Wholesale Real Estate Compliance: Staying Legal While Staying Profitable

Navigating the landscape of wholesale real estate in 2026 requires a sophisticated understanding of both market mechanics and the evolving regulatory environment that governs how investors operate. While wholesaling houses remains a powerful entry point for many, the industry has shifted toward a model of radical transparency that demands every participant act with the precision of a licensed professional. You must recognize that staying compliant is not a barrier to your success but rather the foundation upon which you build a scalable and reputable investment business. Throughout states like Illinois, California, and Florida, authorities have tightened the definitions of what constitutes brokering without a license, making it essential for you to structure your contracts around the sale of an equitable interest rather than the property itself. By prioritizing legal integrity, you distinguish yourself from the "fly-by-night" operators and position your brand as a reliable source of off-market deals for serious cash buyers and institutional investors.

Licensing requirements have become a pivotal focal point for anyone engaged in wholesaling houses across major metropolitan hubs like Chicago, Los Angeles, and Atlanta. In Illinois, for instance, the regulatory framework clearly dictates that performing more than one wholesale transaction within a twelve-month period necessitates a real estate license to avoid hefty fines and legal scrutiny. Similarly, states such as South Carolina and Kentucky have implemented strict mandates that essentially categorize repetitive wholesaling as a real estate activity requiring formal brokerage oversight. If you operate in these regions, obtaining your license can actually be a competitive advantage, allowing you to collect commissions when a wholesale deal isn't the best fit and providing you with direct access to the MLS for more accurate data. Even in more permissive environments like Texas or Nevada, the trend is moving toward mandatory disclosures that inform the seller exactly how you intend to profit from the assignment of the contract.

The core of legal compliance in wholesale real estate lies in the concept of equitable interest and the transparency of your intentions with the homeowner. When you enter into a purchase agreement, you are not claiming to own the dirt and the bricks; instead, you own a contract that grants you the right to purchase that property at a specific price. To remain on the right side of the law, your marketing should always reflect that you are selling your "interest in a contract" rather than the home itself, which helps you avoid accusations of unlicensed brokering. Recent legislation, including the Wholesale Real Estate Transaction Transparency and Protection Act of 2025, now requires clear, written notification to sellers that you are an investor looking to profit through assignment. Providing this information upfront builds trust with motivated sellers and ensures that your deal won't be derailed by a title company or attorney during the closing process.

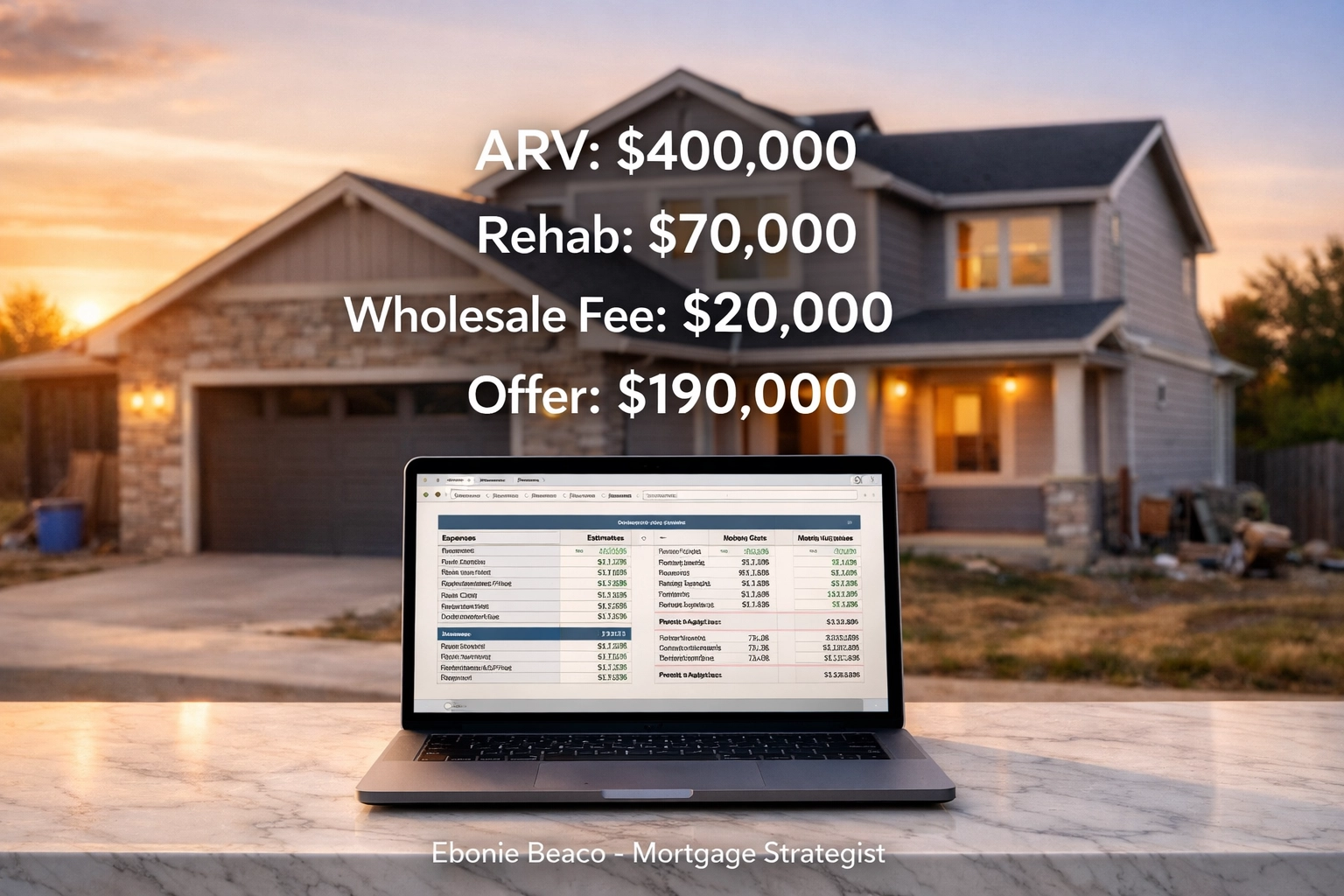

Understanding the financial mechanics of a compliant deal is essential for ensuring that everyone in the transaction: including your end buyer and the original seller: walks away with a clear understanding of the value created. For an investor looking at a distressed property in a market like Virginia or Michigan, a typical compliant deal breakdown must account for the After Repair Value (ARV) and the necessary margins for your cash buyer. Consider a scenario where a property has an ARV of $400,000 and requires $70,000 in renovations to meet market standards for a traditional fix and flip. Using the 70% rule, you would calculate the Max Allowable Offer (MAO) by taking 70% of the ARV ($280,000), subtracting the rehab costs ($70,000), and then subtracting your desired assignment fee of $20,000. In this example, your contract price with the seller would be $190,000, and your end buyer would purchase the assignment for $210,000, leaving them with a $70,000 equity cushion after their repairs are completed.

| Component | Value |

|---|---|

| After Repair Value (ARV) | $400,000 |

| Rehab Estimate | $70,000 |

| 70% Rule Calculation | $280,000 |

| Wholesale Fee | $20,000 |

| Contract Price to Seller | $190,000 |

| Total Price to Cash Buyer | $210,000 |

Structuring your transactions through either an assignment of contract or a double closing is another critical decision that affects your compliance profile and your bottom line. An assignment is often the simplest path, where you transfer your rights to an end buyer for a fee, but it requires the seller to see exactly how much you are making on the deal. If you are working with a massive spread: perhaps a $50,000 fee on a $200,000 house: a double closing might be more appropriate to protect your privacy and ensure the transaction moves forward without friction. In a double closing, you actually purchase the property (A-to-B) and then immediately sell it to your end buyer (B-to-C), which often requires transactional funding to cover the first leg of the deal. While double closings incur higher closing costs and title fees, they provide a layer of separation that can be vital when dealing with sensitive sellers or institutional buyers who have strict internal policies.

Federal regulations such as the Real Estate Settlement Procedures Act (RESPA) and the Dodd-Frank Act also play a role in how you should approach wholesaling, particularly when your end buyers are looking for creative financing. You must be careful never to provide legal or financial advice unless you are licensed to do so, and you should always encourage your buyers to consult with a qualified mortgage strategist. As you scale your business, you may find that some of your buyers struggle to secure traditional funding for the properties you are sourcing, especially if those homes are in significant disrepair. This is where connecting your buyers with specialized lending products, such as fix and flip loans or bridge financing, can help you move inventory faster and close more assignment deals. By acting as a resource for both the property and the financing path, you become an indispensable partner in the local investment community.

The natural evolution for many successful wholesalers is to eventually transition from simply flipping contracts to becoming a buy-and-hold investor or a full-scale renovator. Wholesaling provides the cash flow and the "boots on the ground" experience needed to identify the best opportunities, but long-term wealth is built through property ownership and equity growth. When you decide to keep a deal for yourself, you will need to pivot from seeking cash buyers to seeking DSCR investor loans or landlord financing that allows you to leverage your capital. Understanding how to analyze a deal for a cash-out refinance after a renovation is a skill that will take you from a high-hustle wholesaler to a high-net-worth property owner. This growth trajectory is exactly why maintaining a clean, compliant track record is so important; your reputation with lenders and title companies will follow you throughout your entire career.

Working with an experienced mortgage strategist is one of the most effective ways to ensure your wholesale deals are structured for a smooth exit, especially when your buyers aren't using 100% of their own cash. I can help you evaluate the "financeability" of a deal before you even put it under contract, giving you a clear picture of what an end buyer will need to bring to the table. Whether you are navigating the complexities of a double closing in Chicago or trying to build a buyers list in the competitive Florida markets, having a professional partner who understands the nuances of investor financing is a game-changer. Explore our FAQ to learn more about how different loan products can support your growth, or book an appointment to discuss a specific deal scenario. Compliance and profitability are not mutually exclusive; they are the two pillars of a sustainable real estate career that stands the test of time.

📞 Work With Ebonie Beaco

If you are a wholesaler looking to:

- Close more deals

- Connect your buyers with financing

- Structure deals that actually get approved

- Learn how to grow into a real estate investor

I can help you every step of the way.

Ebonie Beaco Mortgage Strategist Home Loans Network NMLS #2389954

📱 Phone: 312-392-0664 📧 Schedule a 1 on 1: https://calendly.com/homeloansnetwork 🌐 Website: HomeLoansNetwork.com/contact-us

👉 Whether you need lending, deal structuring, or mentorship, reach out today.

Ebonie Beaco - Mortgage Strategist Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664

Meta Title: Wholesale Real Estate Compliance: Staying Legal & Profitable (2026) Meta Description: Learn how to stay compliant while wholesaling real estate. Explore licensing, disclosures, and legal deal structures to protect your investment business in 2026.