Why Everyone in Virginia is Talking About HELOCs Right Now (And the One Catch You Need to Watch For)

The Virginia HELOC buzz is real… but it’s not just Virginia

If you own a home in Virginia, you’ve probably heard the same sentence a dozen ways lately: “Just open a HELOC.”

And honestly, I get why it’s trending.

A lot of homeowners across Virginia, Michigan, Illinois (including Chicago), Indiana, Kentucky, Missouri, Alabama, Arkansas, Georgia, Florida, and California are sitting on equity, holding low first-mortgage rates from prior years, and still wanting cash for renovations, debt cleanup, investments, or tuition.

A HELOC can feel like the “clean” solution.

But there’s one catch that can quietly turn a smart plan into an expensive surprise.

Stick with me, because I’m going to show you the catch, how to stress-test your payment, and how investors are using HELOCs alongside DSCR, BRRRR, and fix and flip strategies.

CTA: If you want a second set of eyes on your numbers, schedule a 1 on 1 with me.

HELOC 101 (plain-English definitions you can use)

HELOC (Home Equity Line of Credit)

Definition: A revolving line of credit secured by your home’s equity.

Practical use: You can draw money, repay it, and draw again during the “draw period,” similar to a credit card but usually at a lower rate.

Draw period

Definition: The time window when you can access the line (often 5 to 10 years).

Practical use: Great for staged projects like renovations, or for investors who need flexible capital.

Repayment period

Definition: The phase after the draw period ends when you can no longer draw and must repay the balance.

Practical use: This is when payments often jump if you were paying interest-only before.

CLTV (Combined Loan-to-Value)

Definition: Your first mortgage balance + HELOC limit divided by your home value.

Practical use: Lenders use CLTV to cap how much equity you can access.

DTI (Debt-to-Income)

Definition: Monthly debt payments divided by gross monthly income.

Practical use: Your DTI helps determine approval and how much line you qualify for.

CTA: Want help estimating your CLTV and DTI before you apply? Schedule a 1 on 1.

The reason Virginia homeowners love HELOCs (it’s not hype, it’s math)

1) Virginia equity is strong in many markets

Northern Virginia has seen meaningful appreciation in many neighborhoods, and that often creates usable equity even if you bought recently.

If you’re in Arlington, Alexandria, Fairfax, Loudoun, Prince William, Richmond, or Virginia Beach, you’ve likely watched values move.

2) HELOCs let you keep your low first-mortgage rate

A lot of homeowners still have a first mortgage in the 2% to 4% range.

A cash-out refinance replaces your entire first mortgage, not just the portion you want to access.

A HELOC can sometimes let you access cash without touching your primary fixed rate.

3) You can draw funds only when you need them

This is huge for:

- Renovations: pay contractors in phases.

- Tuition: pull funds per semester.

- Emergency liquidity: keep the line open but unused.

- Real estate investing: move fast on a down payment or rehab.

CTA: If you’re deciding between a HELOC and cash-out refinance, I can walk you through both paths in one call.

The cliffhanger: the “one catch” you need to watch for

Variable interest rates (the real risk hiding in plain sight)

Definition: A rate that can change, typically tied to the Prime Rate (or an index plus margin).

Practical use: Your monthly payment can increase even if you never borrow more.

Here’s why people got burned from 2022 to 2024.

Prime moved up sharply (it went from very low levels in early 2022 to much higher levels later). That meant HELOC rates reset upward, sometimes fast.

Even today, many HELOCs are still priced around the prime-based range.

The transparent takeaway

A HELOC can be a strong tool, but you should treat it like a flexible short-to-mid-term strategy unless you have:

- a payoff plan,

- a clear budget buffer,

- or a fixed-rate conversion option.

Some lenders offer fixed-rate HELOC segments (you lock a portion), which can help if you hate surprises.

CTA: Ask me to show you how the payment changes at 2 to 3 different rate scenarios before you commit.

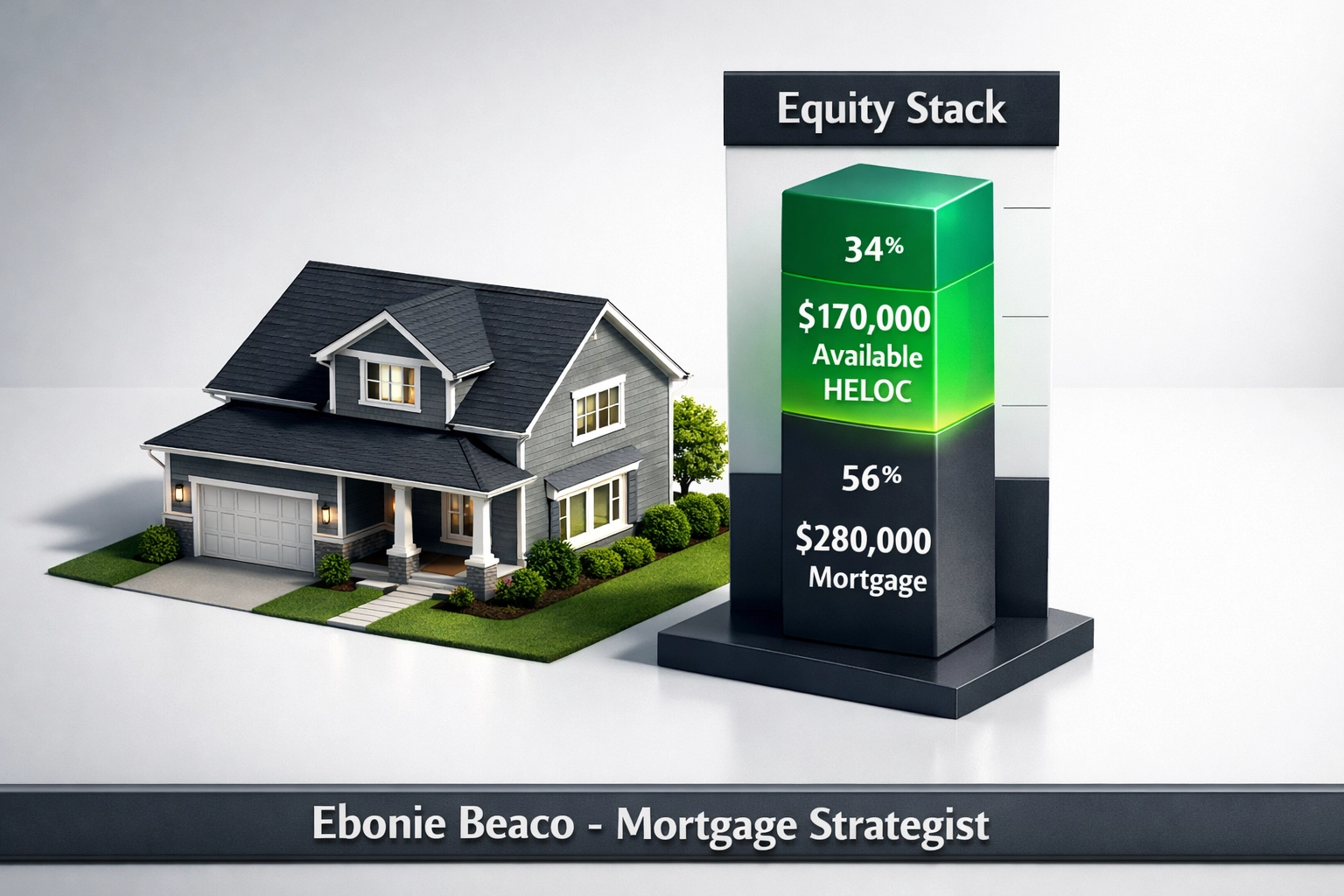

A simple Virginia HELOC example (with real numbers)

Let’s say you own a home in Virginia.

- Home value: $500,000

- Current first mortgage balance: $280,000

- Max CLTV allowed: 90%

- Max total debt allowed: $500,000 × 90% = $450,000

- Potential HELOC limit: $450,000 − $280,000 = $170,000

Now estimate the payment if you draw $100,000 at 7.50% interest-only.

- Monthly interest = $100,000 × 7.50% ÷ 12

- Monthly interest = $625

If the rate later adjusts to 9.50%, interest-only becomes:

- Monthly interest = $100,000 × 9.50% ÷ 12

- Monthly interest = $791.67

That’s a $166.67/month jump without borrowing another dollar.

CTA: If you want a personalized range of “payment at today’s rate” vs “payment if rates rise,” schedule a 1 on 1.

Who is using HELOCs right now (and why it keeps spreading)

Homeowners doing renovations (Virginia, Florida, California)

Renovations are often phased.

A HELOC is built for phased spending, especially in places like Tampa, Orlando, Jacksonville, Miami, San Diego, Riverside, Sacramento, and the Bay Area where home improvement ROI can be meaningful.

CTA: If your contractor schedule spans months, ask about structuring draws and keeping interest costs controlled.

Debt optimization planners (Illinois, Indiana, Kentucky, Missouri)

Some borrowers use HELOCs to consolidate higher-interest debt.

This can be helpful, but you must be disciplined because you’re turning consumer debt into debt secured by your home.

- Consolidation strategy: pay off high-rate cards, stop the swipe habit, and set an aggressive payoff schedule.

- Red flag: paying off cards and then running them back up.

CTA: I can help you compare HELOC vs personal loan vs cash-out refinance based on your timeline.

Investors building a “capital stack” (Michigan, Georgia, Alabama, Arkansas)

Investors love flexible capital.

A HELOC can play a role in:

- BRRRR: buy, rehab, rent, refinance, repeat.

- Fix and flip: quick rehab funding gap coverage.

- Down payment sourcing: pairing with DSCR on the purchase.

But investors also need to manage liquidity risk and rate volatility.

CTA: If you’re combining a HELOC with DSCR or bridge financing, I’ll help you map the full cash flow.

The HELOC vs cash-out refinance decision (and the part people skip)

Cash-out refinance

Definition: A new mortgage that replaces your current first mortgage and gives you cash back.

Practical use: Good when rates are favorable or when you want a fixed payment for the full balance.

HELOC

Definition: Second lien credit line behind your first mortgage.

Practical use: Good when you want flexibility and you want to keep your current first-mortgage rate.

The part people skip: total cost by timeline

- Short timeline (1 to 5 years): HELOC often fits well if you have a payoff plan.

- Long timeline (7 to 30 years): fixed-rate strategies can reduce uncertainty.

CTA: Tell me your timeline and goal, and I’ll help you compare the total cost over time, not just today’s payment.

Virginia-specific watch list: three HELOC pitfalls to avoid

1) Payment shock after the draw period

Some HELOCs shift from interest-only to amortizing repayment.

That can increase your payment dramatically.

Action step: Ask if your HELOC is interest-only during draw, and what the payment looks like once amortization begins.

CTA: I can run a “future payment” estimate so you’re not guessing.

2) Overestimating value (and underestimating underwriting)

Online estimates can be off.

If the appraisal comes in lower, your available line can shrink.

Action step: Build a buffer into your plan so you’re not counting on the maximum.

CTA: If you’re close on CLTV, ask me to help you pre-check the numbers before you apply.

3) Using HELOC funds for speculative investing without a liquidity plan

This shows up with:

- flips that run long,

- Airbnb revenue dips,

- tenant turnover,

- unexpected repairs.

Action step: Keep reserves. Price your deals conservatively.

CTA: If you want a conservative liquidity checklist, schedule a 1 on 1 and I’ll share what I look for.

Quick state-by-state reality check (yes, this applies beyond Virginia)

Michigan

In markets like Detroit, Grand Rapids, Ann Arbor, and Lansing, HELOCs are commonly used for renovations and as investor flexibility capital.

If you’re searching for a Michigan HELOC lender, you want someone who can talk through both homeowner use and investor sequencing (HELOC + DSCR + refi timing) without hand-waving.

CTA: If you’re in Michigan, ask me to help you plan the HELOC around your next purchase.

Illinois (including Chicago)

Chicago-area homeowners often use HELOCs for:

- multi-stage rehabs,

- small multifamily improvements,

- bridging expenses while renovating a unit.

CTA: Want to compare HELOC vs home equity loan vs cash-out refi in Illinois? Let’s map it.

Florida and California

Insurance costs, permitting timelines, and contractor schedules can stretch projects.

A HELOC can help, but variable rates plus long timelines can get expensive.

CTA: If your project timeline is longer than 12 months, ask about fixed-rate options or segmented locks.

Georgia, Alabama, Arkansas, Indiana, Kentucky, Missouri

These states have a mix of homeowners and investors using HELOCs as “cash on standby.”

That’s a smart approach if you treat the HELOC like a tool, not free money.

CTA: I’ll help you set a draw-and-paydown plan you can actually follow.

The “before you apply” checklist (save this)

Underwriting and structure

- CLTV limit: Confirm max CLTV and how value will be determined.

- Rate structure: Confirm index (often Prime), margin, caps, and reset frequency.

- Draw and repayment: Confirm draw period, repayment period, and payment type.

- Fees: Confirm annual fees, closing costs, and early closure terms.

- Lien position: Confirm second lien behind your first mortgage.

Budget and risk control

- Payment stress test: Run payment at +1% and +3% rate scenarios.

- Exit plan: Decide how you will pay it off (sale, bonus, refinance, cash flow).

- Reserves: Keep cash reserves separate from the HELOC itself.

If you want a clean explanation of how lenders typically move a file from application to closing, review our loan flow here: https://www.homeloansnetwork.com/loan-process

CTA: If you’d like, I’ll help you build a one-page plan that includes the rate stress test and payoff strategy.

The bottom line: HELOCs are popular in Virginia for a reason… just respect the catch

A HELOC can be one of the most flexible ways to access equity without rewriting your entire first mortgage.

That’s why you’re hearing so much about HELOCs across Virginia and beyond.

But the variable-rate feature is the piece you need to underwrite like a pro.

If you plan for payment changes, timeline risk, and repayment structure, a HELOC can support renovations, debt strategy, and even real estate investing in a controlled way.

Ready to run your scenario?

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664