Wholesale Wars: Hedge Funds vs. Local Investors: Which Buyer Wins?

The wholesale landscape in markets like Chicago, Illinois, or Atlanta, Georgia, has shifted significantly with the entry of institutional buyers. Wholesaling houses used to mean building a list of local "mom and pop" investors who would buy one or two properties a year to fix and flip. Today, you are often choosing between a local professional and a massive hedge fund that manages thousands of doors across Florida or California. Real estate investing at the wholesale level requires you to understand the specific motivations of these two very different buyer types. Identifying the right partner for your off-market deals determines how quickly you can move onto the next project and how much profit you ultimately retain. You should analyze each deal based on the speed of closing versus the complexity of the property’s needs.

The Rise of the Institutional Buyer in Modern Wholesaling

Hedge funds represent a unique tier of cash buyers that prioritize volume and standardized criteria over individual property quirks. These entities often buy dozens of properties a day in high-demand areas like Virginia or Michigan because they operate on massive institutional scales. They provide an incredible level of certainty for a wholesaler because their "buy box" is clearly defined and their funding is rarely an issue. When you submit a deal that fits their parameters, the process is typically streamlined through regional managers who oversee large swaths of the Midwest or Southeast. However, these funds are notoriously rigid and rarely negotiate on price or terms once an initial offer is generated by their algorithms. They excel at purchasing "turnkey-lite" properties that require minimal structural intervention before being converted into long-term rentals.

Institutional office buildings in a major metropolitan city skyline represent the scale of hedge fund buyers.

The Local Investor Advantage: Flexibility and Problem Solving

Local investors bring a level of flexibility and market-specific knowledge that institutional funds simply cannot replicate in cities like Indianapolis or St. Louis. These buyers often utilize specialized financing like fix and flip loans to acquire properties that need significant rehabilitation. Because they live and work in the community, they understand the value of a specific block or an upcoming school district change that a hedge fund's data might miss. Selling to a local investor often involves a more personal relationship where you can negotiate assignment fees more openly. They are more likely to take on "heavy lifts" or properties with title issues that would cause a hedge fund to automatically decline the deal. Your ability to solve complex problems for these local buyers creates a sustainable business model that persists even when institutional appetites fluctuate.

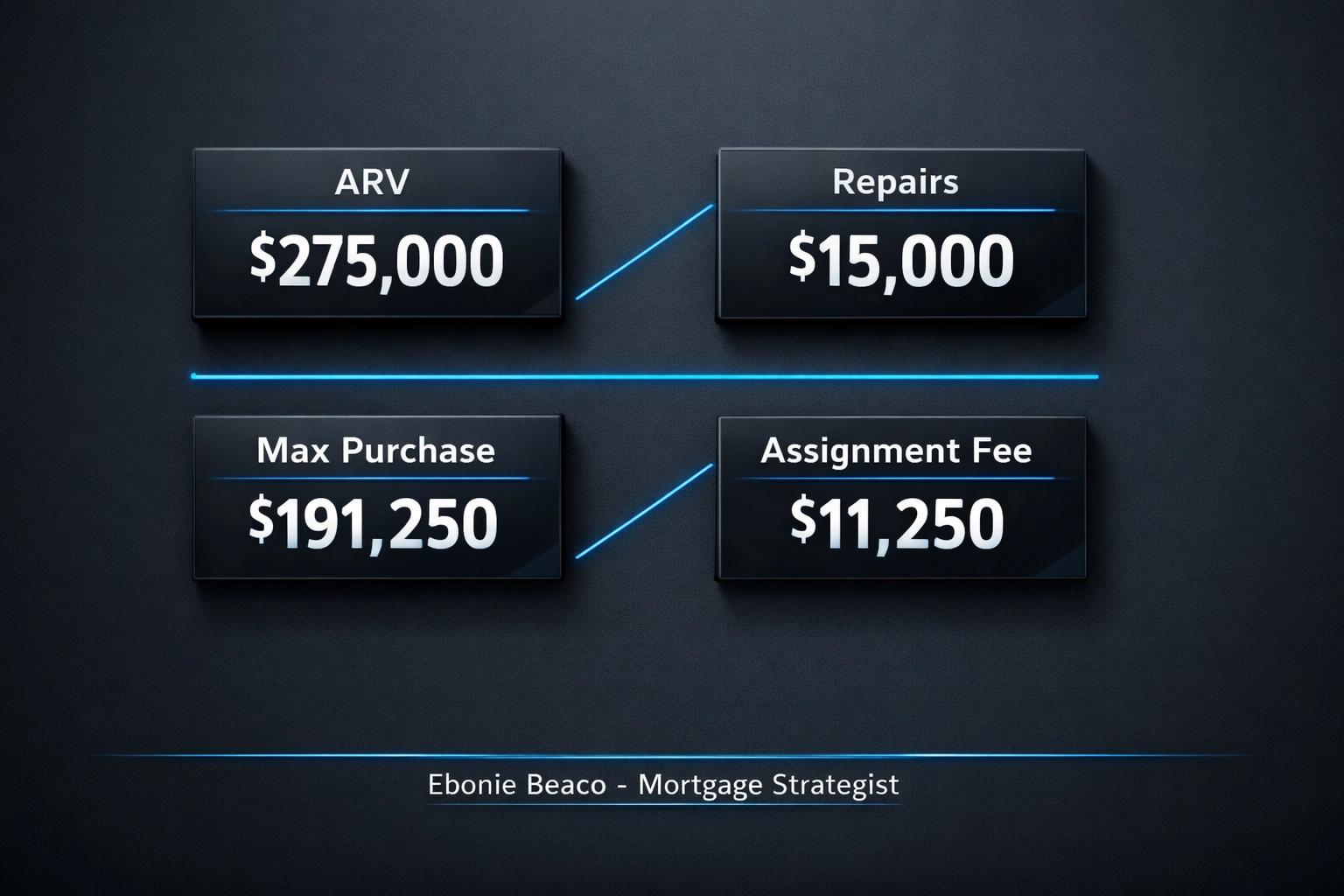

Analyzing the Numbers: The Institutional Exit Strategy

Explore a practical example of a wholesale deal sold to a hedge fund in a market like Jacksonville, Florida. Imagine you secure an off-market deal for $180,000 on a property with an After Repair Value (ARV) of $275,000 that needs about $15,000 in cosmetic work. A hedge fund might have a "buy box" that allows them to pay up to 75% of ARV minus repairs, which calculates to $206,250 minus $15,000, leaving a max purchase price of $191,250. You can assign this deal for an $11,250 fee, bringing the total cost to the fund to $191,250. Because the fund uses its own massive capital reserves, you avoid the complications of third-party appraisals or lengthy financing contingencies. This speed allows you to recycle your capital and move into new home purchase opportunities much faster than traditional methods.

Hedge Fund Deal Analysis: ARV $275,000 | Repairs $15,000 | Max Purchase $191,250 | Assignment Fee $11,250.

Analyzing the Numbers: The Local Fix-and-Flip Strategy

Compare that to a deal involving a local fix-and-flip investor in a market like Detroit or Birmingham. This buyer might be looking at a property with an ARV of $250,000 but requiring $60,000 in structural and cosmetic renovations. While a hedge fund would likely pass on this due to the heavy renovation, a local investor using hard money loans sees opportunity. If the investor needs a 15% profit margin ($37,500), their maximum allowable offer (MAO) might be $250,000 (ARV) minus $60,000 (repairs) minus $37,500 (profit) minus $12,500 (holding/buying costs), resulting in a $140,000 purchase price. If you contracted the property for $120,000, your assignment fee is $20,000, which is higher than the hedge fund deal despite the lower ARV. Local investors often allow for higher wholesale spreads on distressed assets because they add more value through the renovation process.

Local Investor Deal Analysis: ARV $250,000 | Repairs $60,000 | Profit $37,500 | Holding Costs $12,500 | MAO $140,000 | Assignment Fee $20,000.

Diversifying Your Buyer List for Long-Term Stability

You must evaluate your long-term goals when deciding which buyer pool to cultivate for your wholesale real estate business. Hedge funds offer a "set it and forget it" model where you can feed them a consistent stream of similar assets in states like Arkansas or Kentucky. This creates a predictable income stream but makes you vulnerable if that specific fund decides to exit a market overnight. Conversely, building a robust network of local landlords who use DSCR investor loans provides more stability across different economic cycles. These landlords are often looking for long-term holds and are less sensitive to minor market corrections than a large fund focused on quarterly earnings. Diversifying your buyer list ensures that no single entity holds the power to stall your business operations or cash flow.

How Strategic Financing Empowers Your Cash Buyers

Understanding how your buyers fund their acquisitions is a critical component of being a successful wholesaler in today's environment. When you work with local investors, they often rely on a cash-out refinance from previous projects to fund new wholesale purchases. You can add value to your buyers by introducing them to aggressive lending products that help them scale, such as portfolio loans. Providing a "package deal" where you bring the property and a connection to a reliable lender makes your wholesale deals much more attractive. This approach transforms you from a simple transaction coordinator into a strategic partner for their growing real estate portfolio. Many successful wholesalers even keep a list of preferred lenders to ensure their buyers can close as quickly as a hedge fund would.

Choosing Your Path in the Wholesale Market

The "winner" in the battle between hedge funds and local investors depends entirely on the specific property and your current business needs. Use hedge funds for clean, predictable houses in suburban markets like those found in Northern Virginia or suburban Chicago where speed is the priority. Reserve your distressed, high-equity deals for local experts who can navigate the complexities of a full renovation and utilize creative financing strategies. By maintaining relationships with both groups, you position your wholesaling houses business to thrive regardless of which direction the broader economy moves. Access our mortgage calculators to help your buyers analyze their potential returns more effectively before they commit to a deal. Balancing these two buyer types will help you maximize your assignment fees while building a reputation as a versatile and knowledgeable wholesaler.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664