Why Everyone Is Talking About HELOCs in Virginia: And the One Big Catch You Need to See

If you have spent any time scrolling through real estate news or chatting with neighbors in Richmond, Virginia Beach, or Alexandria lately, you have likely heard the term HELOC tossed around like it is a magic wand for home repairs and high interest debt. Virginia homeowners are sitting on a mountain of home equity: collectively billions of dollars: and they are looking for the most efficient way to put that wealth to work.

But while the flexibility of a line of credit is incredibly appealing, there is a specific structural detail that catches thousands of borrowers off guard every year. If you do not understand how this one piece of the puzzle moves, your "flexible" financial tool can quickly turn into a monthly payment headache.

Defining the Terms

Before we jump into the strategy, let's establish exactly what we are discussing. The mortgage industry is full of acronyms that can feel like a different language. Here are the clear definitions you need to navigate these waters:

- Home Equity Line Of Credit (HELOC): A revolving line of credit that allows you to borrow against the equity in your home, similar to how a credit card works but with much lower interest rates because it is secured by your property.

- Combined Loan-To-Value (CLTV): The ratio of all loans on your property (your first mortgage plus the new HELOC) compared to the appraised value of the home.

- Draw Period: The initial phase of a HELOC: typically 10 years: during which you can take money out of the line and usually make interest-only payments.

- Repayment Period: The second phase where you can no longer borrow money and must begin paying back both the principal and interest over a set term.

- Debt-To-Income (DTI): A calculation used by lenders that divides your total monthly debt obligations by your gross monthly income to ensure you can afford the new payment.

The Real Reason Virginia and Michigan Equity Is Skyrolling

In markets like Virginia and Michigan, home values have held remarkably steady through the shifts of early 2026. In the Richmond metro area, for example, many homeowners have seen equity gains nearing $200,000 over the last decade. This is not just "paper money": it is a liquid resource that can be accessed through a Virginia HELOC lender to fund life's biggest transitions.

Similarly, as a Michigan HELOC lender, I see homeowners in the Midwest using these lines to prepare for property expansions or to consolidate credit card debt that has reached 20% or 30% interest. When you compare a 25% credit card rate to a HELOC rate that is significantly lower, the math starts to make sense very quickly.

Explore our mortgage basics to see how equity functions in your specific region.

The One Big Catch: The Variable Rate Rollercoaster

Here is the part where most people stop reading the fine print. Unlike your standard 30-year fixed mortgage, nearly every HELOC is a variable rate product. This means your interest rate is tied to an index: usually the U.S. Prime Rate.

When the Federal Reserve makes a move, your HELOC payment follows. If you open a line when rates are low, but the economy shifts six months later, your monthly obligation could rise significantly. This is known as "payment shock," and it is the primary risk that transparent mortgage strategists will always highlight.

Furthermore, the transition from the Draw Period to the Repayment Period is the second part of the catch. Many borrowers get comfortable making small, interest-only payments for ten years. When year eleven hits and the bank requires you to start paying back the principal, your payment can double or even triple overnight. This "cliff" is why having a clear exit strategy is non-negotiable.

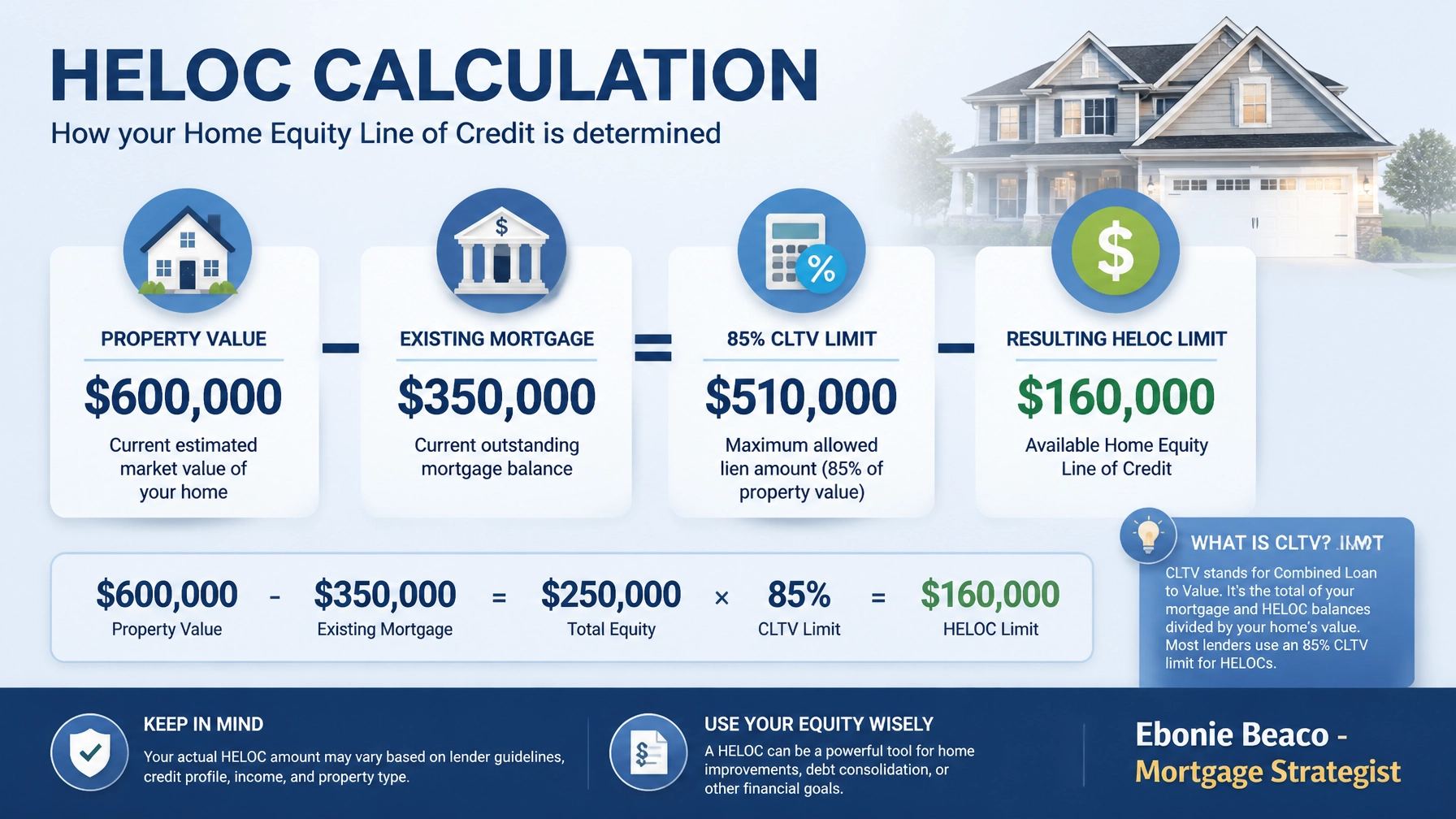

The Math: A Real World Virginia Example

To understand how this looks in your bank account, let's look at a typical scenario for a homeowner in Northern Virginia or the tidewater region.

Imagine you own a home valued at $600,000. You have worked hard to pay your primary mortgage down to a balance of $350,000. Most lenders will allow a CLTV of up to 85%.

- Total Borrowing Capacity: $600,000 x 0.85 = $510,000.

- Current Debt: $350,000 (Your primary mortgage).

- Available HELOC Limit: $510,000 - $350,000 = $160,000.

In this scenario, you now have a $160,000 credit line. You don't have to use all of it. If you only need $40,000 to renovate your kitchen, you only pay interest on that $40,000. This is a massive advantage over a traditional cash-out refinance, where you would be forced to take the full lump sum and pay interest on the entire amount from day one.

How Savvy Investors Are Scaling Portfolios

It is not just homeowners looking for new countertops who are using these tools. Real estate investors are the biggest proponents of the HELOC strategy. Many use the equity in their primary residence to fund the down payment on their next investment property.

- The Airbnb Play: Using a HELOC to purchase and furnish a short-term rental property in a high-demand Virginia tourist area.

- The BRRRR Strategy: Funding the "Buy" and "Rehab" phases of a rental property with a line of credit, then refinancing the property later to pay the HELOC back.

- Fix and Flip: Accessing quick cash to close on a distressed property before another buyer can get their financing in order.

For those looking to scale, our loan programs offer specialized options that go beyond standard residential lines, including DSCR loans for serious landlords.

Finding the Right Michigan or Virginia HELOC Lender

Choosing a lender is about more than just the lowest "teaser" rate. You need to look at the "margin": the extra percentage points the lender adds to the Prime Rate. You also need to ask about annual fees, inactivity fees, and whether they offer a "fixed-rate lock" option. Some modern HELOCs allow you to lock in a portion of your balance at a fixed rate, protecting you from the variable rate catch we discussed earlier.

Whether you are looking for a Michigan HELOC lender to help you consolidate debt or a Virginia HELOC lender to jump into your first investment deal, the key is transparency. You deserve to know exactly how your payment will change if the market shifts.

Are You Ready to Unlock Your Equity?

Accessing your home equity is one of the most powerful wealth-building moves you can make, but it requires a strategist who looks at your whole financial picture, not just a credit score. We help you navigate the loan process from the initial soft credit pull to the final funding of your line.

Jump in and see what your home is truly capable of doing for your future. Whether you are in Alabama, Florida, Illinois, or Virginia, your equity is a tool that should be managed with precision and care.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664