Why Everyone Is Talking About This Morning's Fed Report (And What It Means for Florida and Chicago Real Estate)

The financial world woke up to a significant update this morning as the Federal Reserve released its latest findings on the state of the American economy. As of Wednesday, June 3, 2026, the central bank has provided a clear signal regarding its trajectory for interest rates and inflation management through the remainder of the year. For homeowners in Florida, real estate investors in Chicago, and realtors across the Southeast and Midwest, these updates serve as a critical compass for navigating the current housing market. Understanding the nuances of this report is essential for anyone looking to optimize their property portfolio or secure a new home loan in a changing economic landscape.

The Federal Reserve's current stance remains one of cautious optimism, characterized by a commitment to maintaining stability while monitoring persistent price pressures. While the headline numbers suggest that the economy continues to expand at a moderate pace, the internal data reveals a complex interplay between employment levels and consumer spending. This delicate balance directly influences the cost of borrowing, affecting everything from home purchase financing to sophisticated commercial real estate loans. As we analyze the details, it becomes apparent that the "higher for longer" narrative is evolving into a strategy focused on precision rather than broad-stroke adjustments.

Deciphering the June 2026 Federal Reserve Stance

This morning’s report indicates that the Federal Open Market Committee (FOMC) is satisfied with the progress made toward its long-term inflation goals, yet it remains vigilant against potential shocks. The committee has opted to maintain the federal funds rate within a restrictive range to ensure that inflation continues its descent toward the target level. For the mortgage market, this decision provides a level of predictability that has been absent in previous cycles, allowing lenders to price conventional loans and specialized products with greater confidence. Investors should note that while immediate rate cuts were not announced, the rhetoric suggests a softening of the hawkish stance seen earlier this year.

The persistence of a "restrictive" policy means that the cost of capital remains elevated compared to historical lows, but the stability of these rates is encouraging for market participants. When the Fed holds rates steady, it often leads to a narrowing of the spread between the 10-year Treasury yield and 30-year mortgage rates. This environment creates a unique window for those researching home refinance options to potentially lower their monthly obligations if they secured financing during recent peak volatility. By keeping a close eye on the Fed’s balance sheet reduction, or quantitative tightening, we can better project how liquidity will flow into the mortgage-backed securities market.

Defining Key Economic Indicators

To fully grasp the implications of today's report, it is helpful to define the technical terms that drive these institutional decisions. These concepts are the foundation of modern real estate financing strategies and dictate the availability of capital for all borrower types.

- Personal Consumption Expenditures (PCE): This is the Federal Reserve's preferred measure of inflation, tracking the prices paid by consumers for goods and services. Explore how a declining PCE index often leads to downward pressure on mortgage rates, benefiting both buyers and those seeking a cash-out refinance.

- Federal Open Market Committee (FOMC): The branch of the Federal Reserve System responsible for direction of monetary policy. Jump in and analyze their meeting minutes to understand the consensus on future interest rate hikes or cuts.

- Quantitative Tightening (QT): A monetary policy used by central banks to decrease the amount of liquidity in the economy by reducing their balance sheets. Compare the effects of QT on long-term bond yields, which often serve as the benchmark for jumbo loans and commercial debt.

Florida’s Real Estate Resilience Amidst Restrictive Policy

Florida continues to stand out as a powerhouse in the national housing market, driven by robust migration patterns and a thriving tourism sector. This morning’s Fed report is particularly relevant for the Sunshine State, where Airbnb and short-term rental financing remains in high demand. Even with restrictive interest rates, the demand for primary residences and vacation properties in cities like Miami, Orlando, and Tampa remains high. The Federal Reserve's commitment to a stable economic environment supports continued investment in these high-growth regions, as it reduces the risk of sudden market corrections that can deter large-scale developers and individual landlords.

Real estate investors in Florida are increasingly turning to DSCR rental property loans to expand their portfolios without the stringent income verification required by traditional lending. Because these loans focus on the cash flow of the property itself, the Fed's success in stabilizing inflation helps investors project future rental income with greater accuracy. Furthermore, as the Florida market matures, many homeowners find themselves sitting on significant amounts of equity. Accessing this wealth through HELOC loans or a cash-out refinance has become a popular strategy for funding property renovations or making down payments on additional investment units.

Leveraging Home Equity in the Sunshine State

The recent appreciation in Florida property values has created a surge in available home equity for long-term residents and recent buyers alike. A cash-out refinance allows you to replace your existing mortgage with a new one for a larger amount, taking the difference in cash to use for strategic investments. This is often an effective way to secure capital for a fix and flip loan or to bridge the gap during a construction project. For example, consider a homeowner in a high-demand coastal market who has seen their property value climb significantly over the last three years.

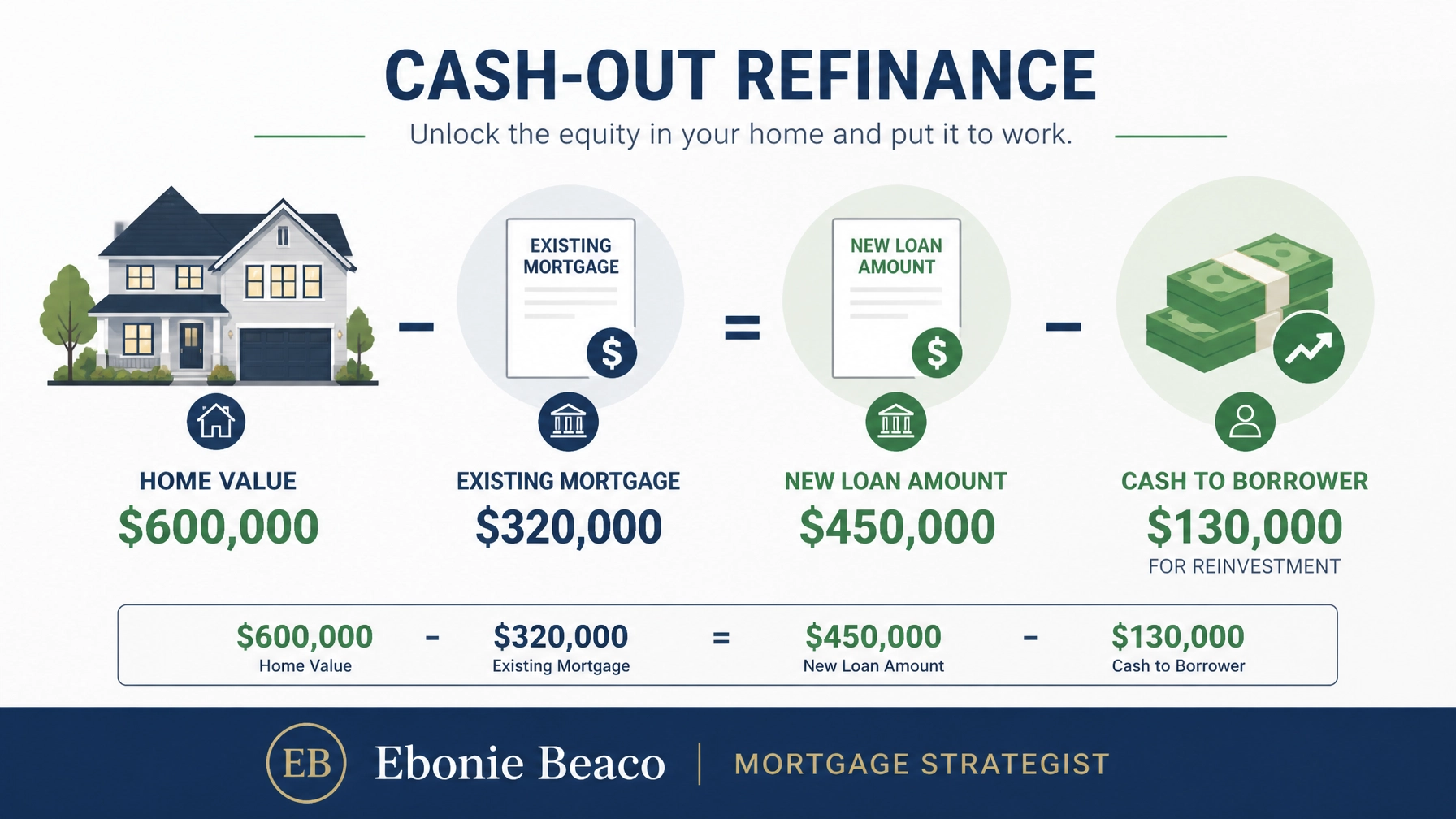

Financial Example: Florida Cash-Out Refinance

Imagine you own a property in Florida valued at $600,000 with an existing mortgage balance of $320,000. By utilizing a cash-out refinance at a 75% Loan-to-Value (LTV) ratio, you could potentially secure a new loan amount of $450,000. After paying off the original mortgage, you would receive approximately $130,000 in cash (before closing costs). These funds can be strategically deployed as a down payment on a multi-family property or used to provide liquidity for a bridge loan on a new acquisition.

Chicago’s Real Estate Market: Stability and Growth

In the Midwest, the Chicago real estate market offers a different but equally compelling narrative of stability and value. While coastal markets often see dramatic price swings, Chicago’s diverse economy and inventory of classic multi-unit buildings provide a solid foundation for landlord financing and long-term wealth building. This morning's Fed report, which suggests a leveling off of borrowing costs, is a welcome sign for Chicagoans exploring local neighborhood market reports. The city remains a prime destination for real estate investor loans, particularly for those focused on the "buy-and-hold" strategy in developing neighborhoods.

For the Chicago investor, the availability of Non-QM mortgage loans and bank statement loans is crucial for navigating the city's unique mix of self-employed professionals and entrepreneurs. The Fed's latest economic outlook indicates that the labor market remains resilient, which supports steady occupancy rates and consistent rental growth across the Chicagoland area. Whether you are looking at a two-flat in Logan Square or a commercial property in the Loop, understanding how these national economic shifts impact local lending standards is the key to closing deals in 2026. The predictability of the current monetary policy allows for better structuring of apartment building financing and mixed-use developments.

Investor Opportunities in the Windy City

Chicago’s market is particularly well-suited for the Debt Service Coverage Ratio (DSCR) model, where the property’s ability to cover its own debt is the primary qualification factor. DSCR investor loans are ideal for scaling a portfolio quickly, as they do not typically factor in your personal debt-to-income ratio. This allows seasoned investors and newcomers alike to capitalize on the city's strong rental demand. As the Fed moves toward a neutral policy stance, the spreads on these non-traditional products often become even more competitive, providing an excellent entry point for those looking to build a rental empire.

Financial Example: Chicago DSCR Loan Calculation

Consider an investor purchasing a four-unit apartment building in a appreciating Chicago neighborhood for $400,000. The projected annual gross rental income is $42,000, and the estimated annual debt service (including principal, interest, taxes, insurance, and HOA) is $30,000. To find the DSCR, you divide the Net Operating Income by the Debt Service. In this scenario, a DSCR of 1.40 ($42,000 / $30,000) indicates a very healthy cash flow, well above the typical lender requirement of 1.15 to 1.25.

Strategic Financing for the Modern Investor

The landscape of real estate finance has expanded far beyond traditional 30-year fixed mortgages, and today's Fed report reinforces the importance of diverse funding options. For those involved in the rapid revitalization of neighborhoods, fix and flip loans and hard money loans provide the speed and flexibility needed to secure distressed assets before the competition. These programs are essential in states like Alabama, Georgia, and Michigan, where urban renewal projects are driving significant investor interest. By understanding the Fed’s influence on short-term rates, you can better time your exit strategies when transitioning from a high-interest bridge loan to permanent long-term financing.

Self-employed borrowers and those with non-traditional income streams should also explore bank statement loans and ITIN mortgage loans. These products are designed to provide access to homeownership for the millions of Americans who do not fit the standard W-2 box but have the financial strength to sustain a mortgage. The Fed’s latest report, which highlights a stable and growing workforce, encourages lenders to continue offering these innovative non-QM mortgage loans. Whether you are a freelance consultant in Virginia or an entrepreneur in Missouri, there are pathways to financing that align with your specific professional profile and financial goals.

The Path Forward for Borrowers and Realtors

As we analyze the data from this morning's Federal Reserve release, the message for the real estate community is clear: preparation and education are your most valuable assets. While the macro-economic environment remains complex, the stabilization of inflation and the cautious approach to interest rates provide a foundation for strategic planning. Realtors and loan officers must work together to guide clients through the various loan programs available, ensuring that every borrower finds a solution that meets their immediate needs and long-term objectives. From VA loans for our veterans to complex commercial real estate loans for developers, the opportunities are vast.

The housing markets in Indiana, Kentucky, Arkansas, and California all react differently to these national shifts, making it vital to work with a strategist who understands the local nuances. By staying informed on the Fed's trajectory, you can anticipate changes in lending appetite and adjust your investment strategies accordingly. We encourage you to delve deeper into the mortgage basics and use the mortgage calculators available on our platform to run your own scenarios. The path to homeownership and real estate wealth is built on a series of well-informed decisions made today.

For the latest official updates and detailed data on the national economy, you can reference the Federal Reserve’s Monetary Policy Report or visit the Bureau of Labor Statistics for comprehensive employment and inflation statistics. Staying connected to these primary sources ensures that your financial strategies are always based on the most accurate and up-to-date information available.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664