Why Everyone from Florida to California Is Talking About HELOCs (And You Should Too)

From the busy streets of Chicago to the coastal reaches of California and the growing suburbs of Virginia, homeowners are looking at their properties differently. If you have owned your home for more than a couple of years in states like Florida, Georgia, or Michigan, you are likely sitting on a significant amount of equity.

The conversation isn't just about property values anymore. It is about how to use that value without selling your home or giving up a low interest rate on your primary mortgage. This is where the Home Equity Line of Credit, or HELOC, enters the picture.

Explore the mechanics of this financial tool and why it has become the preferred strategy for savvy homeowners and investors across the Home Loans Network service areas.

The Invisible Gold Mine Sitting Under Your Living Room Floor

Many homeowners in Alabama, Arkansas, and Missouri are surprised to realize how much wealth they have accumulated through home appreciation. You might not see it in your bank account, but it is there, locked in your walls and land.

Home Equity: The difference between the current market value of your property and the outstanding balance of all liens on the property.

Practical Application: If your home in Michigan is worth $400,000 and you owe $250,000, you have $150,000 in equity that can potentially be leveraged for other financial goals.

HELOC: A revolving line of credit that uses your primary residence or investment property as collateral.

Practical Application: You can borrow against your equity, pay it back, and borrow again, much like a high-limit credit card but with typically much lower interest rates.

Jump in and look at why this specific tool is gaining traction in states like Kentucky and Indiana. While traditional loans provide a lump sum, a HELOC offers flexibility. You only pay interest on what you actually spend. This transparency is a core part of how we operate at Home Loans Network.

The Secret Mechanism of Home Equity You Haven't Used Yet

What makes a HELOC different from a standard home equity loan? It comes down to the "Draw Period" and the "Repayment Period."

Draw Period: A set timeframe, usually 5 to 10 years, during which you can withdraw funds from your credit line as needed.

Practical Application: You might use $20,000 for a kitchen remodel in year one and another $10,000 for tuition in year three without reapplying for a new loan.

Repayment Period: The phase following the draw period where you can no longer withdraw funds and must pay back the remaining balance plus interest.

Practical Application: This period often lasts 10 to 20 years, allowing for manageable monthly payments to clear the debt.

In high-growth markets like Virginia and Florida, this flexibility is vital. As a Virginia HELOC lender, we often see homeowners use the draw period to fund strategic renovations that further increase the home's value before they ever enter the repayment phase.

Why Your Credit Card Might Be Your Biggest Financial Liability

If you are carrying high-interest debt in Chicago or anywhere in Illinois, you are likely paying 20% or more in interest. This is a massive drain on your monthly cash flow.

Compare that to a HELOC. Because the loan is secured by your home, the interest rates are significantly lower than unsecured credit cards or personal loans. Homeowners are using HELOCs for debt consolidation, essentially swapping high-interest debt for a lower-interest line of credit.

Access this strategy to simplify your finances. By consolidating multiple payments into one HELOC payment, you reduce your monthly overhead and potentially save thousands in interest over the life of the debt.

The Real Estate Investor’s Multi-Tool: Scaling Your Portfolio

For real estate investors in Georgia and California, a HELOC is more than a safety net; it is a growth engine. Investors use HELOCs to fund the "Buy" and "Renovate" stages of the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) method.

LTV (Loan-to-Value): The ratio of a loan to the value of an asset purchased.

Practical Application: Most HELOC programs allow you to borrow up to 80% or 85% of your home's total value, including your primary mortgage.

DSCR (Debt Service Coverage Ratio): A measurement of the cash flow available to pay current debt obligations.

Practical Application: While HELOCs are typically based on personal income, savvy investors use the funds from a HELOC to purchase rental properties that qualify for DSCR loans based on the property’s income alone.

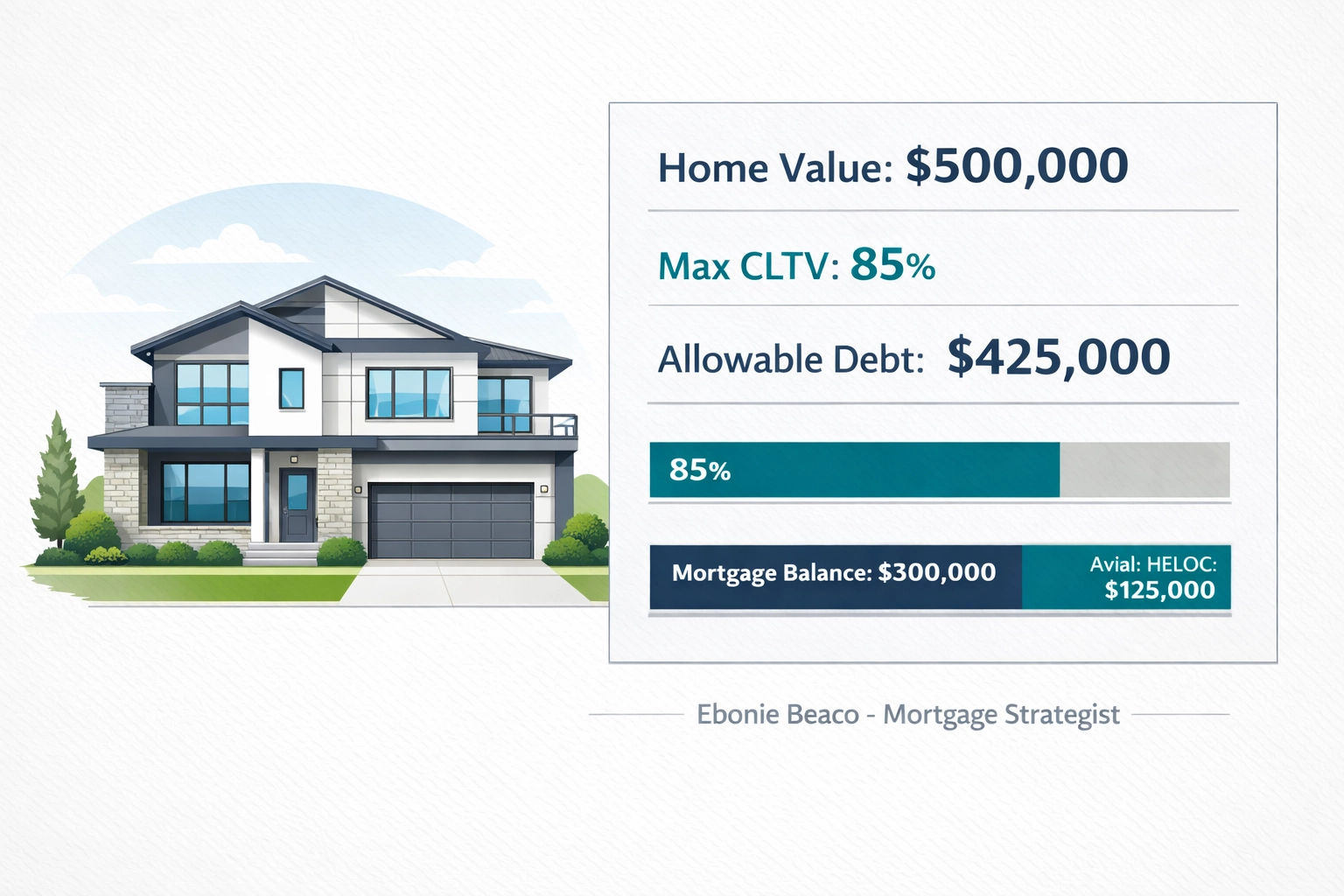

Where Does the Money Actually Come From? A Real-World Calculation

Let’s look at a practical scenario for a homeowner in Michigan. Understanding the math is the first step toward financial clarity.

The Scenario:

- Current Home Value: $500,000

- Current Mortgage Balance: $300,000

- Max Combined Loan-to-Value (CLTV): 85%

The Calculation:

- Calculate total allowable debt: $500,000 x 0.85 = $425,000

- Subtract the existing mortgage: $425,000 - $300,000 = $125,000

- Available HELOC Limit: $125,000

In this case, the homeowner has a $125,000 line of credit waiting for them. If they don't use it, they don't owe anything. If they use $10,000 for a repair, they only pay interest on that $10,000.

As an experienced Michigan HELOC lender, we walk clients through these numbers daily to ensure they understand exactly how much liquidity they can unlock.

What Happens When You Reach the Draw Period Limit?

A common question we hear at Home Loans Network is: "What happens when the party ends?"

Transparency is key here. When the draw period ends, your monthly payment will increase because you will start paying back both the principal and the interest.

Interest-Only Payments: A feature where you only pay the interest charges each month during the draw period.

Practical Application: This keeps your monthly costs extremely low while you are using the funds for investments or improvements, but you must be prepared for the principal payments later.

Before you reach that point, many homeowners choose to perform a home refinance to roll the HELOC balance into a new first mortgage. This is a common strategy in California and Florida where property values often rise fast enough to cover the combined debt easily.

The Reason High-Interest Rates on First Mortgages Don't Stop HELOCs

We are currently in a market where many people have a first mortgage rate of 3% or 4%. If you need cash, a cash-out refinance would force you to replace that entire 3% loan with a new one at current market rates.

That is a losing move for most.

The HELOC allows you to keep your 3% rate on your main mortgage. You only take the current market rate on the smaller line of credit. This protects your low-cost debt while still giving you access to the cash you need. This is exactly why homeowners from Virginia to Missouri are choosing "second-lien" financing over traditional refinances.

Navigating the Local Markets: From Alabama to Virginia

Every state has its own nuances when it comes to property values and lending.

- Florida and California: High appreciation makes HELOCs massive. Homeowners here often have six figures of equity to tap into.

- Illinois (Chicago): A great market for using HELOCs to renovate older homes and increase their competitive edge.

- Michigan and Indiana: Reliable markets where a HELOC can provide a "rainy day" fund for unexpected expenses.

- Virginia: A hub for professional homeowners who use HELOCs as a strategic tool for secondary investment properties.

Whether you are looking for a Virginia HELOC lender or a Michigan HELOC lender, the goal is the same: providing a clear path to your financial objectives. You can learn more about our team and our approach on our about us page.

Is a HELOC Right for Your Specific Situation?

While the benefits are many, a HELOC is not a "one size fits all" solution. It requires discipline. Because it is a revolving line of credit, it can be easy to overspend.

Collateral: An asset that a lender accepts as security for a loan.

Practical Application: Your home is the collateral. If you cannot make the payments, the home is at risk.

This is why we focus on education. We want you to understand the mortgage basics before you sign on the dotted line. A HELOC is a powerful tool, but it should be used as part of a broader financial strategy.

How to Get Started Without the Stress

The process of securing a HELOC is often faster and involves fewer closing costs than a traditional mortgage.

- Check Your Equity: Get a professional estimate of your home's current value.

- Review Your Credit: Higher credit scores typically unlock better interest rates.

- Calculate Your DTI: Debt-to-Income ratio is a key factor lenders use to ensure you can handle the new line of credit.

- Compare Options: Look at different draw periods and interest rate structures.

If you are curious about how the numbers look for your specific property, you can use our mortgage calculators to run different scenarios.

Explore your options with a team that values transparency and expert guidance. Whether you are an investor looking to scale or a homeowner looking to improve your living space, your home equity is a resource that shouldn't go to waste.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664