivers Behind the May 2026 Shift

The primary engine behind today's rate environment is the interplay between inflation data and the 10-Year Treasury yield. In the first few weeks of May, the 30-year fixed rate spiked toward 6.51% before easing slightly to 6.46%, creating a "sawtooth" pattern on financial charts.

CPI (Consumer Price Index): A measure that examines the weighted average of prices of a basket of consumer goods and services, used to track inflation trends. When CPI reports show "sticky" or rising inflation, the bond market typically reacts by pushing yields higher, which directly increases mortgage rates.

Global instability, specifically concerning energy supply routes in the Middle East, has added upward pressure on crude oil prices this month. This geopolitical friction contributes to higher domestic transportation and production costs, which the Federal Reserve monitors when determining the future path of interest rates.

While the Fed has maintained the federal funds rate between 3.50% and 3.75%, the market is already pricing in expectations for the remainder of the year. According to Freddie Mac, the hope for a return to the 5% range in 2026 is becoming less likely as economic indicators remain robust.

Regional Snapshots: Alabama to California

Volatility does not impact every region in the same way, as local inventory levels and migration patterns often dictate how sensitive a market is to rate spikes. In California and Virginia, high equity levels have allowed many sellers to remain active, as they can use large down payments to mitigate the impact of higher monthly costs.

DTI (Debt-to-Income Ratio): The percentage of a borrower's monthly gross income that goes toward paying monthly debt payments, including the proposed mortgage. In high-cost markets like Los Angeles or Arlington, managing your DTI becomes more challenging as rates rise, often requiring alternative financing solutions.

Conversely, states like Alabama, Arkansas, and Missouri continue to see strong demand from investors seeking "Blended Rate" strategies. These lower-entry-point markets allow for portfolio expansion even when the cost of capital is higher than it was during the historic lows of the early 2020s.

In the Midwest, Illinois, Indiana, and Michigan are benefiting from stable local economies and a surge in mid-term rental interest. Cities like Chicago and Indianapolis remain attractive because they offer a balance between property appreciation and consistent rental yields for long-term landlords.

Strategy for Homeowners: The Refinance vs. HELOC Debate

If you are a homeowner with significant equity, you might be wondering how to access those funds without losing the low interest rate you secured years ago. Many owners in Florida and Georgia currently hold primary mortgages in the 3% to 4% range, making a full cash-out refinance feel like a heavy trade-off.

Cash-Out Refinance: A mortgage transaction where a new loan replaces an existing one for a higher amount, with the difference paid to the borrower in cash. This is a powerful tool for consolidating high-interest credit card debt or funding large-scale renovations when the math makes sense.

Instead of replacing the entire loan, a HELOC allows you to keep your primary low-rate mortgage intact while adding a second-lien revolving credit line. This "Second-Lien Strategy" is often the most cost-effective way to fund investment property down payments or home improvements in a high-rate environment.

HELOC (Home Equity Line of Credit): A revolving line of credit that allows homeowners to borrow against the equity in their home as needed, similar to a credit card but with the property as collateral.

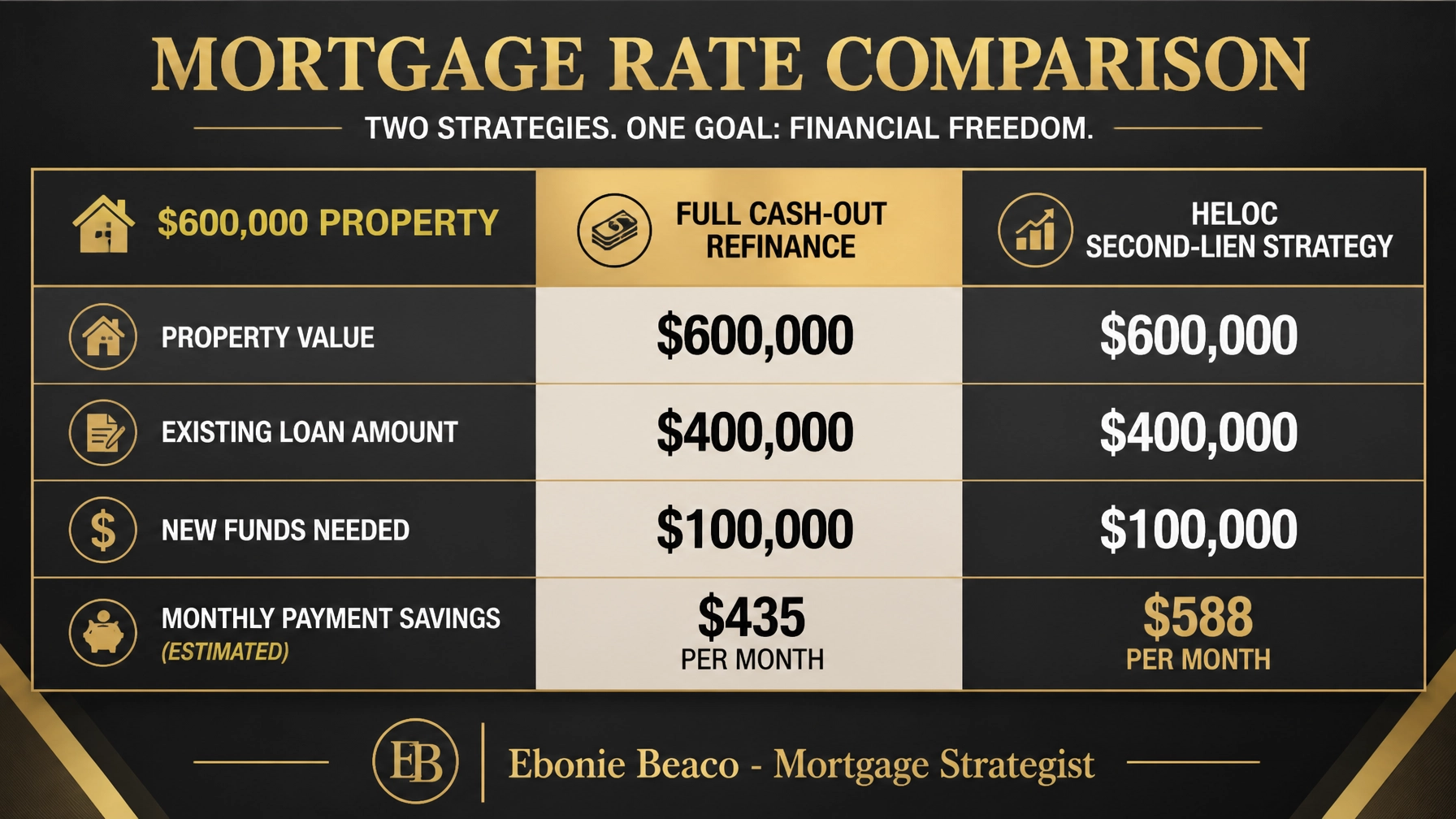

The Real-World Math: Refi vs. HELOC

Consider a homeowner in Illinois with a property valued at $600,000 and an existing mortgage of $300,000 at 3.5%. They want to access $100,000 for a down payment on a rental property in Kentucky.

- Option A: Full Cash-Out Refinance

- New Loan: $400,000 at 6.75%

- Monthly Payment Increase: Approximately $1,247

- Option B: HELOC Strategy

- Primary Loan: Remains $300,000 at 3.5%

- HELOC: $100,000 at 9.0% (Interest-only)

- Combined Increase: Approximately $750

In this scenario, the homeowner saves nearly $497 every month by choosing the HELOC strategy instead of refinancing the entire balance. You can run your own numbers using our mortgage calculators to see which path fits your specific financial profile.

Strategies for Real Estate Investors: DSCR and Non-QM

For investors building a portfolio in Michigan or Arkansas, conventional financing is not the only path forward during periods of volatility. DSCR loans have become a staple for professional landlords because they prioritize the property's performance over the individual's tax returns.

DSCR (Debt Service Coverage Ratio): A financial metric used by lenders to qualify a borrower based on the rental income generated by the property relative to the mortgage payment. A ratio of 1.25 means the property produces 25% more income than the cost of the monthly debt service.

These loans are particularly useful for Airbnb and short-term rental operators in Florida where yields remain high. Since these programs do not require personal income verification, they offer a streamlined loan process that is ideal for quick closings on competitive deals.

Non-QM Mortgage: A category of loans designed for borrowers who do not meet the strict criteria of government-backed entities like Fannie Mae or Freddie Mac. This includes bank statement loans for self-employed entrepreneurs and asset-depletion loans for retirees.

Investors looking to scale quickly in Georgia or Alabama often utilize bridge loans or fix-and-flip financing to acquire distressed assets. These short-term solutions provide the capital needed to renovate a property, which increases the ARV (After Repair Value) and allows for a permanent refinance once the work is complete.

Why Waiting for Lower Rates Might Be Costly

A common mistake in a volatile market is waiting for rates to return to "normal" levels before taking action. While the 30-year fixed rate is higher than it was in 2021, home values in most metropolitan areas in Virginia, Illinois, and California continue to appreciate due to low inventory.

PMI (Private Mortgage Insurance): An insurance policy required for conventional loans when the down payment is less than 20% of the purchase price. While PMI is an added cost, the equity gained through home price appreciation often far outweighs the expense of the insurance premiums over time.

By waiting for a 1% drop in rates, a buyer might find that the price of the home they want has increased by 5% or 10%. In many cases, it is more advantageous to secure the property now and refinance later if rates decline, rather than missing out on the equity growth that occurs in the meantime.

Strategic borrowers are also looking at Adjustable-Rate Mortgages (ARMs), which currently account for about 8.3% of new applications. An ARM can provide a lower initial payment for the first 5 or 7 years, giving the homeowner a "bridge" to a future lower-rate environment without the immediate burden of high fixed costs.

Jump in and review our current VA loan options or conventional loan guides to find the right fit for your purchase or refinance goals.

Navigating the Path Forward

The mortgage market of May 2026 is defined by rapid movement and strategic complexity, but these conditions also create unique opportunities. Whether you are a first-time buyer in Missouri or a seasoned investor in Florida, the key is to focus on the numbers that move you closer to your goals.

Compare your options and look beyond the headline interest rate to find the structure that maximizes your cash flow and equity access. Our team specializes in breaking down these complex scenarios for borrowers across the country, ensuring you have the clarity needed to act with confidence.

Access our latest market insights and professional guidance to stay ahead of the curve.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664