What is Escrow? Keeping Your Taxes and Insurance on Track

Navigating the world of real estate financing often feels like learning a second language. If you are a homeowner in Chicago, a landlord in Florida, or a fix-and-flip investor in California, you have likely seen the word "escrow" appear on your closing disclosures and monthly statements. While the term sounds technical, the concept is straightforward. Escrow is a tool designed to provide transparency and security for everyone involved in a property transaction.

Whether you are managing a single-family home or building a portfolio of rental properties using DSCR investor loans, understanding how these accounts function is a critical part of your financial strategy. This guide breaks down the mechanics of escrow, the math behind the payments, and how to stay ahead of your annual tax and insurance obligations.

Defining the Essentials

Escrow A legal arrangement where a neutral third party holds money or assets on behalf of two other parties until specific conditions are fulfilled. In mortgage lending, this ensures that funds are available to pay for property-related expenses without the homeowner having to manage separate due dates.

Escrow Agent A neutral third party, such as a title company or mortgage servicer, responsible for holding funds and disbursing them to the correct entities. The agent acts as a buffer to ensure that taxes and insurance premiums are paid accurately and on time.

Escrow Analysis An annual review performed by your mortgage servicer to determine if your current monthly deposits are sufficient to cover upcoming bills. This review prevents your account from falling short when tax rates or insurance premiums increase in states like Illinois or Virginia.

How Mortgage Escrow Functions

When you secure a mortgage to purchase a home, your monthly payment typically consists of four main parts: Principal, Interest, Taxes, and Insurance (often abbreviated as PITI). The "Taxes and Insurance" portion is what flows into your escrow account.

Think of your escrow account as a dedicated savings account managed by your lender. Every month, a portion of your payment is set aside in this bucket. When your property tax bill arrives from the county or your homeowners insurance premium is due, the lender pays those bills directly using the funds you have accumulated.

This system is common across all types of financing, from traditional primary residence loans to specialized landlord loans. Lenders prefer this arrangement because it minimizes risk. If property taxes go unpaid, the local government can place a lien on the property, which could take priority over the mortgage. By managing the escrow, the lender ensures their collateral remains protected.

The Mathematical Breakdown of Escrow

Understanding how much you owe each month does not have to be a guessing game. The calculation is based on your total annual obligations divided by the number of months in a year.

For many investors in markets like Georgia or Michigan, property taxes can vary significantly by county. Here is a simple example of how a mortgage servicer calculates the monthly escrow deposit.

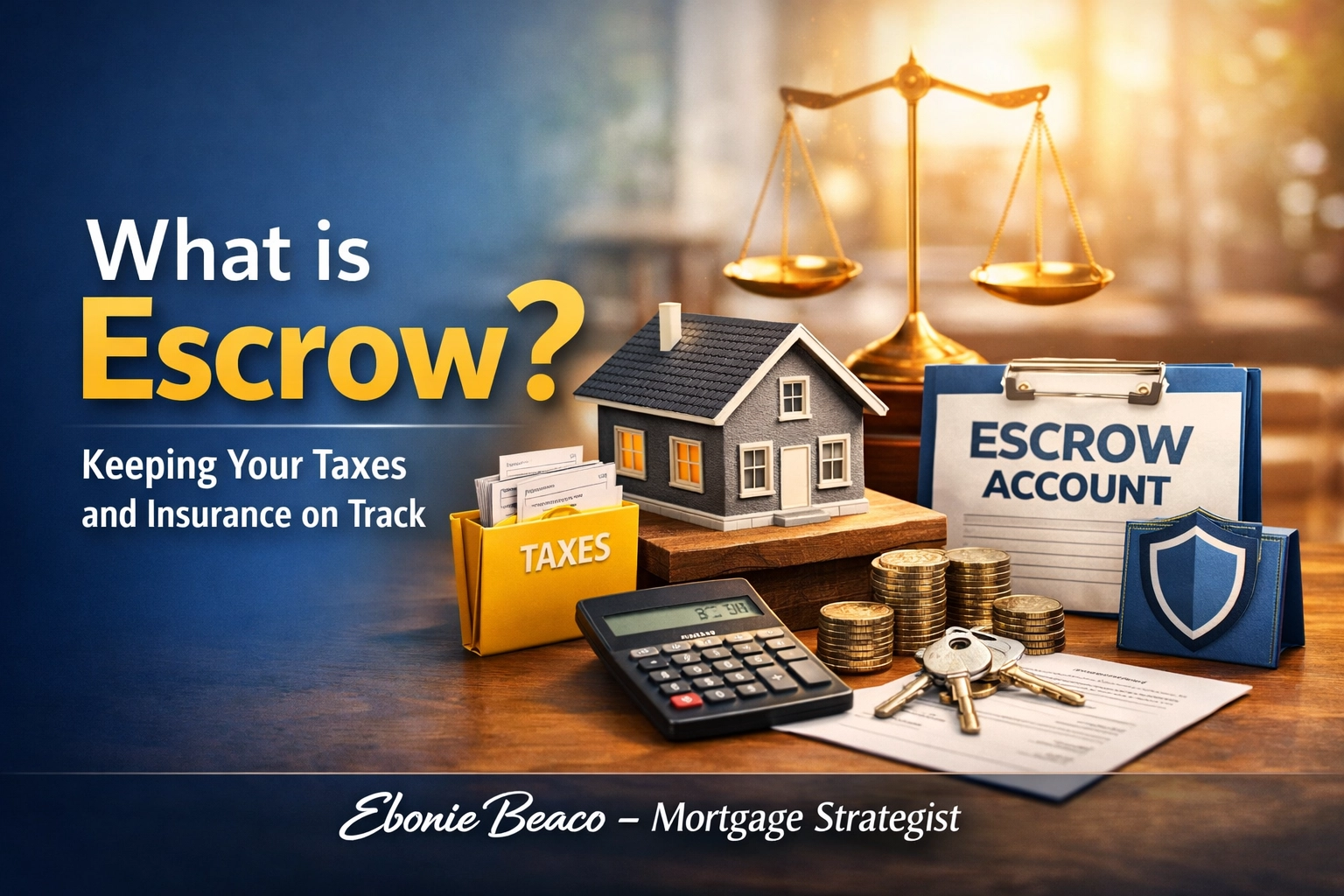

The Standard Calculation Example

Assume a property has the following annual expenses:

- Annual Property Taxes: $4,200

- Annual Homeowners Insurance: $1,200

- Total Annual Obligation: $5,400

To find the monthly amount, the servicer uses this formula: (Total Taxes + Total Insurance) / 12 = Monthly Escrow Payment

$5,400 / 12 = $450.00 per month

Visual Breakdown: Escrow Accounts Explained. Calculation: ($4,200 Taxes + $1,200 Insurance) / 12 = $450 Monthly Payment. Ebonie Beaco - Mortgage Loan Officer.

Visual Breakdown: Escrow Accounts Explained. Calculation: ($4,200 Taxes + $1,200 Insurance) / 12 = $450 Monthly Payment. Ebonie Beaco - Mortgage Loan Officer.

Beyond this base amount, many lenders require an Escrow Cushion. This is an extra amount (usually equal to two months of payments) held in the account to cover unexpected increases in tax assessments or insurance rate hikes. If you are looking to run your own numbers for a potential investment, you can use our mortgage calculators to estimate your full PITI payment.

Escrow in the Real Estate Investment World

For real estate investors, escrow accounts play a dual role. There is the mortgage escrow described above, but there is also the Earnest Money Escrow that occurs during the acquisition phase.

When you go under contract to buy a property in a competitive market like Virginia or Florida, you provide an earnest money deposit to show you are a serious buyer. This money is held in an escrow account by a title company or attorney. It stays there until the deal closes, at which point it is applied toward your down payment or closing costs. If the deal falls through due to a protected contingency, the escrow agent ensures the money is returned to you according to the contract terms.

Strategies for Landlords and BRRRR Investors

If you are using a DSCR rental property loan to scale your portfolio, escrow is often mandatory. Investors using the BRRRR strategy (Buy, Rehab, Rent, Refinance, Repeat) need to be particularly mindful of escrow during the refinance stage.

When you refinance your property, your new lender will set up a new escrow account. You will receive a refund check from your old lender's escrow account a few weeks after the loan is paid off. Managing this transition effectively ensures you have the liquidity needed for your next acquisition.

Escrow Analysis: Surpluses and Shortages

Once a year, your mortgage servicer will send you an Escrow Analysis Statement. This document compares what they projected you would spend on taxes and insurance versus what was actually paid.

What is an Escrow Shortage?

A shortage occurs when your taxes or insurance premiums increased more than expected. This is common in rapidly growing areas of California or Florida where property values: and subsequently tax assessments: are rising.

- The Result: Your monthly mortgage payment will likely increase to cover the gap and rebuild the required cushion.

- Your Choice: You can usually pay the shortage in a one-time lump sum or spread the cost over the next 12 months.

What is an Escrow Surplus?

A surplus happens if your taxes or insurance costs decreased. In this scenario, the servicer will typically send you a check for the overage, provided the amount exceeds a certain threshold (usually $50).

If you find yourself confused by your annual statement, reviewing our FAQ section can provide quick answers to common homeowner concerns regarding payment fluctuations.

Why Transparency in Escrow is Vital

At Home Loans Network, we believe transparency is the foundation of a successful lending relationship. Whether you are a first-time homebuyer in Indiana or a seasoned commercial investor in Arkansas, you deserve to know exactly where every dollar of your mortgage payment is going.

Escrow accounts eliminate the "sticker shock" of a multi-thousand dollar tax bill arriving in your mailbox. By spreading the cost over 12 months, it makes homeownership and property management much more predictable. For investors, this predictability is essential for calculating accurate cash flow projections on rental properties.

Frequently Asked Questions About Escrow

Can I waive escrow and pay taxes/insurance myself? Some loan programs allow you to manage these payments yourself if you have a certain amount of equity (usually 20% or more). However, many lenders charge a small fee or a slightly higher interest rate for this "escrow waiver" because it increases their risk.

Does my escrow account earn interest? In most states, lenders are not required to pay interest on escrow accounts. However, a few states have specific laws that mandate a small interest payment to the homeowner.

What happens if the lender forgets to pay the tax bill? Since the lender is responsible for the disbursement, they are generally liable for any late fees or penalties incurred if they fail to pay the bill on time from an adequately funded escrow account.

Explore more about the loan process to see how escrow fits into the bigger picture of your closing.

Navigating Your Real Estate Journey

Whether you are looking to optimize your current mortgage or you are ready to expand your investment footprint with a Fix and Flip loan, having a clear understanding of your financial obligations is the first step toward success. Escrow is more than just a line item on your statement; it is a system designed to provide stability in your real estate holdings.

If you are a homeowner wondering why your payment changed, or an investor trying to structure a multi-unit deal in Alabama or Missouri, we are here to help you navigate the complexities of mortgage financing with confidence.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664

Questions about your escrow or mortgage? Contact Ebonie Beaco for a personal guide.