Why Everyone Is Talking About the May Housing Inventory Spike (And You Should Too)

The housing market landscape is undergoing a significant transformation this May, and the latest data reveals a shift that few predicted just twelve months ago. According to recent market reports from the National Association of Realtors (NAR), total housing inventory has surged by over 20% compared to the same period last year. This influx of homes for sale is creating a unique window of opportunity for buyers and investors who have been sidelined by the inventory drought of previous years. You are seeing more "For Sale" signs appearing in neighborhoods from Chicago to Orlando, signaling a move toward a more balanced market. Exploring these trends now can help you position yourself for success before the summer peak.

Understanding the "Months’ Supply" Metric

In the world of real estate finance, the "Months’ Supply" is a critical indicator of market health and negotiating power. This metric represents how long it would take for all current listings to sell at the present sales pace if no new homes were added to the market. Historically, a six-month supply represents a balanced market where neither buyers nor sellers have a distinct advantage over the other. As of May, the national supply has climbed to roughly 4.6 months, a notable jump from the sub-3-month levels seen in early 2024. For you, this means more choices and, more importantly, more leverage when it comes to seller concessions and price negotiations.

Why Rates and Inventory Are Moving Together

It might seem counterintuitive that inventory is rising while mortgage rates remain stubbornly high, but the two are deeply linked. Many homeowners who previously felt "locked in" to their low interest rates are finally reaching a breaking point where life changes: like job relocations or growing families: outweigh the desire to keep a 3% mortgage. Additionally, high rates have cooled buyer demand, which allows properties to sit on the market longer and contributes to the growing "standing inventory." You might notice that homes in cities like Atlanta or Richmond are staying active for 50 days or more, giving you more time to conduct due diligence. This "slowdown" is actually a healthy reset for a market that was previously overheating at an unsustainable pace.

Strategic Financing for the New Market

With more inventory available, real estate investors are increasingly looking at DSCR Investor Loans to expand their portfolios without the hurdles of traditional income verification. A Debt Service Coverage Ratio (DSCR) loan allows you to qualify based on the rental income generated by the property rather than your personal W-2 earnings. This is a powerful tool for those looking to acquire properties in Florida or California where home values remain high but rental demand is surging. By focusing on the property's ability to pay for itself, you can bypass the complex debt-to-income (DTI) calculations that often stall traditional financing. Jump in and compare how these specialized programs can help you scale your real estate business in a high-inventory environment.

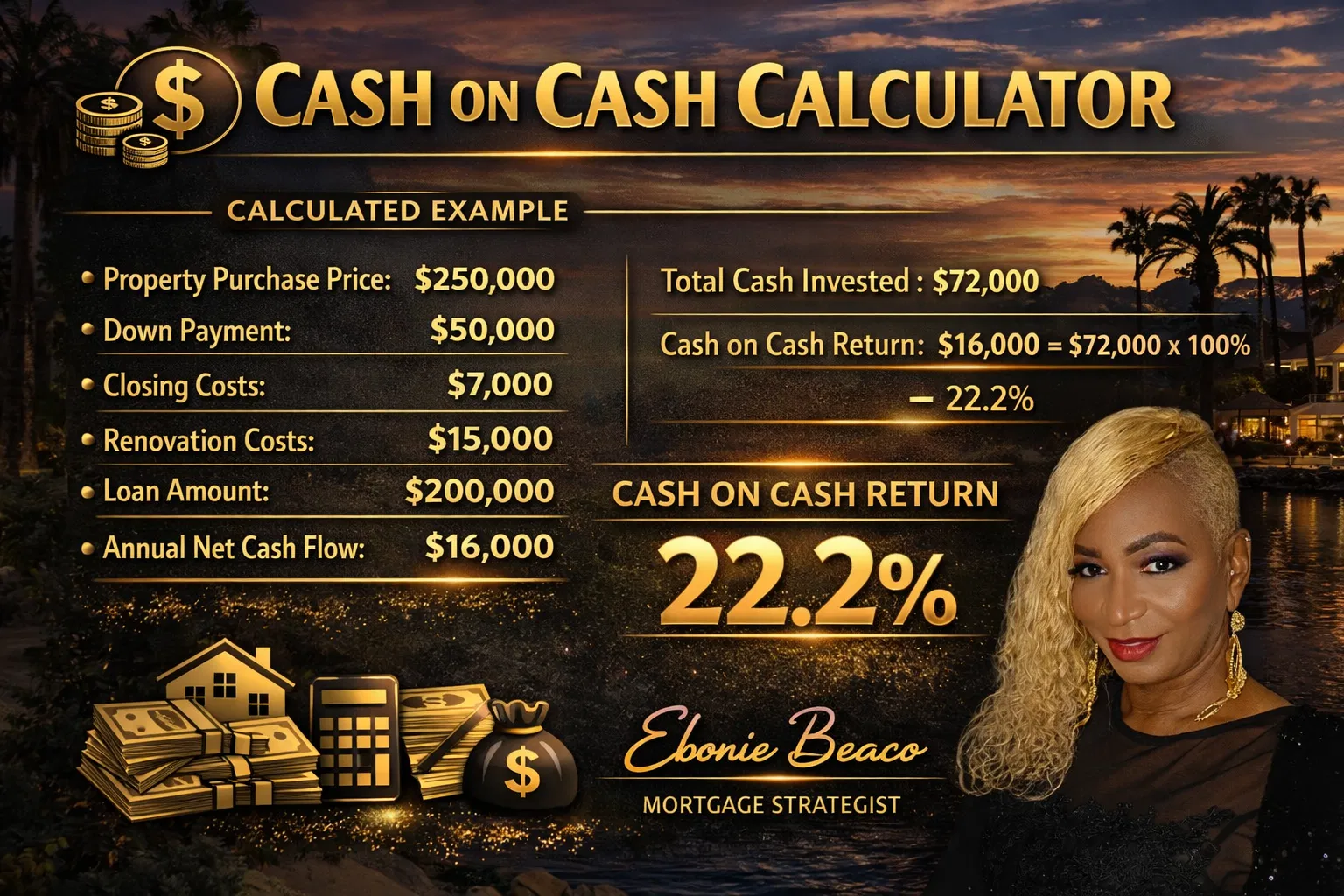

Real-World Example: The Investor’s Advantage

Consider an investor looking at a multi-family property in Indiana with a purchase price of $400,000. Under the old inventory constraints, this property might have sold in a weekend with multiple over-asking offers, leaving no room for a thorough inspection or financing contingencies. Today, that same investor can use a Non-QM Mortgage Loan to secure the property while the inventory spike keeps competition manageable. If the property generates $3,500 in monthly rent and the total mortgage payment (Principal, Interest, Taxes, Insurance) is $2,700, the DSCR would be approximately 1.29. This healthy ratio not only secures the loan but also provides a "safety margin" for the investor’s cash flow.

Accessing Equity to Fuel Your Next Purchase

For current homeowners in Virginia or Michigan who have seen their property values skyrocket, the inventory spike presents a chance to tap into their "lazy equity." A HELOC (Home Equity Line of Credit) or a Cash-Out Refinance can provide the necessary capital to fund a down payment on an investment property or a second home. While rates are higher than they were a few years ago, the ability to access $100,000 or more in liquidity can be life-changing for your long-term wealth strategy. You can use these funds to buy distressed properties for a Fix and Flip project or to secure a Bridge Loan while you wait for a traditional sale to close. Transparency and education are key when deciding which equity strategy aligns with your specific financial goals.

Navigating Price Cuts and Seller Motivation

One of the most telling statistics from the May inventory report is that nearly 20% of active listings have seen price reductions. This represents the highest share of price cuts for any month of May since 2016, indicating that sellers are becoming more realistic about current market conditions. For you as a buyer, this is a clear sign of growing seller motivation, which can be leveraged during the closing process. Whether you are a first-time homebuyer or an experienced landlord, these price adjustments can make the difference between a deal that barely breaks even and one that provides immediate equity. Accessing the latest market data for your specific ZIP code is the best way to identify which sellers are ready to negotiate.

Regional Highlights: Where the Inventory Is Growing Fastest

The inventory surge is not uniform across the country, with some states seeing much more dramatic shifts than others. The South and the West, particularly Florida and California, are leading the way with double-digit increases in active listings. In states like Georgia and Alabama, the market is gradually shifting from a "seller's market" to a "balanced market," providing a breath of fresh air for those who were previously priced out. Even in the Midwest, states like Missouri and Illinois are seeing a steady rise in new listings, offering more variety for those looking at single-family homes or mixed-use properties. Staying informed about these regional nuances ensures your financing strategy is tailored to the local environment.

The Path Forward for Homeowners and Investors

As we move further into the year, the "inventory spike" is likely to remain the most talked-about topic in real estate. While mortgage rates will continue to fluctuate based on economic reports and Fed policy, the increased supply of homes is a constant that you can use to your advantage today. Whether you are looking to refinance, buy your first home, or build a rental empire, the current market dynamics are creating pathways to wealth that were previously closed. Explore your options, ask the hard questions about loan programs, and ensure you have a mortgage strategist who understands how to navigate this shifting landscape. The most successful participants in the real estate market are those who act when the data reveals a clear opportunity.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664