What is a DSCR Loan? Financing Your Rental Portfolio

If you have ever tried to get a traditional mortgage for a rental property, you know the drill. The bank asks for two years of tax returns, W-2s, pay stubs, and a deep dive into your personal Debt-to-Income (DTI) ratio. For many real estate investors: especially those who are self-employed or already own multiple properties: this process is a massive hurdle.

Enter the DSCR Loan.

DSCR stands for Debt Service Coverage Ratio. It is a type of non-QM (Non-Qualified Mortgage) loan designed specifically for real estate investors. Instead of looking at how much money you make at your day job, lenders look at how much income the property itself generates.

If the rent covers the mortgage payment, you are often good to go. This makes it a primary tool for landlords in markets like Chicago, Atlanta, and Miami who want to scale their portfolios without the red tape of traditional financing.

Defining the Debt Service Coverage Ratio

Debt Service Coverage Ratio (DSCR): A financial metric used by lenders to measure a property's ability to cover its monthly debt obligations using its own rental income.

In practical terms, this ratio tells the lender if the property is "self-sustaining." If the property brings in more cash than it costs to keep it running, the risk to the lender is lower.

How the Calculation Works

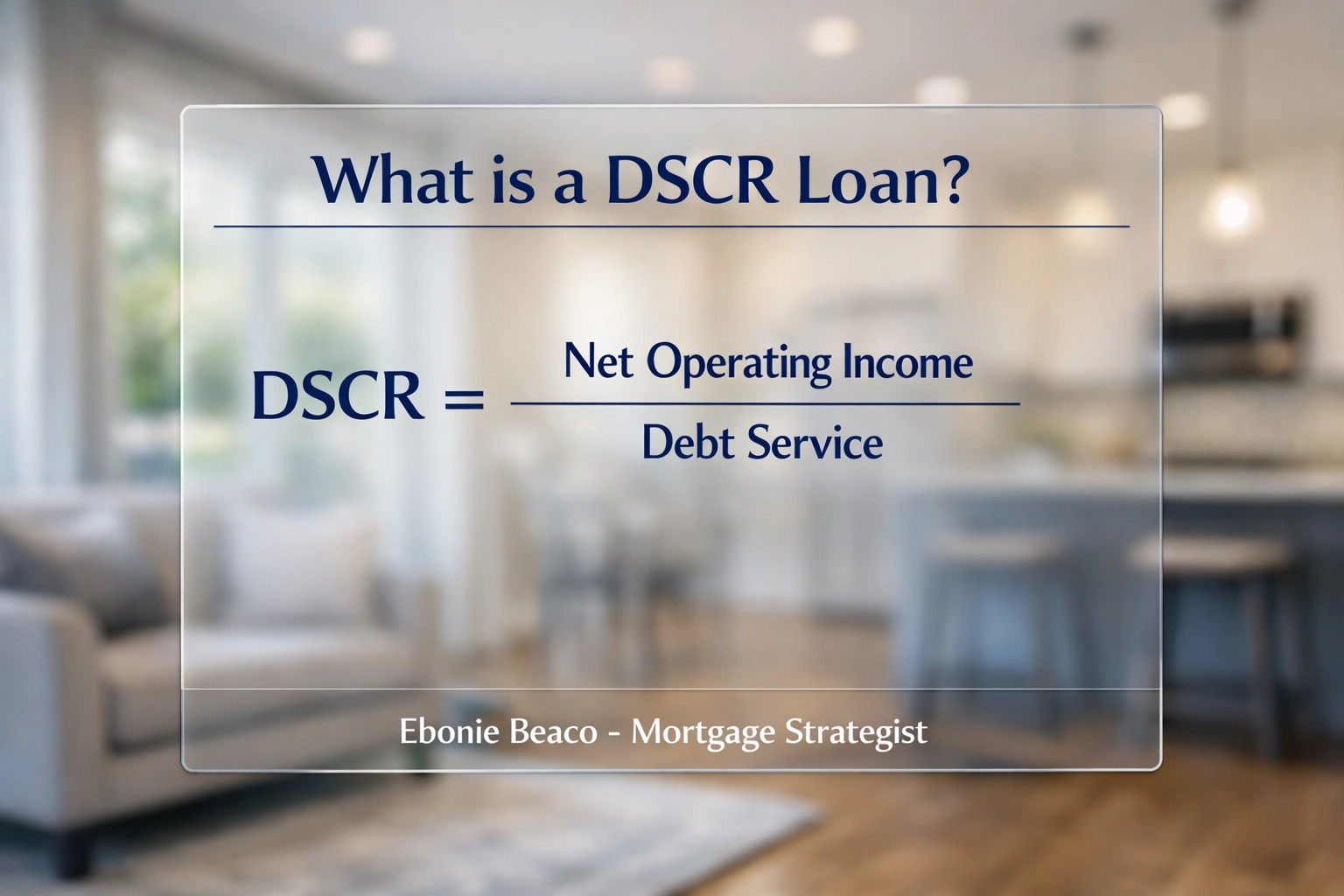

The math behind a DSCR loan is straightforward. Lenders calculate the ratio by dividing the Net Operating Income (NOI): which is the gross rent minus operating expenses: by the total Debt Service (the monthly mortgage payment including principal, interest, taxes, insurance, and any HOA fees).

(Note: Image displays Title: 'What is a DSCR Loan?' Calculation: 'DSCR = Net Operating Income / Debt Service'. Bottom: 'Ebonie Beaco - Mortgage Loan Officer')

(Note: Image displays Title: 'What is a DSCR Loan?' Calculation: 'DSCR = Net Operating Income / Debt Service'. Bottom: 'Ebonie Beaco - Mortgage Loan Officer')

Let’s look at a real-world scenario for a rental property in Virginia Beach:

- Monthly Rent: $2,500

- Total Monthly Mortgage Payment (PITIA): $2,000

- Calculation: $2,500 / $2,000 = 1.25 DSCR

In this case, the ratio is 1.25. Most lenders prefer a DSCR of 1.20 or higher, meaning the property generates 20% more income than the cost of the debt. However, in some high-growth markets like Florida or California, some programs allow for a 1.0 ratio or even "no ratio" loans if the borrower has a strong credit profile and a larger down payment.

Why Investors Prefer DSCR Loans Over Conventional Financing

Traditional loans are built for homeowners, not business owners. When you are buying your fifth or tenth rental property in Michigan or Indiana, the traditional banking system starts to view you as a high risk because of your total debt load. DSCR loans solve this problem.

No Personal Income Verification

Since the loan is qualified based on the property’s cash flow, you do not need to provide tax returns or pay stubs. This is a game-changer for self-employed investors who take legal deductions that might make their personal income look lower on paper than it actually is.

Faster Closing Times

Without the need for extensive personal income underwriting, the process moves much faster. In competitive markets like Tampa or Charlotte, being able to close quickly can be the difference between winning a deal and losing it to a cash buyer.

Borrowing in an LLC

Many investors prefer to hold their properties in a Limited Liability Company (LLC) for asset protection. Conventional loans usually require you to close in your personal name. DSCR loans allow you to close directly in the name of your LLC, keeping your personal and business assets separate.

No Limit on Number of Properties

Conventional lenders often cap the number of financed properties you can own (usually at 10). DSCR lenders typically have no such limit. Whether you own five doors or fifty doors in Arkansas or Alabama, you can continue to use DSCR financing to grow.

Explore more about the loan process to see how these timelines compare to traditional products.

Scaling with the BRRRR Method

If you are a fan of the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat), the DSCR loan is your best friend.

After you have purchased a distressed property in a city like Gary, Indiana or Decatur, Georgia, and finished the renovations, you need to pull your capital back out to move on to the next deal. A DSCR cash-out refinance allows you to do this based on the new appraised value and the new rental rate, regardless of your personal DTI.

(Note: Image shows a deal breakdown of a BRRRR refinance: After Repair Value (ARV) $200,000, Loan Amount at 75% LTV $150,000, Monthly Rent $1,800, PITIA $1,400, DSCR 1.28. Bottom: 'Ebonie Beaco - Mortgage Loan Officer')

(Note: Image shows a deal breakdown of a BRRRR refinance: After Repair Value (ARV) $200,000, Loan Amount at 75% LTV $150,000, Monthly Rent $1,800, PITIA $1,400, DSCR 1.28. Bottom: 'Ebonie Beaco - Mortgage Loan Officer')

This strategy allows you to recycle your initial investment capital over and over again. You can jump in and access equity to fund your next acquisition without waiting years to save up another down payment.

Requirements for a DSCR Loan

While these loans are more flexible regarding income, lenders still have standards to ensure the investment is sound.

Credit Score

Your personal credit score still plays a role. Most DSCR programs require a minimum score of 620 to 640, though the best rates are reserved for those with scores of 720 and above.

Loan-to-Value (LTV)

Expect to put more skin in the game. While some conventional loans allow for lower down payments, DSCR loans typically require 20% to 25% down for a purchase. For a cash-out refinance, you can usually access up to 75% or 80% of the property’s value.

Appraisals and Rent Schedules

The lender will order an appraisal that includes a "Comparable Rent Schedule" (Form 1007 for single-family homes). This confirms to the lender that the rent you are claiming is consistent with the local market in areas like Chicago or Los Angeles.

Prepayment Penalties

Unlike most consumer mortgages, DSCR loans often include a prepayment penalty. This is standard in commercial-style lending. It typically lasts for 1 to 5 years. You can often pay a slightly higher interest rate to have this penalty reduced or removed, depending on your long-term strategy.

Short-Term Rentals and Airbnb Financing

The rise of short-term rentals (STRs) has changed the landscape for investors in vacation-heavy states like Florida and California. Traditional lenders often struggle to categorize Airbnb income.

However, many DSCR lenders now accept "AirDNA" data or historical STR income to qualify the loan. If you are looking at a property in Destin or Joshua Tree, you can use the projected short-term rental income to hit your DSCR requirements, even if the long-term annual rent wouldn't cover the mortgage.

Access our mortgage calculators to run your own numbers on a potential STR deal.

Is a DSCR Loan Right for Your Portfolio?

This financing path is ideal if:

- You are a self-employed investor with complex tax returns.

- You have reached the "maxed out" limit with conventional lenders.

- You want to protect your personal credit from being weighed down by multiple mortgage balances.

- You are focused on cash flow and scaling quickly.

It might not be the right choice if you are looking for the absolute lowest interest rate possible, as DSCR rates are typically 0.75% to 1.5% higher than conventional rates. However, for most investors, the trade-off for speed and flexibility is well worth the slightly higher cost of capital.

For those just starting out, check out our mortgage basics to get a foundational understanding of how these different programs interact with your long-term goals.

Navigating the Market in 2026

The real estate market across Georgia, Virginia, and the Midwest continues to evolve. Staying ahead requires a mortgage strategist who understands that every deal is unique. Whether you are looking for your first rental in Little Rock or refinancing a 10-unit building in Detroit, the right leverage is the key to building wealth.

We focus on helping you compare options objectively so you can make the best decision for your financial future. If you are ready to explore how a DSCR loan can unlock your next investment opportunity, let's talk.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664