Why Everyone Is Talking About This Week’s Rate Forecast (And You Should Too)

As we move through the final week of May 2026, the mortgage market is buzzing with a level of anticipation we haven’t seen since the start of the year. Investors, homeowners, and real estate professionals across the country are closely monitoring the latest economic signals to determine where financing costs are headed as we enter the peak summer season. The narrative surrounding interest rates has shifted rapidly this month, moving from a position of cautious optimism to a focused analysis of sticky inflation data and Federal Reserve commentary. Whether you are planning to purchase a primary residence in Chicago or looking to scale a rental portfolio in Florida, understanding these shifts is essential for making informed financial decisions.

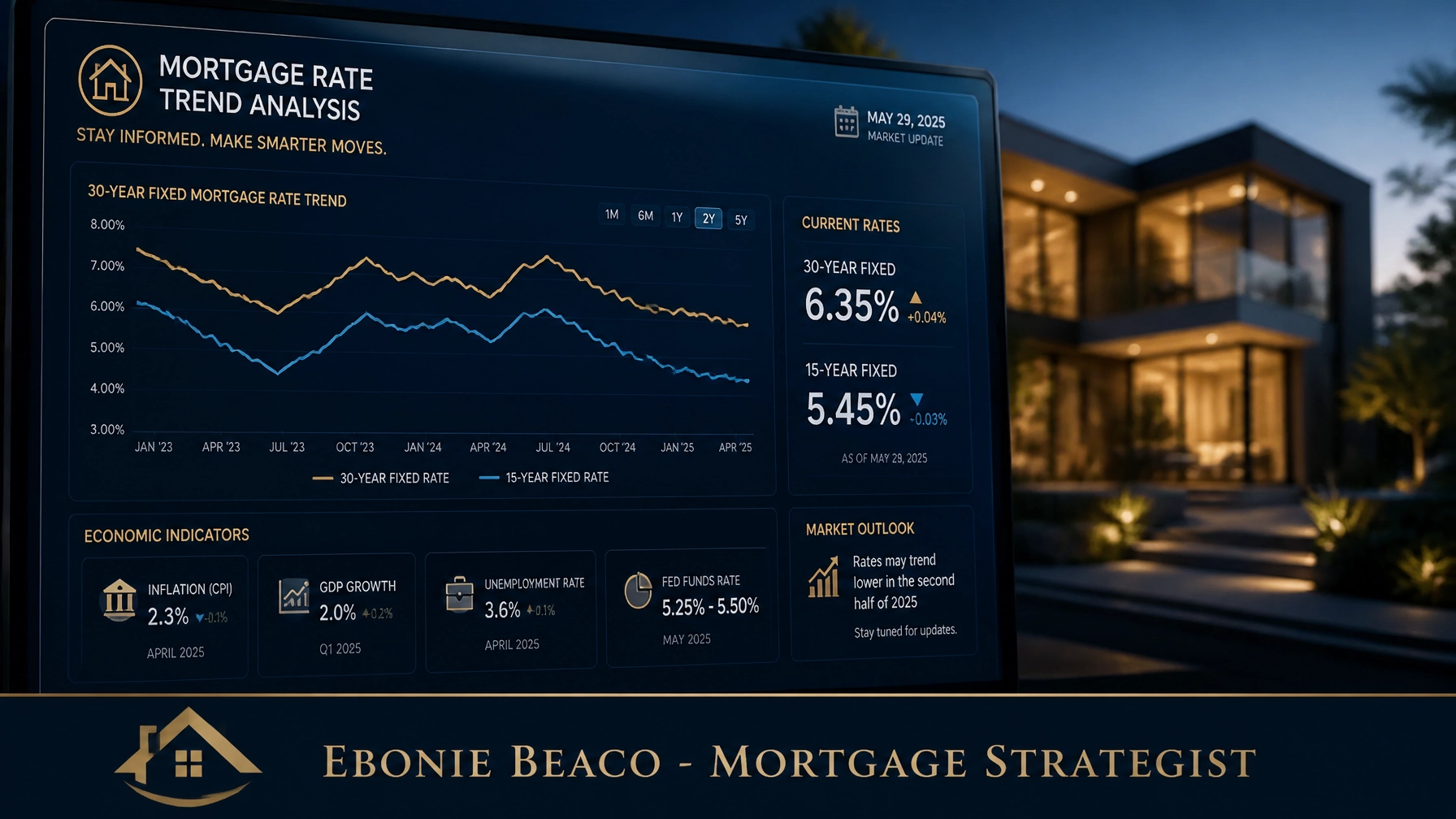

The conversation this week centers on the upcoming release of the Personal Consumption Expenditures (PCE) price index, which remains the primary metric used by policymakers to gauge inflationary pressure. Early indicators suggest that while some cooling has occurred, the road back to long-term stability is proving to be more gradual than many anticipated earlier in the spring. This data directly influences the yield on the 10-year Treasury, which serves as the benchmark for long-term fixed-rate mortgages. When these yields fluctuate, lenders adjust their pricing accordingly, creating a ripple effect that touches every segment of the real estate market from entry-level buyers to institutional investors.

Exploring the nuances of the current forecast allows you to position yourself ahead of the curve rather than reacting to headlines after the fact. In a market where a quarter-point difference in interest rates can translate to tens of thousands of dollars in lifetime interest, being proactive is the most effective way to protect your purchasing power. We are currently seeing a divergence in regional market behavior, where inventory constraints in states like Virginia and Georgia are keeping prices firm even as buyers navigate shifting rate environments. This intersection of high demand and volatile financing costs makes this week’s forecast a critical piece of the puzzle for anyone active in the housing market today.

Defining Key Economic Indicators

Before we dive deeper into the specific forecasts, it is helpful to clarify the technical terms that dominate the current financial landscape. Understanding these definitions provides the context needed to interpret market news with confidence and clarity.

Mortgage Rate Forecast

A mortgage rate forecast is a professional projection of future interest rate movements based on a comprehensive analysis of economic indicators, including inflation reports, employment data, and central bank policy. You can use these forecasts to help determine the optimal timing for a home purchase or a strategic refinance.

Personal Consumption Expenditures (PCE)

The PCE index is a measure of the prices people in the United States pay for goods and services, and it is the Federal Reserve's preferred gauge for tracking inflation trends. Monitoring this data helps you predict potential shifts in the Fed's stance on interest rate cuts or hikes.

Debt Service Coverage Ratio (DSCR)

DSCR is a financial metric used to qualify investment property loans by comparing the property’s annual net operating income to its total annual debt service. This allows investors to secure financing based on the property's performance rather than personal income or debt-to-income ratios.

The Federal Reserve and the Quest for Stability

The Federal Reserve continues to play a central role in the current mortgage rate narrative. Throughout May 2026, central bank officials have emphasized a commitment to data-driven decisions, which has kept the market in a state of constant recalibration. While the hope for multiple rate cuts earlier in the year has moderated, the conversation has now turned toward the sustainability of the current "higher for longer" policy. For homeowners in states like Michigan and Indiana, this means that the window for traditional rate-term refinancing may be narrower than in previous cycles, requiring a more specialized approach to equity management.

Inflation remains the primary hurdle for those wishing to see a significant drop in borrowing costs. Recent reports from the Federal Reserve indicate that while the labor market remains resilient, the cost of housing and services continues to exert upward pressure on the overall economy. This persistent inflation prevents the 10-year Treasury yield from settling into a lower range, which in turn keeps 30-year fixed rates in a state of flux. If the PCE data released this week shows even a slight improvement, we could see a temporary easing of rates that savvy buyers might use to lock in a more favorable loan term.

Investors are also paying close attention to these signals as they calculate their cap rates and projected returns. In markets such as Alabama and Arkansas, where entry prices are relatively lower, even a small shift in interest rates can significantly impact the cash-on-cash return of a rental property. By staying informed about the weekly forecast, you can better time your acquisitions and ensure that your financing strategy aligns with the broader economic environment. Jump in and analyze your current scenarios to see how a slight adjustment in the forecast might change your long-term outlook.

Comparing Equity Access Strategies

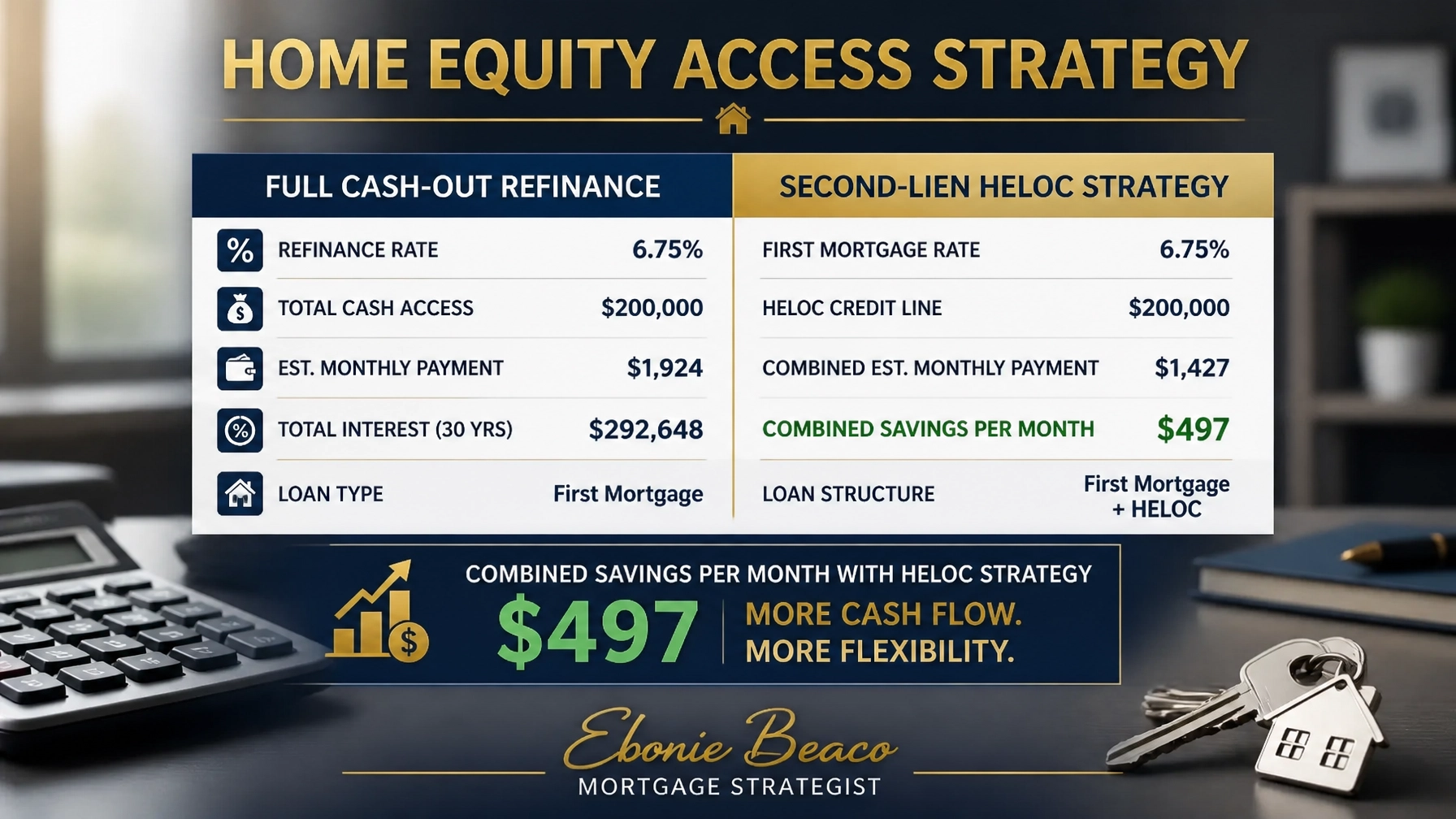

For current homeowners, the most important part of this week's forecast is how it impacts their ability to access the equity they have built over the last several years. With home values remaining strong in many regions, including the metro areas of California and Virginia, homeowners are sitting on record amounts of tappable equity. However, the strategy used to access that equity must be carefully chosen to avoid unnecessarily increasing the cost of existing debt. Many individuals who locked in low rates between 2020 and 2021 are hesitant to pursue a full cash-out refinance, as doing so would mean replacing their entire mortgage with a new, higher interest rate.

A more effective approach in the current environment is often a Second-Lien Strategy, such as a HELOC (Home Equity Line of Credit). This allows you to keep your primary mortgage at its original low rate while borrowing only the specific amount of equity you need at a separate, prevailing market rate. By comparing these two options, you can see exactly how much you might save on a monthly basis.

Consider a scenario where a property is valued at $600,000 with an existing mortgage balance of $300,000 at a 3.5% interest rate. The homeowner wants to access $100,000 for a renovation project or to fund a down payment on a new investment property.

- Full Cash-Out Refinance: Replacing the entire $400,000 debt with a new loan at a 6.75% rate would result in a significant increase in the monthly principal and interest payment.

- HELOC Strategy: Keeping the $300,000 loan at 3.5% and taking out a separate $100,000 HELOC at approximately 9% (interest-only) would result in a total monthly outlay that is roughly $497 lower than the full refinance option.

Investor Strategies for a Volatile Market

Real estate investors are currently navigating one of the most complex financing environments in recent history. The standard conventional loan is not always the best fit for those looking to scale a portfolio or acquire specialized assets like Airbnb and short-term rental financing. In high-demand markets like Florida and the coastal regions of California, investors are increasingly turning to DSCR investor loans to stay competitive. These programs allow you to qualify based on the rental income generated by the property itself, which is particularly beneficial for those who may have high debt-to-income ratios due to multiple existing mortgages.

The current rate forecast also affects the Fix and Flip and Bridge Loan sectors. Investors who rely on short-term financing to renovate and resell properties must be acutely aware of how the cost of capital changes from week to week. A rise in the forecast can squeeze profit margins if the exit strategy relies on a buyer securing a traditional mortgage at a certain rate. Access specialized financing tools that allow for more flexibility, such as Non-QM mortgage loans, which cater to unique borrower profiles including self-employed entrepreneurs and foreign national investors.

In the commercial space, we are seeing strong interest in multi-unit buildings and apartment complexes in cities like Richmond, Virginia, and St. Louis, Missouri. These assets often provide more stability during periods of rate volatility because their value is tied closely to the income they produce rather than just the comparable sales in the neighborhood. By using a DSCR rental property loan or a commercial bridge loan, you can acquire these properties and implement value-add strategies that increase the Net Operating Income (NOI), effectively hedging against the impact of higher interest rates.

Regional Market Activity and Inventory Trends

The impact of the rate forecast is not felt equally across all states. In Illinois and Indiana, we are seeing a steady demand for suburban single-family homes, but low inventory levels continue to push prices higher. According to recent reports from Freddie Mac, the "rate lock-in" effect is still preventing many homeowners from listing their properties, as they do not want to trade their current low rates for the rates available in today’s market. This has created a unique opportunity for new construction and fix-and-flip financing to fill the gap in the housing supply.

In Florida and Georgia, the market remains resilient due to strong population growth and a robust job market. Even as the forecast suggests rates may stay elevated, buyers are finding ways to make deals work through down payment assistance programs and creative financing. For those looking to enter these markets, the key is to have a clear understanding of your budget and to be prepared to act quickly when the right property becomes available. Exploring options like ITIN mortgage loans or bank statement loans can also open doors for borrowers who do not fit the traditional W-2 employee mold but have the financial strength to support a mortgage.

Specialized Solutions for the Self-Employed

Self-employed borrowers often face unique challenges when interest rates are in the spotlight. Traditional lenders typically require two years of tax returns, which may not accurately reflect the current cash flow of a successful business owner or entrepreneur. This is where bank statement loans become an invaluable tool. By using 12 to 24 months of bank statements to verify income, you can qualify for a mortgage that reflects your true earning potential, regardless of what the general rate forecast might suggest for the average consumer.

Refinancing for the self-employed also requires a strategic look at the overall financial picture. If you are looking to consolidate high-interest business debt or fund a new venture, a cash-out refinance or a HELOC could be a powerful move. The goal is to align your financing with your long-term wealth-building objectives, ensuring that every dollar of equity is working as hard as possible for you. Compare your current loan terms with the options available through our 240+ lenders to find the perfect fit for your situation.

Taking Control of Your Financial Future

The mortgage market will always be subject to the ebbs and flows of the global economy, but you do not have to be a passive observer. By staying engaged with the weekly rate forecast and understanding the specific loan programs available to you, you can move forward with confidence. Whether you are a first-time homebuyer in Alabama, a seasoned landlord in Virginia, or a self-employed professional in California, there is a financing strategy designed to help you achieve your goals.

Don’t let the noise of the headlines distract you from the opportunities that exist in today’s market. The best time to review your strategy is before the next major economic shift occurs. We are here to help you navigate the complexities of the loan process and provide the guidance you need to succeed.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664