What Exactly is a DSCR Loan? The Investor’s Secret Weapon

If you have ever tried to get a mortgage for an investment property through a big traditional bank, you know the drill. They want your tax returns from the last two years, every pay stub you’ve ever touched, and a detailed explanation of why you spent twenty dollars at a taco stand three months ago. For a lot of real estate investors: especially those who are self-employed or already own a few properties: the traditional lending process is a massive headache.

This is where the DSCR loan comes in. It is often called the "Investor’s Secret Weapon" because it skips the personal income verification and focuses on what actually counts: the property’s ability to pay for itself.

At Home Loans Network, we see investors in markets like Chicago, Florida, and Virginia moving away from conventional loans in favor of this flexible option. Whether you are looking to buy your first rental in Michigan or scale a massive portfolio in California, understanding how this works is a total game-changer.

Flipping the Script on Traditional Lending

Traditional mortgages are "Qualified Mortgages" (QM). They are designed for homeowners with W-2 jobs and predictable income. Lenders look at your Debt-to-Income (DTI) ratio, which compares your personal monthly debts to your personal monthly gross income.

A DSCR loan is a Non-QM (Non-Qualified Mortgage) product. Instead of looking at you, the lender looks at the property.

DSCR Definition

DSCR (Debt Service Coverage Ratio): A financial metric used by lenders to measure a property’s ability to cover its monthly mortgage debt using its own rental income.

In simple terms, if the rent covers the mortgage payment, you are usually good to go. This approach is perfect for landlords who have high tax deductions that make their personal income look lower than it actually is.

How the DSCR Calculation Works

The math behind a DSCR loan is straightforward, but it is the most important part of the entire deal. Lenders calculate the ratio by dividing the property's Net Operating Income (NOI) by the annual or monthly debt service (the mortgage payment).

For most residential DSCR loans, the "Debt Service" includes Principal, Interest, Taxes, Insurance, and any HOA fees (PITI+H).

The Formula

DSCR = Monthly Rental Income / Monthly Debt Service (PITI)

Let’s look at a real-world scenario. Imagine you are eyeing a duplex in Gary, Indiana or a condo in Miami, Florida.

- Gross Monthly Rent: $3,000

- Monthly Mortgage Payment (Principal & Interest): $1,800

- Property Taxes: $300

- Insurance: $200

- HOA Fees: $100

- Total Monthly Debt Service: $2,400

The Calculation: $3,000 (Rent) ÷ $2,400 (Debt Service) = 1.25

In this case, your DSCR is 1.25. This means the property generates 25% more income than what is needed to pay the mortgage. Most lenders look for a ratio of 1.0 or higher, though some programs allow for "no ratio" or "low ratio" deals if you have a larger down payment.

Visual Description: A clean, professional infographic titled "Understanding DSCR Loans" showing the calculation: Gross Monthly Rent ($3,000) divided by Total Monthly Debt Service ($2,400) equals 1.25 DSCR. The bottom of the image includes "Ebonie Beaco - Mortgage Loan Officer". No money or cash is pictured.

Visual Description: A clean, professional infographic titled "Understanding DSCR Loans" showing the calculation: Gross Monthly Rent ($3,000) divided by Total Monthly Debt Service ($2,400) equals 1.25 DSCR. The bottom of the image includes "Ebonie Beaco - Mortgage Loan Officer". No money or cash is pictured.

Why Investors Love DSCR Loans

There are several reasons why this is the preferred tool for serious real estate professionals in states like Georgia, Alabama, and Arkansas.

1. No Personal Income Verification

Since the loan is based on the property’s cash flow, you don’t have to provide tax returns or pay stubs. This is a massive relief for self-employed investors or those who have "paper losses" on their tax returns due to depreciation. You can explore more about our specialized processes at the Home Loans Network loan process page.

2. Faster Closing Times

Because there is no deep dive into your personal finances, the underwriting process is often much faster. When you are competing for a hot property in a market like Northern Virginia or suburban Chicago, speed is everything.

3. Ability to Scale

Traditional lenders often cap the number of properties you can own (usually 10). With DSCR loans, you can theoretically own an unlimited number of properties. Each deal stands on its own. This is how investors build massive rental empires across multiple states.

4. Close in an LLC

Most traditional conventional loans require you to close in your personal name. DSCR lenders actually prefer (and sometimes require) that you close in the name of an LLC. This provides an extra layer of asset protection and keeps your personal credit report cleaner.

Scaling Your Portfolio with DSCR

If you are following the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat), the DSCR loan is your best friend during the refinance stage.

Once you have renovated the property and placed a tenant, you can use a DSCR loan to do a cash-out refinance. This allows you to pull your original capital back out based on the new, higher appraised value and the new rental income. You can then take that cash and move on to your next deal in Michigan, Missouri, or Illinois.

For more details on how refinancing works in these scenarios, check out our home refinance guide.

Visual Description: A professional diagram titled "Understanding DSCR Loans" illustrating the flow of the BRRRR method with a focus on the 'Refinance' step using a DSCR loan. The footer reads "Ebonie Beaco - Mortgage Loan Officer".

Visual Description: A professional diagram titled "Understanding DSCR Loans" illustrating the flow of the BRRRR method with a focus on the 'Refinance' step using a DSCR loan. The footer reads "Ebonie Beaco - Mortgage Loan Officer".

Common Scenarios for DSCR Loans

We see these loans used in a variety of ways across the country. Here are a few examples of how our clients are putting them to work:

- Short-Term Rentals (Airbnb/VRBO): Many DSCR lenders now allow you to use "airDNA" data or short-term rental projections to qualify. This is huge for investors in vacation spots throughout Florida and California.

- Small Multi-Family: These loans are perfect for 2-4 unit properties where the combined rent of all units creates a very strong debt service coverage ratio.

- Foreign National Investors: If you are an investor from outside the U.S. looking to buy property in Georgia or Virginia, DSCR loans are often one of the few pathways available since you likely don't have a U.S. credit score or tax history.

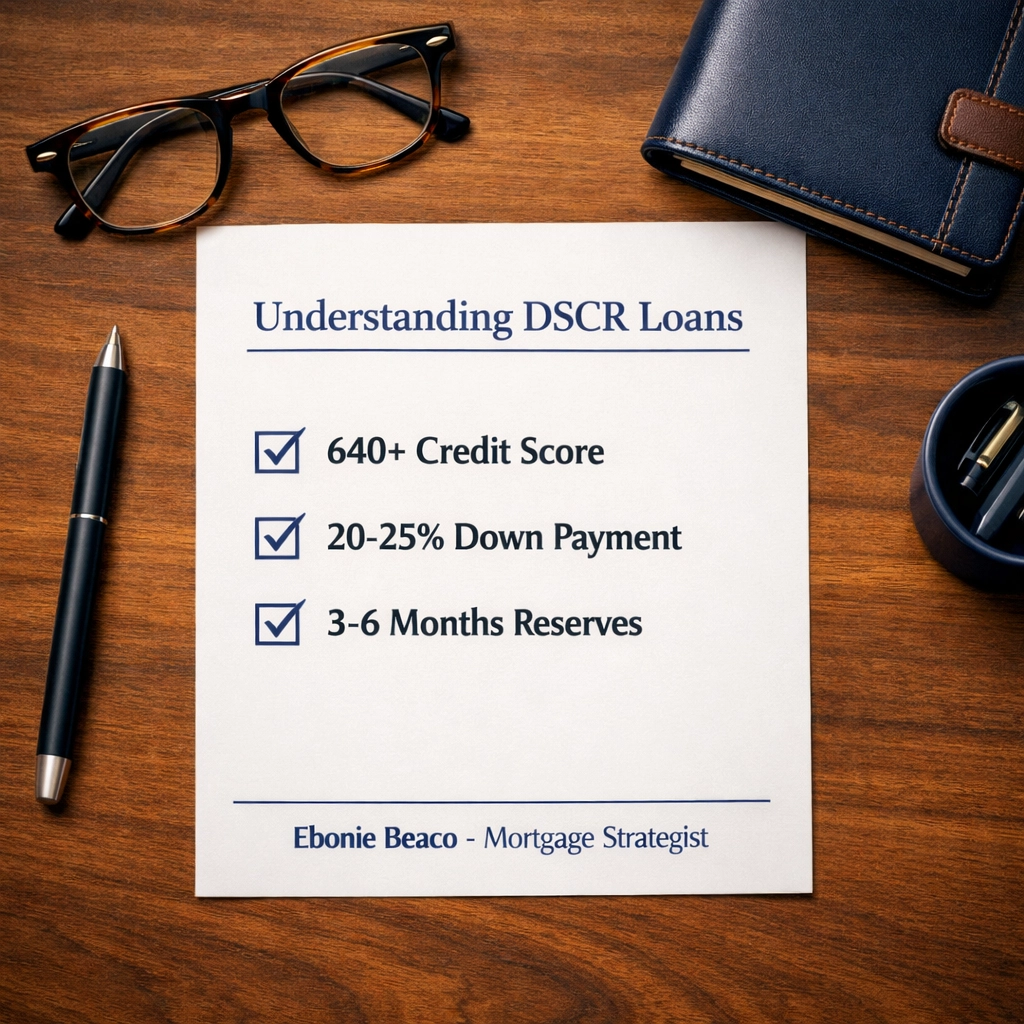

What You Need to Qualify

While these loans are easier to get in terms of paperwork, they aren't "easy" in terms of requirements. Lenders are taking on more risk by not looking at your personal income, so they compensate in other ways:

- Credit Score: You generally need a decent credit score (typically 640 or higher).

- Down Payment: Expect to put down at least 20% to 25%.

- Appraisal and Rent Schedule: The lender will order an appraisal that includes a "1007 Rent Schedule." This is where an independent appraiser confirms what the fair market rent is for the property.

- Cash Reserves: Lenders like to see that you have 3 to 6 months of mortgage payments tucked away in a bank account just in case the property sits vacant for a bit.

If you have questions about specific requirements for your state, you can look through our mortgage basics section or visit our FAQ page.

Visual Description: A professional list titled "Understanding DSCR Loans" showing key requirements: 640+ Credit Score, 20-25% Down Payment, and 3-6 Months Reserves. The footer reads "Ebonie Beaco - Mortgage Loan Officer".

Visual Description: A professional list titled "Understanding DSCR Loans" showing key requirements: 640+ Credit Score, 20-25% Down Payment, and 3-6 Months Reserves. The footer reads "Ebonie Beaco - Mortgage Loan Officer".

Is a DSCR Loan Right for You?

The choice between a traditional loan and a DSCR loan often comes down to your long-term goals. If you have a steady W-2 job and this is your very first rental property, a conventional loan might offer a lower interest rate.

However, if you are looking to build a business, protect your assets through an LLC, and move quickly without the headache of tax return verification, the DSCR loan is unbeatable. It is the bridge that allows you to transition from "someone who owns a house" to "a professional real estate investor."

Don't let the complexity of traditional banking hold you back from growing your portfolio in Kentucky, Indiana, or any of the other states we serve. The property should do the heavy lifting for you.

Taking the Next Step

Whether you are ready to lock in a rate for a new purchase in Chicago or you want to sit down and map out a growth strategy for your portfolio, I am here to help. Real estate investing is a journey, and having the right financing partner is a vital part of the process.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664