Why Everyone Is Talking About This Week’s Mortgage Rate Volatility (And You Should Too)

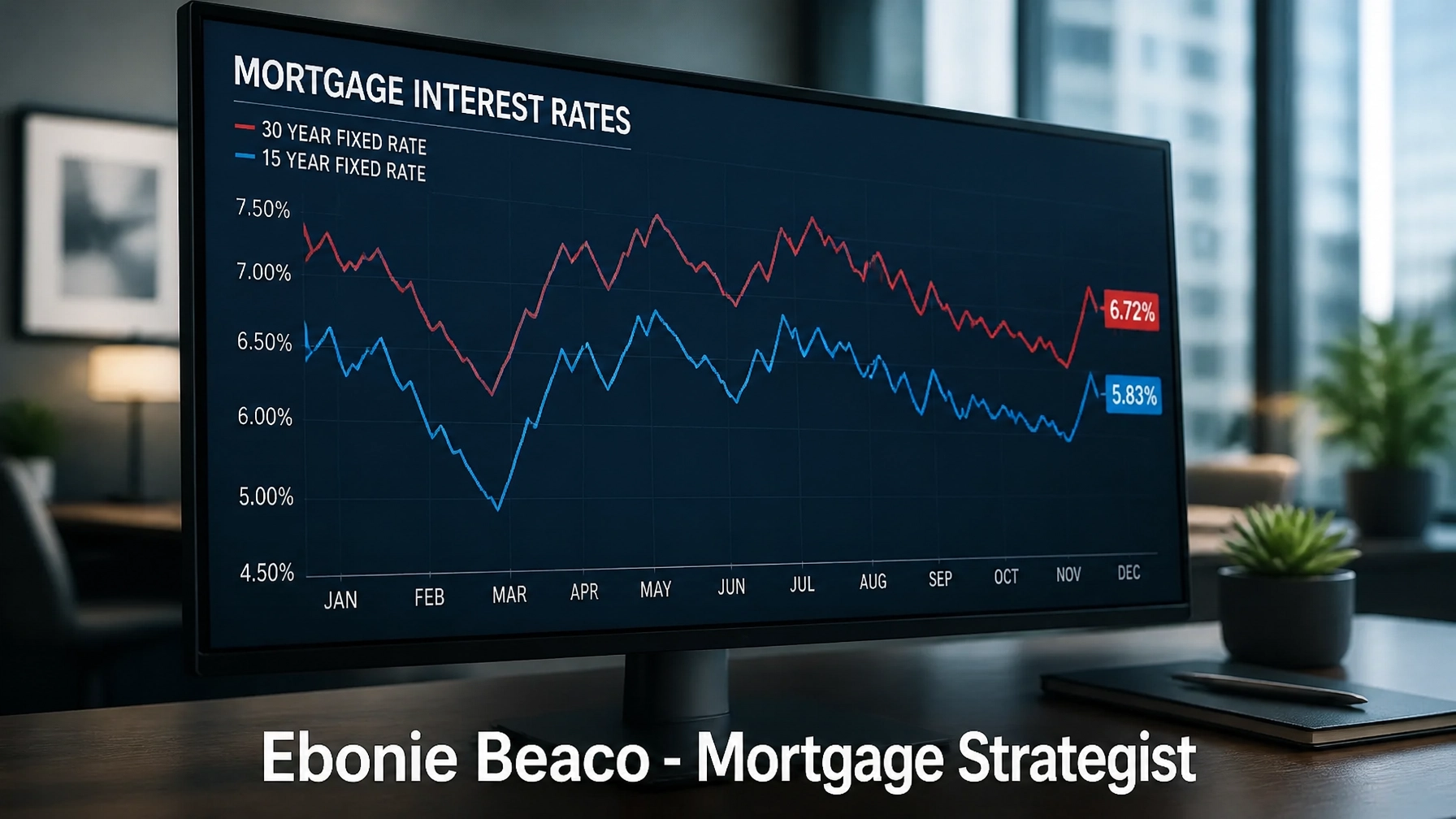

The mortgage market has reached a critical juncture this week, sparking intense discussions among economists, real estate investors, and prospective homebuyers alike. As we wrap up the final days of May 2026, the landscape of residential and commercial financing is shifting beneath our feet, driven by a complex interplay of inflation reports and Federal Reserve sentiment. For those tracking property values in Illinois, Florida, or California, the sudden movement in the 30 year fixed rate has become the primary topic of conversation. Understanding these shifts is essential for anyone looking to secure a loan or manage an existing real estate portfolio.

Recent data indicates that the 30 year fixed mortgage rate has been hovering in a narrow but choppy range, frequently dipping just below the 7% mark before bouncing back. This volatility is largely attributed to the latest Consumer Price Index (CPI) readings, which suggest that inflation is cooling but remains stubbornly above the target. Investors in states like Georgia and Virginia are watching these numbers closely, as they directly influence the secondary market for Mortgage Backed Securities (MBS). When inflation shows signs of persistence, bond yields tend to rise, which in turn pushes mortgage rates higher for the average borrower.

Decoding the Spread: Treasury Yields and Mortgage Rates

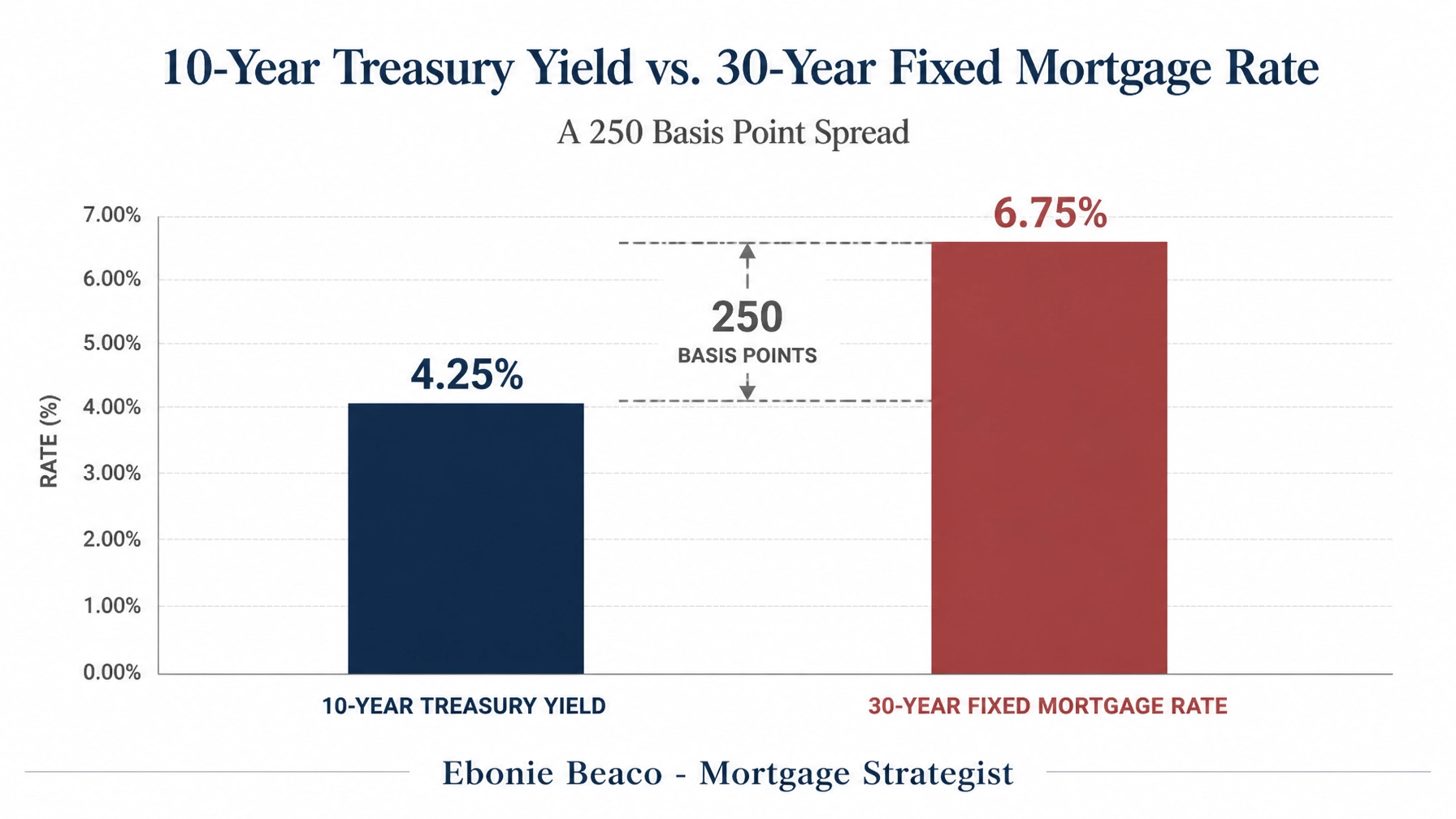

To understand why rates move the way they do, we must look at the relationship between the 10 year Treasury yield and residential interest rates. Historically, the gap between these two figures averages around 170 to 200 basis points, yet recently we have seen this spread widen to approximately 250 basis points. This wider spread represents a form of market "risk premium" where lenders account for uncertainty in the future of the economy. For a strategist, this spread is a key indicator of where rates might head if the market achieves more stability.

Explore the nuances of this relationship:

- Treasury Yield: The return on investment for U.S. government debt, which serves as a benchmark for long term interest rates.

- Basis Point: A unit of measure equal to one one-hundredth of a percentage point (0.01%).

- MBS Spread: The difference in yield between a mortgage backed security and a comparable Treasury bond.

Accessing this information helps you understand why your quoted rate might change from Monday to Friday, even if the Federal Reserve has not made a formal announcement. The market reacts in real time to every piece of economic data, from employment numbers to retail sales figures. In competitive markets like Chicago or Miami, being aware of these daily fluctuations can save a borrower thousands of dollars over the life of a loan.

The Regional Impact: From the Midwest to the Gulf Coast

The impact of rate volatility is not uniform across the country, as local inventory levels and buyer demand create unique challenges in different states. In Alabama and Arkansas, where home prices remain relatively more affordable compared to the national average, even a small dip in rates can significantly expand the pool of qualified buyers. Conversely, in high cost areas like California or Northern Virginia, a quarter point increase in interest rates can dramatically alter a buyer's debt to income (DTI) ratio. Real estate professionals in these regions are increasingly relying on creative financing solutions to help their clients navigate these hurdles.

In Florida, the combination of high insurance costs and interest rate volatility has led many investors to pivot toward specialized loan products. We are seeing a surge in interest for Non-QM Mortgage Loans and bank statement loans for self employed entrepreneurs who may not fit the traditional W-2 box. These programs offer flexibility that is often necessary when the conventional market becomes too restrictive due to rate hikes. Meanwhile, in the Indiana and Michigan markets, the focus remains on inventory management and finding value in emerging suburban neighborhoods.

Investment Strategies in a Volatile Market

For the seasoned real estate investor, volatility is not just a challenge; it is an opportunity to restructure and refine. Many landlords are moving away from traditional financing and exploring DSCR Investor Loans (Debt Service Coverage Ratio loans). These loans prioritize the property's ability to generate rental income over the borrower's personal income, making them ideal for scaling a portfolio quickly. If you are operating an Airbnb in a tourist heavy area of Florida or Georgia, a DSCR loan can be a powerful tool for acquisition without the hurdles of a standard mortgage application.

Jump in and compare these investor focused options:

- DSCR Loans: Financing based on the property's cash flow rather than personal tax returns.

- Fix and Flip Loans: Short term funding used for purchasing and renovating distressed properties for a quick resale.

- Bridge Loans: Temporary financing that "bridges" the gap between the purchase of a new property and the sale of an existing one.

According to the Mortgage Bankers Association (MBA), investor activity remains a significant driver of the housing market, particularly in the multi unit and commercial sectors. Whether you are looking at a duplex in St. Louis or a mixed use building in Richmond, understanding how to leverage these specialized products is vital. You can view our full range of loan programs to see which fits your specific investment goal.

Homeowner Equity: Accessing Your Hidden Wealth

Despite the conversation surrounding high rates, many homeowners are sitting on record amounts of equity. If you purchased your home several years ago in a market like Chicago or Atlanta, your property value has likely appreciated significantly. This equity can be accessed through a HELOC (Home Equity Line of Credit) or a Cash-Out Refinance to fund home improvements, consolidate high interest debt, or even provide the down payment for a new investment property.

Consider this real world scenario for a homeowner in a growing suburb:

- Current Home Value: $750,000

- Existing Mortgage Balance: $400,000

- Lender's Max Loan-to-Value (80% LTV): $600,000

- Total Available Equity for Extraction: $200,000

In this example, the homeowner could potentially access $200,000 to renovate their property, which in turn increases the home's value further. This strategy is frequently used by "buy and hold" investors who use a cash out refinance to pull capital from one property to fund the purchase of the next. It is a proven method for building wealth through real estate, even when the broader market feels uncertain. You can use our mortgage calculators to run your own numbers and see how much equity you might be able to unlock.

Looking Ahead: The Path to Stability

The Federal Reserve has signaled that it will remain data dependent throughout the remainder of 2026. This means that every major economic report will likely trigger a reaction in the mortgage market. While the era of 3% interest rates may be behind us, the current environment of 6% to 7% rates is historically normal. The key is to avoid waiting for the "perfect" moment, as timing the market is notoriously difficult. Instead, focus on the fundamentals of the deal and the long term benefits of property ownership.

Recent reports from Freddie Mac suggest that while rates are higher than they were two years ago, the demand for housing remains robust. People still need places to live, and investors still need places to put their capital. By staying informed and working with a strategist who understands the nuances of the current volatility, you can make decisions with confidence. Whether you are a first time homebuyer in Virginia or a veteran investor in California, the right financing structure is out there.

Expert Tools for Your Real Estate Journey

Navigating this market requires more than just a basic understanding of interest rates. It requires the right tools to analyze deals, calculate ROI, and compare different loan scenarios. From BRRRR analysis (Buy, Rehab, Rent, Refinance, Repeat) to fix and flip profit projections, having access to professional grade calculators is a game changer. We provide these resources to ensure that our clients in Missouri, Kentucky, and beyond are equipped to succeed.

Explore our specialized analysis tools:

- Deal Analyzer: A comprehensive tool for evaluating the profitability of a potential real estate acquisition.

- Cap Rate Calculator: Helps you determine the capitalization rate of an income producing property.

- Refinance Break-Even: Calculates how long it will take for the savings from a new rate to outweigh the closing costs.

If you are feeling overwhelmed by the recent headlines, remember that volatility often precedes opportunity. By staying grounded in the data and focusing on your long term financial goals, you can navigate this week's market movements with ease. We are here to provide clear guidance and support as you explore your options in this dynamic real estate environment.

Are you ready to see how this week’s rate changes impact your purchasing power or investment strategy?

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664