Why Everyone from Florida to Michigan Is Talking About HELOCs: And Why You’ll Regret Not Looking Into One Today

The real estate world is buzzing right now. From the sunny coastlines of Florida to the industrial heart of Michigan, homeowners are sitting on a goldmine they haven’t touched. If you are a homeowner or a real estate investor, you have likely noticed that the old ways of accessing cash: like the standard cash-out refinance: are not as attractive as they used to be.

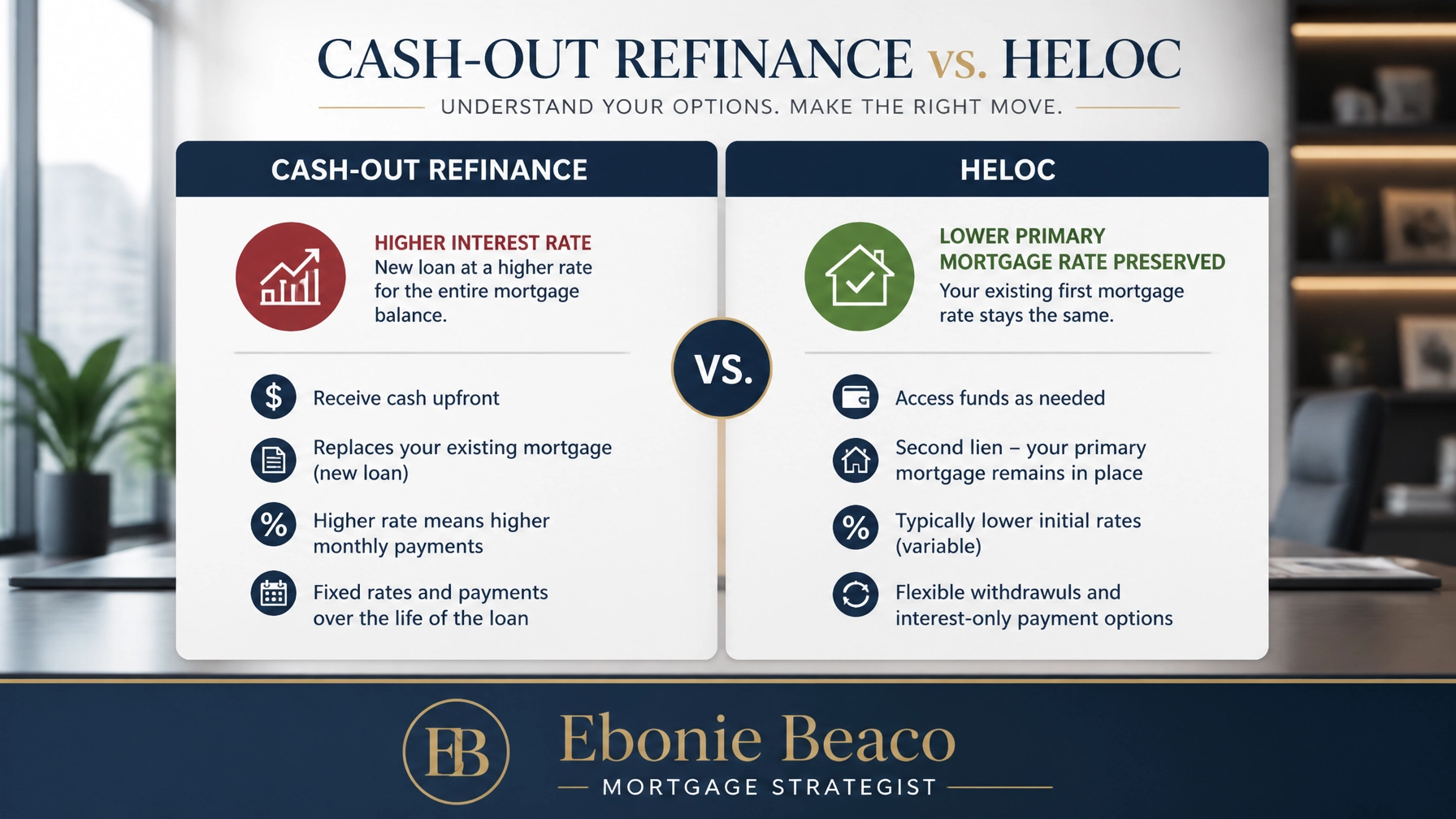

Why is everyone suddenly obsessed with a product that has been around for decades? It is because the market has shifted, and the HELOC has emerged as the most strategic way to leverage your property without touching your existing low-interest mortgage.

If you are waiting for rates to hit 3% again before you take action, you are missing out on incredible opportunities to build wealth today.

The Secret Most Homeowners are Overlooking

The biggest hurdle for most people right now is the "rate lock-in" effect. Most homeowners in states like Illinois, Georgia, and Virginia are currently holding mortgages with interest rates between 2.5% and 4%.

Giving up a 3% rate to get cash at today’s 7% rates via a traditional refinance feels like a step backward. This is exactly where the Home Equity Line of Credit (HELOC) saves the day.

HELOC (Home Equity Line of Credit): A revolving credit line secured by your home’s equity that allows you to borrow, repay, and borrow again during a set draw period.

Application: You use this to access cash for home improvements or investment property down payments while keeping your primary low-interest mortgage untouched.

By choosing a HELOC, you keep that beautiful 3% rate on your main loan. You only pay the higher current interest rate on the specific amount of money you actually draw from your line of credit.

Why Michigan and Virginia are Seeing a HELOC Surge

As a Michigan HELOC lender, I have seen a massive uptick in homeowners in the Detroit and Grand Rapids areas using their equity to weather economic shifts or upgrade their primary residences. Property values in Michigan have seen steady growth, leaving many families with six figures of "trapped" wealth.

Similarly, as a Virginia HELOC lender, I am working with clients in Northern Virginia and Richmond who are using HELOCs to stay competitive. In these fast-moving markets, having a line of credit ready means you can act quickly when a new investment property hits the market or when a renovation project becomes a necessity.

Whether you are in Alabama, Arkansas, California, or Missouri, the logic remains the same: your home is a bank. It is time you started using it like one.

The Investor’s Secret Weapon for Portfolio Expansion

Real estate investors are some of the most frequent users of specialized loan programs. If you are looking to scale your portfolio using the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) method, a HELOC is your best friend.

Imagine finding a distressed property in Indiana or Kentucky. Instead of waiting for a bank to approve a new loan, you simply write a check from your HELOC to cover the purchase and the renovations.

Once the property is fixed up and rented, you can use a conventional loan or a DSCR loan to pay back your HELOC and reset your credit line for the next deal. This is how professional landlords and Airbnb operators in Florida and Georgia are scaling their businesses in a high-interest-rate environment.

Let’s Do the Math: How Much Cash is Actually in Your House?

Understanding your numbers is the first step toward financial freedom. Many people underestimate how much equity they can actually tap into. Most lenders will allow a Combined Loan-to-Value (CLTV) of up to 85% or even 90% depending on your credit profile.

CLTV (Combined Loan-to-Value): The ratio of all loans on a property compared to the property’s total appraised value.

Application: This number tells you the maximum amount you can borrow across your first mortgage and your new HELOC combined.

The Financial Breakdown Example:

- Current Property Value: $500,000

- Max Allowable CLTV (85%): $425,000

- Your Existing Mortgage Balance: $280,000

- Available HELOC Credit Line: $145,000

In this scenario, you have $145,000 available at your fingertips. You do not pay interest on that money until you use it. It can sit there as an emergency fund, a renovation budget, or a down payment for your next three rental properties.

You can use our mortgage calculators to run your own scenarios and see what your specific equity looks like.

The Risk of Doing Nothing

Many homeowners think that waiting is the safest bet. However, in real estate, the cost of waiting is often higher than the cost of borrowing.

If you have debt with high interest rates: like credit cards averaging 24%: using a HELOC at 8% or 9% to consolidate that debt can save you thousands of dollars in interest every single month. This is a transparent strategy to improve your cash flow immediately.

Furthermore, if you are an investor, the "perfect deal" won't wait for you to find funding. Having a HELOC in place means you are a cash buyer in the eyes of a seller. That gives you leverage that other buyers simply do not have.

Exploring Your Options Across the Country

We work with homeowners and investors across several states to find the right financing fit. Whether you are looking for a soft pull credit request to get started or you are ready to dive deep into a complex investment strategy, we are here to guide you.

Our expertise covers:

- Alabama and Arkansas: Navigating emerging markets with high rental demand.

- California and Florida: Leveraging high-value equity for luxury renovations or STR (Short-Term Rental) acquisitions.

- Georgia and Indiana: Building landlord portfolios with high cash flow potential.

- Illinois and Missouri: Utilizing equity for urban redevelopment and multi-unit projects.

- Kentucky and Virginia: Strategic financing for both rural and metro area properties.

- Michigan: Helping homeowners tap into the steady appreciation seen in recent years.

Jump in and see how your home can start working for you today. The equity is there: you just need the right strategist to help you unlock it.

Explore your equity options today.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664