What is a Rate-Term Refinance and How Does It Save You Money?

Navigating the world of mortgage financing often feels like learning a second language. If you already own a home in Illinois, Florida, or Virginia, you have likely heard the term "refinance" tossed around during market shifts. Among the various ways to restructure debt, the Rate-Term Refinance stands out as one of the most effective tools for improving your financial position without increasing your total debt load.

Whether you are a primary homeowner in Chicago looking to breathe easier each month or a landlord in Alabama trying to improve the cash flow on a rental property, understanding this strategy is essential. A rate-term refinance is designed specifically to change the "interest rate," the "term" (length of the loan), or both, without taking additional cash out of the property's equity.

Defining the Rate-Term Refinance

Rate-Term Refinance: A mortgage transaction where the primary goal is to replace an existing lien with a new loan that offers more favorable interest rates or a different repayment schedule. Practical Application: You use this to lower your monthly obligation or pay off your home faster without touching the equity you have built up.

Explore the mechanics of how this works. Unlike a cash-out refinance: which allows you to pull liquid funds from your home for renovations or other investments: the rate-term refinance is strictly about the loan's structure. You are essentially trading your old contract for a new one that fits your current financial goals better. You can access more information about these options at https://www.homeloansnetwork.com/home-refinance.

How a Rate-Term Refinance Operates

When you move forward with a rate-term refinance, your new lender pays off your original mortgage in full. You are then left with a single new loan. Because you are not withdrawing equity, the loan-to-value (LTV) ratio often stays lower, which can lead to better interest rates and a smoother underwriting process.

In states like Michigan and Georgia, where housing markets have seen steady activity, homeowners often use this to move from an Adjustable-Rate Mortgage (ARM) into a Fixed-Rate Mortgage. This provides long-term stability and protects against future market volatility.

Why Homeowners Choose This Path

There are three primary reasons to pull the trigger on a rate-term refinance:

- Lowering the Interest Rate: This is the most common motivation. When market rates drop below your current rate, refinancing can significantly reduce your monthly overhead.

- Adjusting the Loan Term: You might choose to move from a 30-year mortgage to a 15-year mortgage. While this often increases the monthly payment, it drastically reduces the total interest paid over the life of the loan.

- Removing Private Mortgage Insurance (PMI): If your home value has increased in markets like California or Florida, a rate-term refinance can help you reach the 80% LTV threshold required to drop PMI, even if the interest rate stays the same.

The Math: How a 1% Reduction Changes Your Life

To truly understand the benefit, we must look at the numbers. Let’s look at a typical scenario for a homeowner or an investor with a single-family rental.

The Scenario:

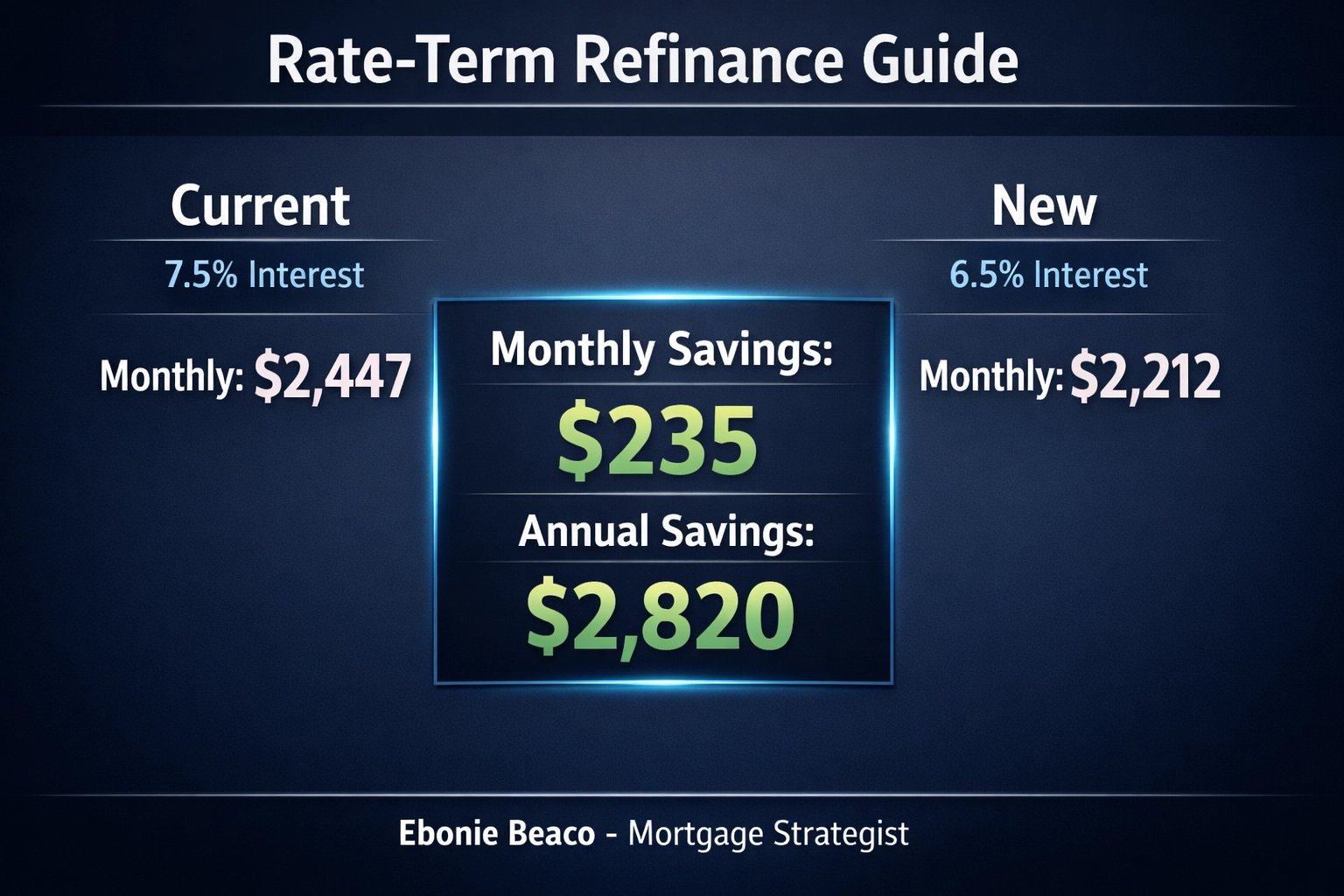

- Current Loan Balance: $350,000

- Current Interest Rate: 7.5%

- New Interest Rate: 6.5%

- Loan Term: 30 Years Fixed

The Calculation:

- Current Monthly Principal & Interest: $2,447

- New Monthly Principal & Interest: $2,212

- Monthly Savings: $235

- Annual Savings: $2,820

- Total Interest Saved Over 30 Years: $84,600

Image instructions: Create a clean financial comparison chart titled "Rate-Term Refinance Guide". Show two columns: "Current (7.5%)" with a payment of $2,447 and "New (6.5%)" with a payment of $2,212. Highlight the "Monthly Savings: $235" and "Annual Savings: $2,820". Add "Ebonie Beaco - Mortgage Loan Officer" at the bottom. Do not include money, cash, or portraits.

Image instructions: Create a clean financial comparison chart titled "Rate-Term Refinance Guide". Show two columns: "Current (7.5%)" with a payment of $2,447 and "New (6.5%)" with a payment of $2,212. Highlight the "Monthly Savings: $235" and "Annual Savings: $2,820". Add "Ebonie Beaco - Mortgage Loan Officer" at the bottom. Do not include money, cash, or portraits.

Jump in and analyze how that $235 per month could be used. For a landlord in Indiana or Arkansas, that extra $235 is pure profit (cash flow) every single month. For a homeowner, it could be redirected into a retirement account or used to pay down the principal even faster.

Strategic Use for Real Estate Investors

Investors frequently use rate-term refinances as part of a larger portfolio strategy. If you are a BRRRR investor (Buy, Rehab, Rent, Refinance, Repeat), the "Refinance" step is where you stabilize your debt. While many investors prefer cash-out options to fund the next deal, a rate-term refinance is often the better choice if the goal is to maximize the Debt Service Coverage Ratio (DSCR).

DSCR (Debt Service Coverage Ratio): A metric used by lenders to measure a property's ability to cover its debt payments with its rental income. Practical Application: By lowering your interest rate through a rate-term refinance, you improve your DSCR, which makes your portfolio look stronger to lenders for future financing.

In competitive markets like Northern Virginia or parts of Kentucky, maintaining a high DSCR allows you to continue scaling your investments. You can explore how these ratios impact your lending options at https://www.homeloansnetwork.com/mortgage-basics.

Switching from ARM to Fixed-Rate

Many buyers who purchased homes during periods of high rates opted for Adjustable-Rate Mortgages (ARMs) to get a lower initial "teaser" rate. However, ARMs come with the risk of payments increasing after the initial fixed period.

A rate-term refinance allows you to "lock in" a fixed rate. This transparency in your future payments is invaluable for long-term planning. Whether you are managing a household budget or a commercial multifamily property, knowing exactly what your debt obligation is for the next 15 to 30 years provides peace of mind.

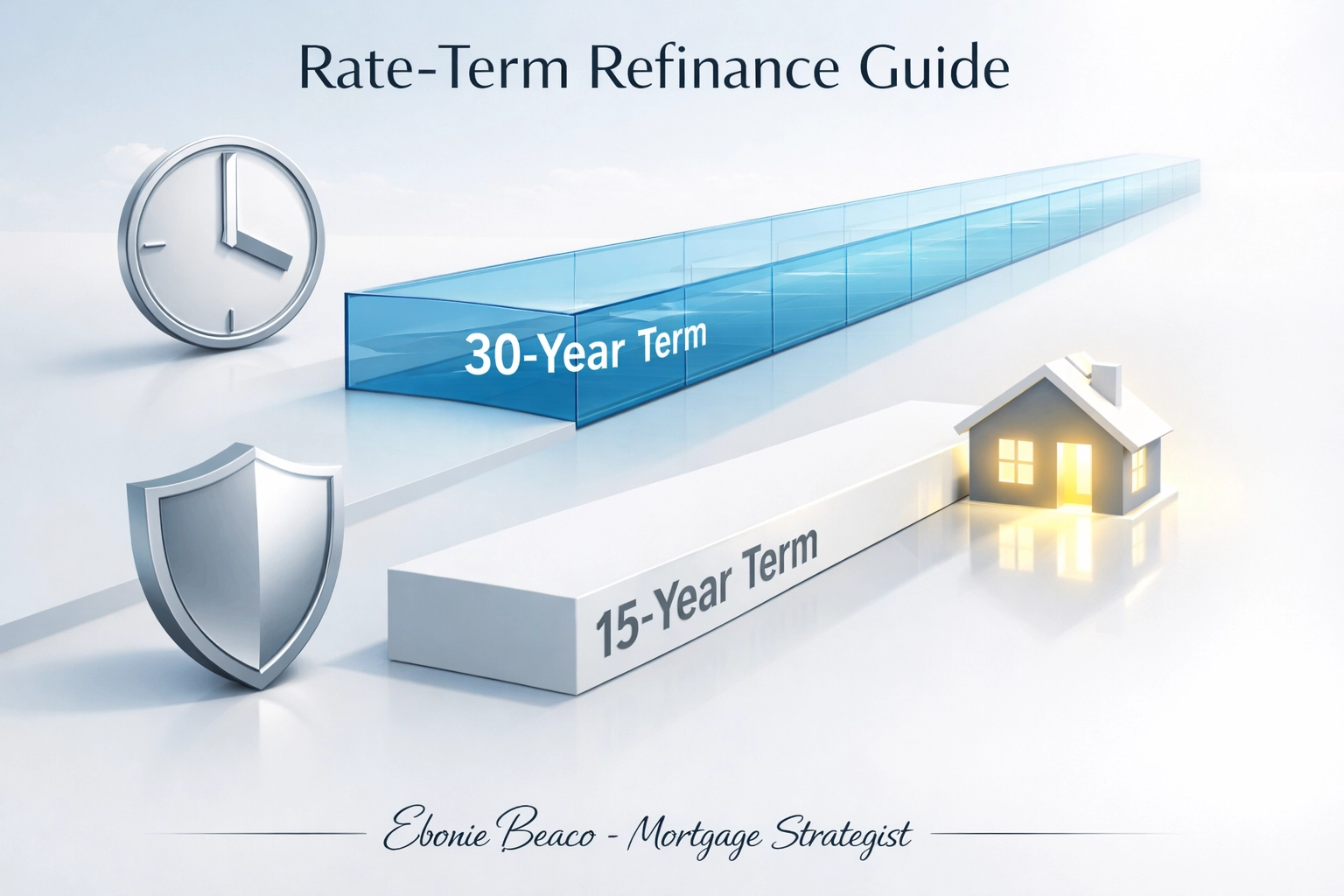

Shortening Your Loan Term

For those focused on wealth building and debt elimination, refinancing from a 30-year term to a 15-year or 20-year term is a power move.

Consider a homeowner in Missouri who has 25 years left on a 30-year mortgage. By refinancing into a 15-year term at a lower rate, they might see their payment stay nearly the same while shaving 10 years off their debt. This is a common strategy for individuals nearing retirement who want to enter that phase of life with a free-and-clear property.

Image instructions: Create a graphic titled "Rate-Term Refinance Guide". Show a timeline comparison between a 30-year loan and a 15-year loan. Use icons representing "Time Saved" and "Interest Saved". Include the text "Ebonie Beaco - Mortgage Loan Officer" at the bottom. Ensure no currency symbols or cash are visible.

Image instructions: Create a graphic titled "Rate-Term Refinance Guide". Show a timeline comparison between a 30-year loan and a 15-year loan. Use icons representing "Time Saved" and "Interest Saved". Include the text "Ebonie Beaco - Mortgage Loan Officer" at the bottom. Ensure no currency symbols or cash are visible.

Qualification Standards for Refinancing

While a rate-term refinance is generally easier to qualify for than a cash-out refinance, lenders still have specific requirements.

- Credit Score: Most programs, including conventional and FHA, look for a score of 620 or higher, though higher scores secure the best rates https://www.homeloansnetwork.com/faq.

- Equity: You typically need some equity in the home, although some programs like the FHA Streamline or VA Interest Rate Reduction Refinance Loan (IRRRL) have very flexible equity requirements.

- Debt-to-Income (DTI): Lenders will verify that your income is sufficient to cover the new mortgage along with your other debts.

- Appraisal: Depending on the loan type and the amount of equity, an appraisal may be required to confirm the current market value of the property in its local market, such as Atlanta or Chicago.

Closing Costs and the Break-Even Point

It is important to remember that refinancing is not free. You will encounter closing costs, which typically range from 2% to 5% of the loan amount. These can include appraisal fees, title insurance, and loan origination fees.

To determine if a rate-term refinance is right for you, calculate your "break-even point." This is the number of months it takes for your monthly savings to cover the cost of the refinance.

Break-Even Calculation:

- Total Closing Costs: $5,000

- Monthly Savings: $200

- Break-Even Point: 25 Months ($5,000 / $200)

If you plan to stay in the home or keep the investment property longer than 25 months, the refinance is a winning strategy. You can use our tools to run your own scenarios here: https://www.homeloansnetwork.com/mortgage-calculators.

The Process: Step-by-Step

Accessing a better mortgage term is a straightforward process when you have the right guidance.

- Review Your Current Note: Look at your existing interest rate, remaining term, and whether you have a prepayment penalty.

- Check Your Credit: Ensure there are no errors on your report that could negatively impact your new rate.

- Gather Documentation: You will likely need recent pay stubs, W2s, and bank statements, similar to when you first purchased the home.

- Compare Scenarios: Work with a mortgage strategist to see how different rates and terms impact your long-term wealth.

- Lock Your Rate: Once you find a scenario that fits your goals, lock in the rate to protect yourself from market fluctuations.

- Close the Loan: Sign the final documents and begin your new, lower-cost mortgage journey.

Compare your current situation with what is possible in today's market. Even a small change in percentage can result in tens of thousands of dollars staying in your pocket rather than going to the bank.

Final Thoughts for Homeowners and Investors

The housing markets in states like Florida, California, and Georgia are constantly evolving. As a homeowner or a landlord, your mortgage should not be a "set it and forget it" obligation. It is a dynamic financial tool that should be adjusted as the market and your personal goals change.

A rate-term refinance is one of the cleanest ways to optimize your finances. It doesn't require you to take on more debt; it simply ensures that the debt you have is as inexpensive and efficient as possible.

Ready to lower your rate? Contact Ebonie Beaco for a rate-term refinance.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664